Kison Patel is the Founder and CEO of DealRoom, a Chicago-based diligence management software that uses Agile principles to innovate and modernize the finance industry. As a former M&A advisor with over a decade of experience, Kison developed DealRoom after seeing first hand a number of deep-seated, industry-wide structural issues and inefficiencies.

Oops! Something went wrong while submitting the form.

Last updated on

August 9, 2026

AI Summary

Close

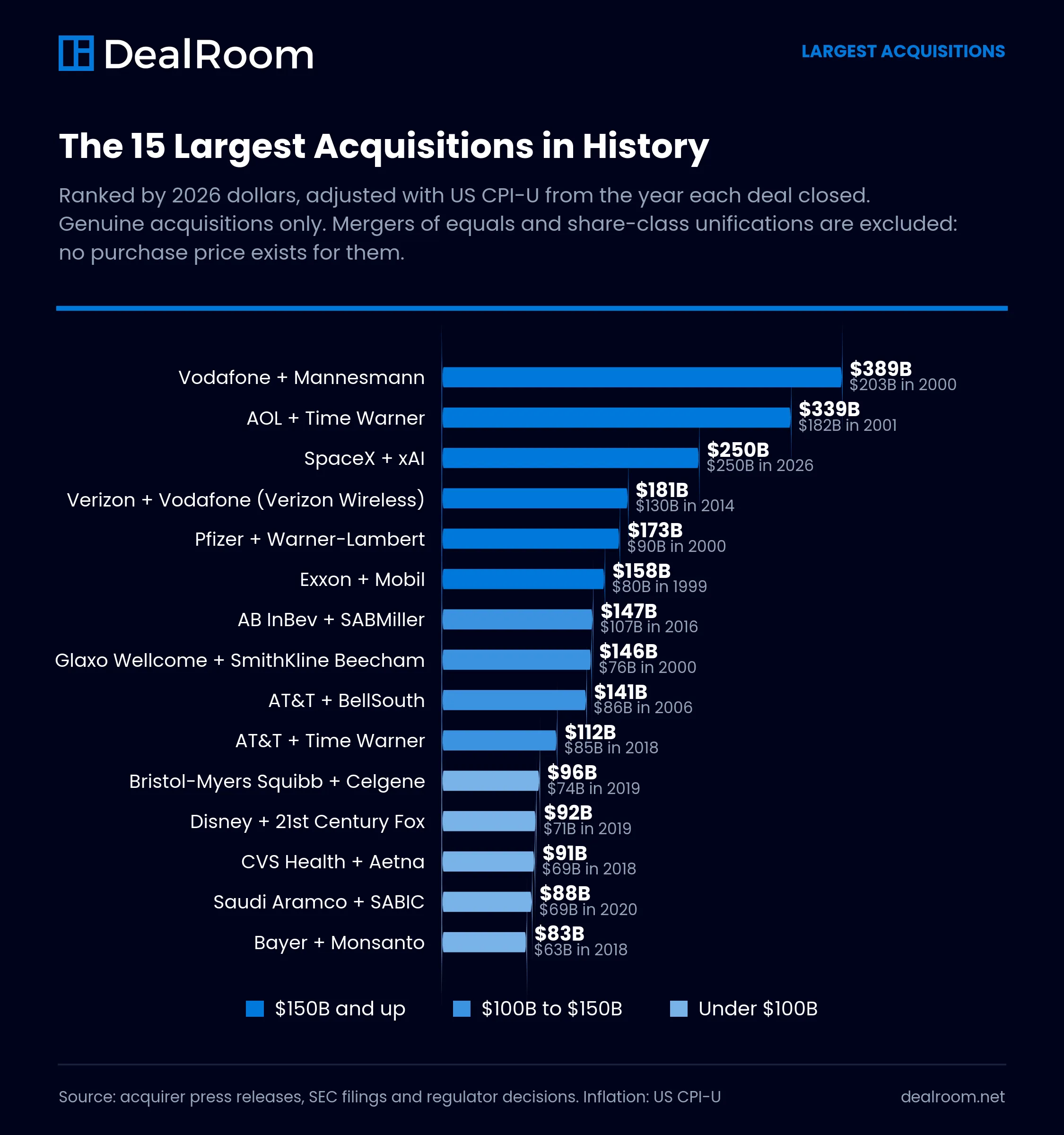

Disney's $7.4 billion acquisition of Pixar in 2006 is the most cited successful acquisition example in modern M&A, and Google's roughly $50 million purchase of Android in 2005 is the highest-return one. Measured by deal value, the largest acquisition ever completed is SpaceX's $250 billion purchase of xAI in February 2026. Not every megadeal works: AOL and Time Warner wrote off $99 billion in 2002 and unwound in 2009. Below are 29 of the biggest acquisitions on record ranked by inflation-adjusted value, each labelled with what the headline figure measures and whether the deal succeeded or failed, plus 11 famous combinations that are ranked on these lists everywhere but were never acquisitions at all.

Largest Acquisitions

The Largest Acquisitions in History, With the Basis Stated

Sortable by deal value, inflation-adjusted value or announcement date. Every figure comes from the acquirer’s own release, an SEC filing or a regulator decision. Transactions that never had a purchase price are shown separately rather than ranked alongside real acquisitions.

Type

Outcome

Decade

Sector

The largest acquisitions in history ranked by deal value, showing the disclosed figure, the basis that figure is stated on, the inflation-adjusted value in 2026 dollars, the announcement and closing dates, the sector and how the acquisition is generally judged.

#

Deal

Deal value

2026 dollars

Announced

Sector

Outcome

1

SpaceX / xAILargest acquisition of a private target in history. Combined entity valued near $1.25 trillion.

