Revamp your divestiture process

Get a secure place to arrange business units for divestment, collect information and files, centralize communications and questions, and effectively manage the overall divestiture process.

Confidently and efficiently prepare your business for a divestiture

DealRoom’s interface makes it easy for buyers to focus on the value of your company instead of the process of harvesting files in the diligence process. With a high level permissibility feature, you can control anything that goes in and out of the platform.

Reduce divestment costs

Stop paying for multiple software platforms to manage your divestitures. Reduce software expenses by centralizing all deal work and speeding up the divestiture process.

Analyse the data

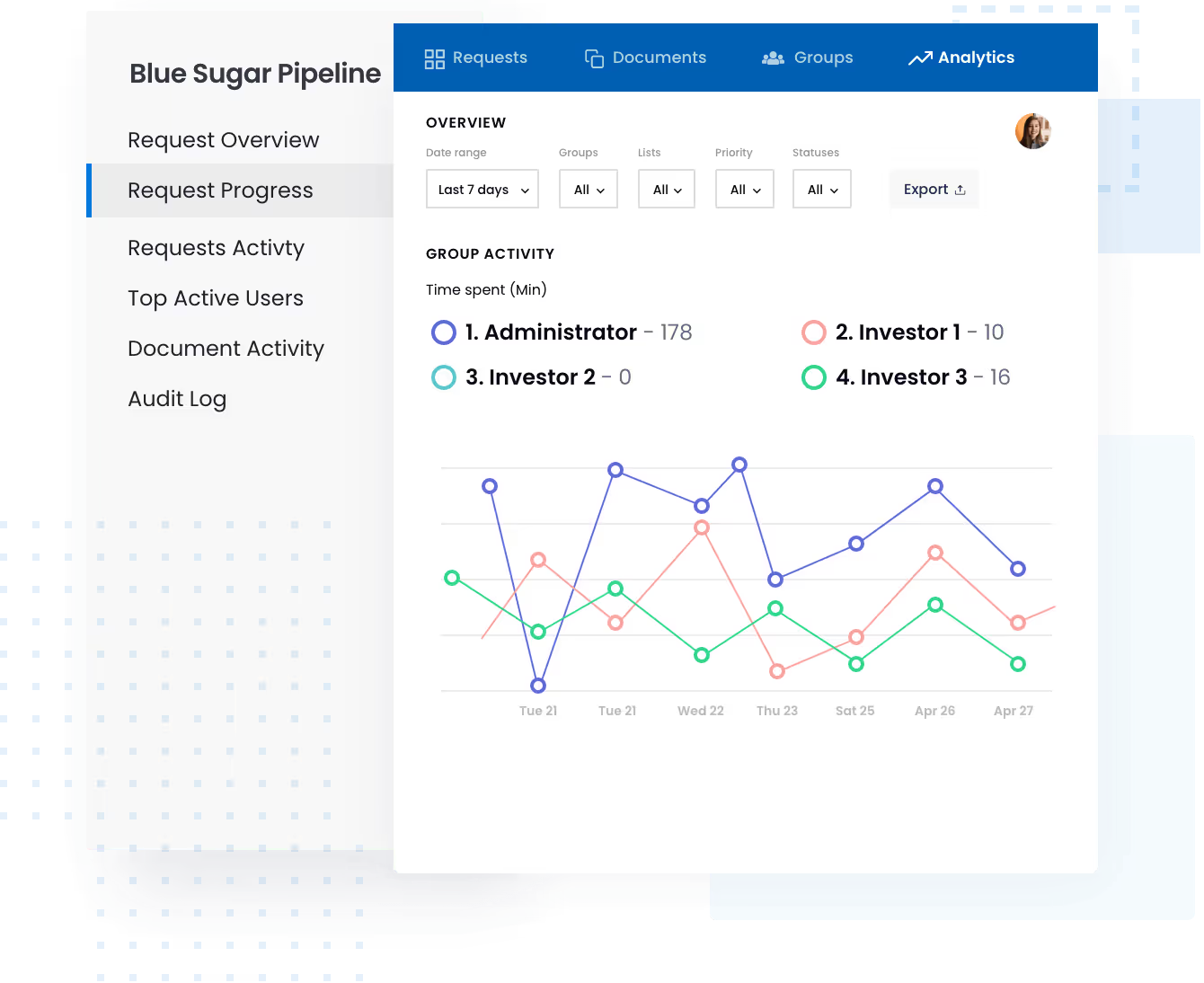

Learn from the data collected. DealRoom’s advanced analytics collect data on how everything in the room is used and by whom.

Effectively manage the process

Manage the entire divestiture lifecycle on one platform. Starting with strategy review, to deal marketing, all the way through pushing a transaction to separation management.

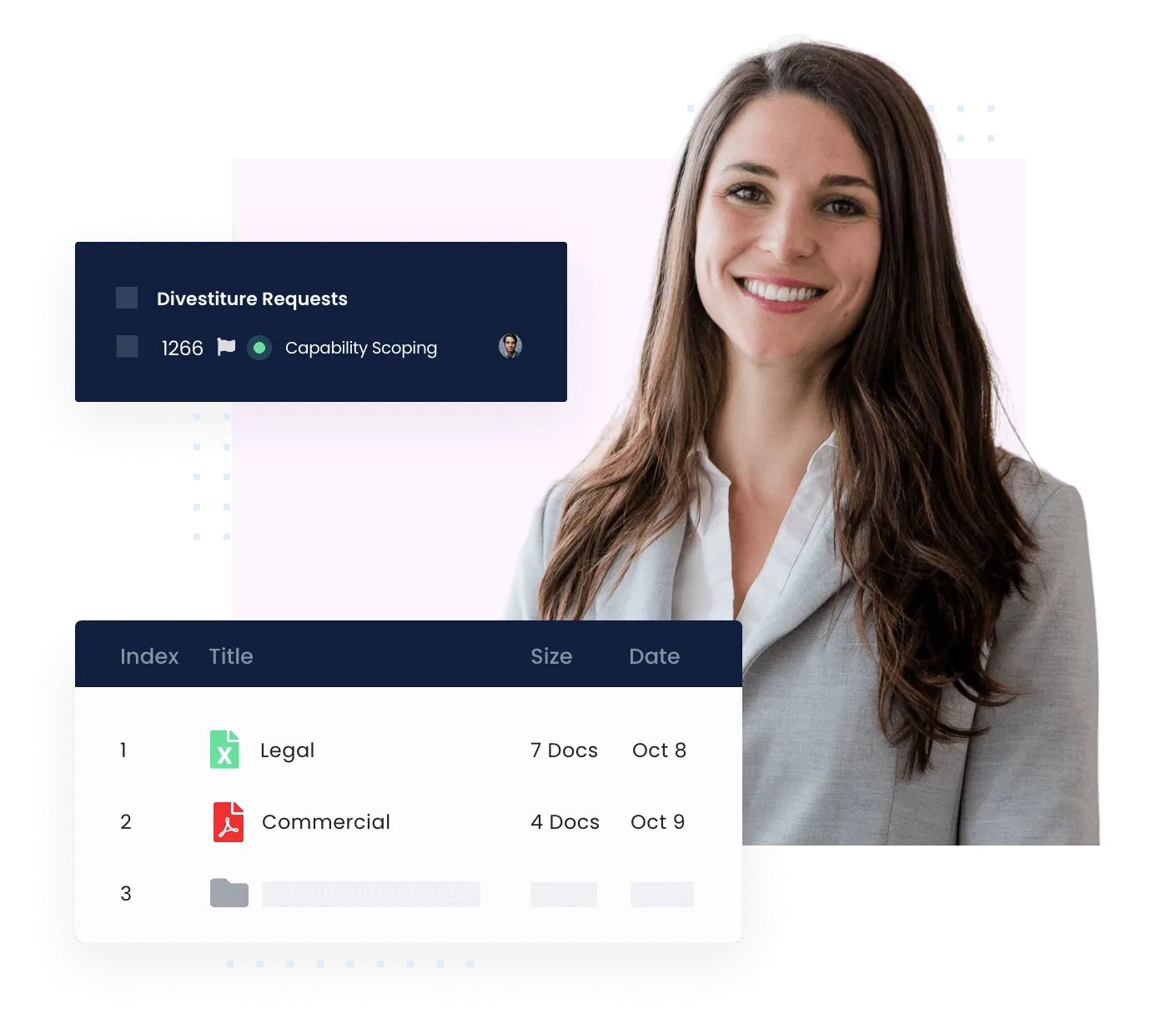

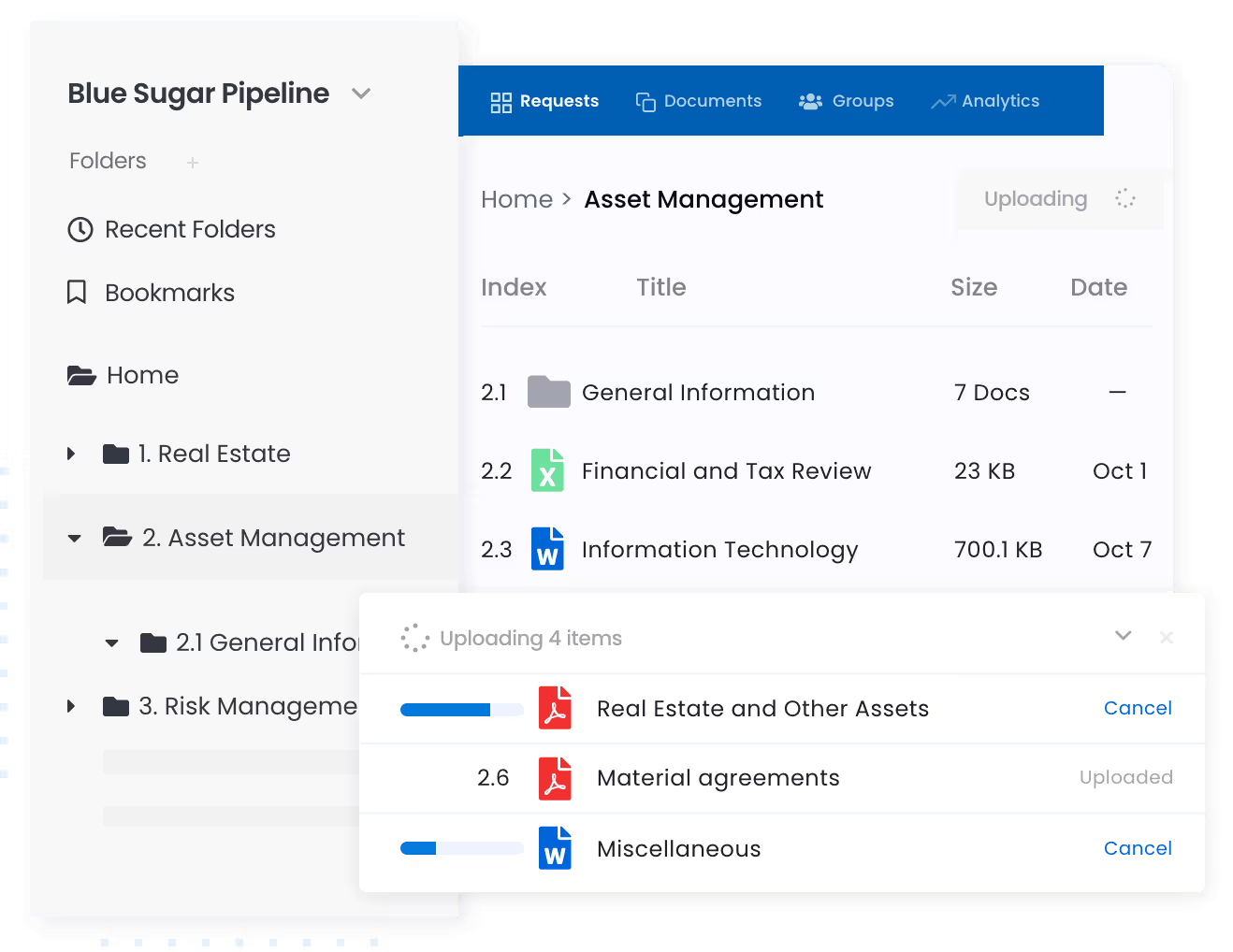

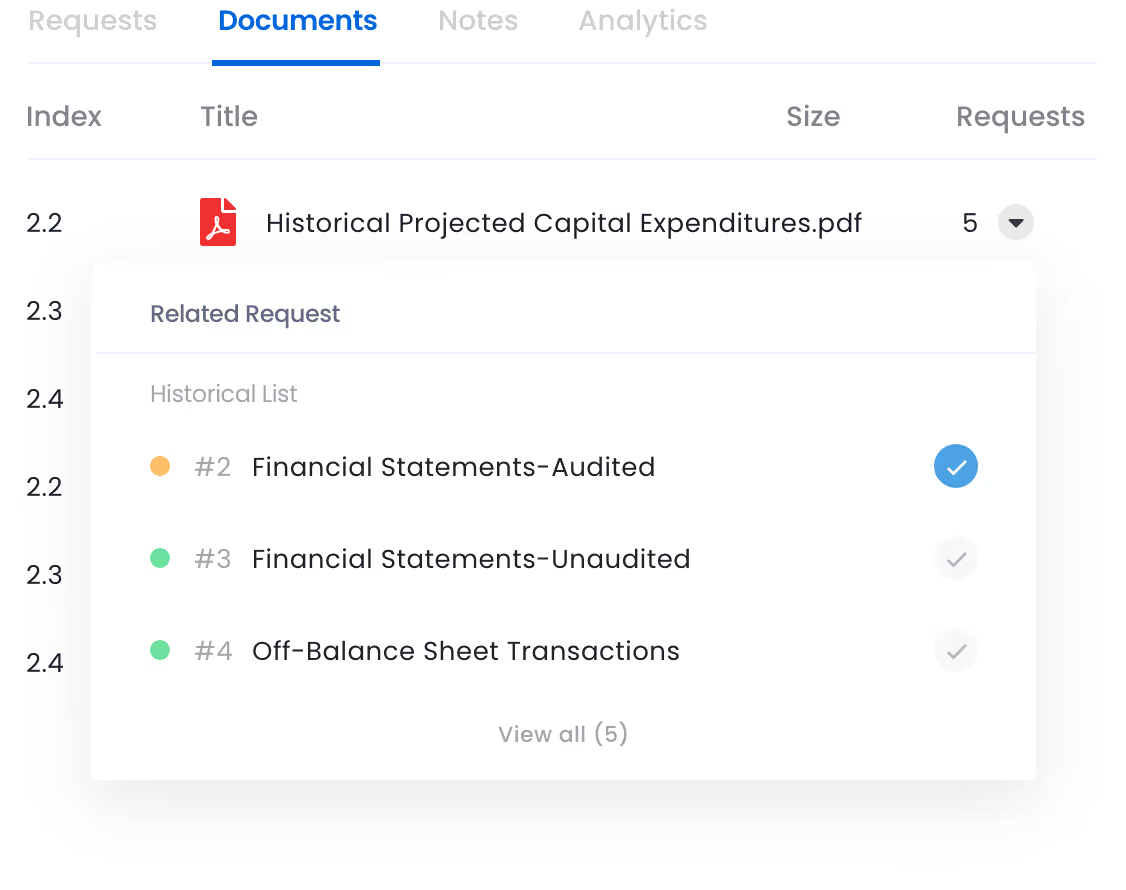

Secure documents storage & sharing

Organize and manage your documents with easy drag & drop upload, 4-levels permissions, built-in viewer, and smart notifications.

Productive diligence process

Answer diligence requests without leaving the platform since DealRoom combines diligence management with a virtual data room.

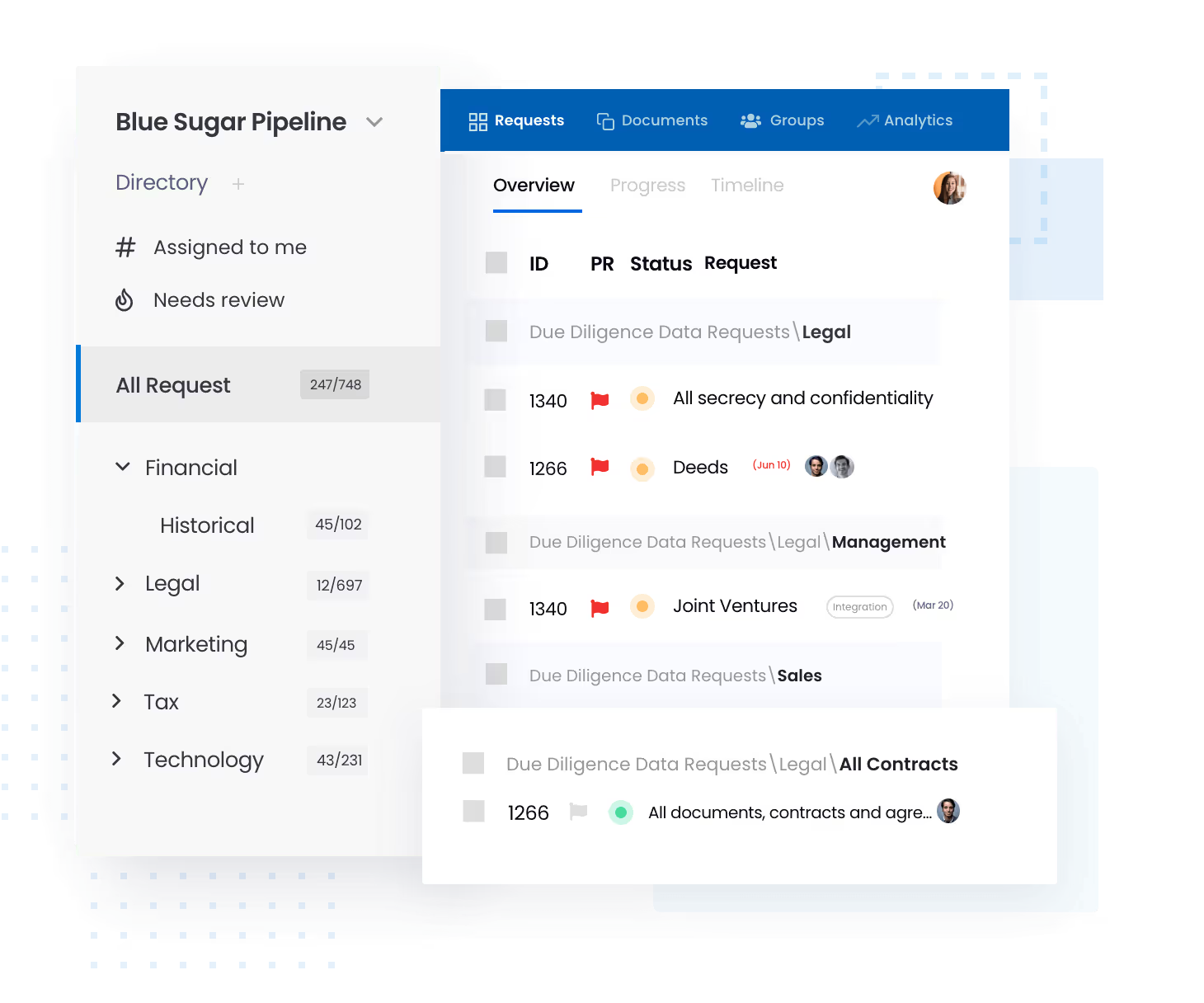

Home for buyer engagement

Potential buyers have a convenient place within DealRoom to access any information they need. They can leave new requests, collaborate in comments, review documents, and more.

Divestiture reporting as it happens

Divestiture management teams need to be aware of progress in real time. DealRoom’s analytics tab gives users insight into request, document, and user activity, as well as a detailed audit log.

Integrate with tools you already use

DealRoom can integrate with modern and useful M&A tools to further create a central hub for collaboration.

Simple and intuitive, DealRoom's interface made sharing and facilitating a breeze.

We loved the ability to loop in constituents from a variety of places to see only what they needed to see, as well as the granular level of visibility and control that made monitoring and compliance as pain-free as possible.

Financial Analyst

-2.png)

Let us optimize your deal management workflows

Tackle each aspect of the deal lifecycle with DealRoom

Pipeline

Diligence

Virtual Data Room

BI Reporting

.jpg)

.jpg)