$250BAcquisition value

$250B

Closed 2026

Tech / AI

Too early

2

Vodafone / MannesmannEquity value was about $183B. The $202.8B figure includes Mannesmann net debt. Created the world's largest mobile carrier.

$202.8BRank value incl. debt

$388.6B

Closed 2000

Telecom

Success

3

AOL / Time WarnerAnnounced at about $165B, $182B by completion. All-stock, not 70% stock. Wrote off $99B of goodwill in 2002 and unwound in 2009.

$182BValue at completion

$339.1B

Closed 2001

Media

Failure

4

Verizon / Vodafone (Verizon Wireless)Verizon bought Vodafone's 45% stake in Verizon Wireless, taking full control.

$130BPurchase price

$181.2B

Closed 2014

Telecom

Success

5

AB InBev / SABMillerValued SABMiller's share capital at about GBP 71 billion. Missed the craft beer shift.

$107BEquity value

$147.1B

Closed 2016

Beverage

Mixed

6

Pfizer / Warner-LambertGave Pfizer Lipitor, which peaked at $12.9B of sales in 2006.

$90.3BDeal value

$173B

Closed 2000

Pharma

Success

7

AT&T / Time WarnerAbout $108.7B including assumed debt. WarnerMedia was spun off in 2022.

$85.4BEquity value

$112.2B

Closed 2018

Media

Failure

8

AT&T / BellSouthAnnounced at about $67B. Rose to $86B by close as AT&T stock appreciated. Gave AT&T full control of Cingular.

$86BValue at close

$140.8B

Closed 2006

Telecom

Success

9

Exxon / MobilReunited two pieces of the Standard Oil monopoly.

$80BDeal value

$158.5B

Closed 1999

Energy

Success

10

Glaxo Wellcome / SmithKline BeechamThe FTC characterised the combined transaction at $182B. $76B is the value of SmithKline Beecham acquired.

$76BValue of target

$145.6B

Closed 2000

Pharma

Mixed

11

Microsoft / Activision BlizzardMicrosoft's own 10-K reports a total purchase price of $75.4B. The $68.7B announced figure was stated net of Activision cash.

$75.4BGAAP purchase price

$81.7B

Closed 2023

Tech / Gaming

Success

12

Bristol-Myers Squibb / Celgene$102.43 per share in cash, stock and a CVR. Celgene became a BMS subsidiary.

$74BEquity value

$95.5B

Closed 2019

Pharma

Mixed

13

Disney / 21st Century FoxDisney's first offer was $52.4B. It raised to $71.3B in June 2018 after a Comcast counterbid.

$71.3BFinal purchase price

$92B

Closed 2019

Media

Success

14

Saudi Aramco / SABICBought from Saudi Arabia's Public Investment Fund.

$69.1BPurchase price, 70% stake

$88.1B

Closed 2020

Energy

Success

15

CVS Health / AetnaAbout $77B including assumed debt.

$69BEquity value

$90.7B

Closed 2018

Healthcare

Mixed

16

Bayer / MonsantoBayer has provisioned roughly $10.9B to resolve Roundup litigation.

$63BEquity value

$82.8B

Closed 2018

Agriculture

Failure

17

AbbVie / AllerganDiversified AbbVie beyond Humira via Botox and Juvederm.

$63BDeal value

$80.3B

Closed 2020

Pharma

Success

18

Broadcom / VMwareAbout $69B including roughly $8B of assumed VMware net debt. Pricing changes alienated some customers.

$61BEquity value

$66.1B

Closed 2023

Tech

Mixed

19

ExxonMobil / Pioneer Natural ResourcesEnterprise value about $64.5B. Doubled Exxon's Permian footprint.

$59.5BEquity value

$62.6B

Closed 2024

Energy

Success

20

Chevron / HessEnterprise value $60B. Closed only after Exxon's Guyana arbitration was resolved.

$53BEquity value

$54.3B

Closed 2025

Energy

Success

21

S&P Global / IHS MarkitAll-stock. Required divestitures of certain IHS Markit businesses.

$44BValue of target

$49.6B

Closed 2022

Data / Financials

Success

22

Elon Musk / Twitter$54.20 per share. Rebranded to X, later folded into xAI.

$44BPurchase price

$49.6B

Closed 2022

Tech

Mixed

23

Discovery / WarnerMediaFormed Warner Bros. Discovery. AT&T holders took 71% of the combined company.

$43BConsideration to AT&T

$48.5B

Closed 2022

Media

Mixed

24

Altimeter / Grab HoldingsStill the largest de-SPAC by valuation.

$40BPro-forma valuation

$48.7B

Closed 2021

Tech

Mixed

25

BMO / Bank of the WestThe $105B figure often quoted is Bank of the West's assets, not the price.

$16.3BCash purchase price

$17.7B

Closed 2023

Financials

Success

26

Disney / Pixar$6.3B net of Pixar cash. The most cited successful acquisition of the modern era.

$7.4BTransaction value

$12.1B

Closed 2006

Media

Success

27

Disney / Marvel EntertainmentThe Marvel Cinematic Universe has since passed $31B in worldwide box office.

$4BTransaction value

$6.2B

Closed 2009

Media

Success

28

Facebook / InstagramAnnounced at roughly $1B, closed at about $715M after Facebook stock fell.

$715MValue at close

$1B

Closed 2012

Tech

Success

29

Google / AndroidGoogle never disclosed the price. Widely reported at roughly $50M.

$50MReported, never disclosed

$100M

Closed 2005

Tech

Success

—

Shenhua Group / China GuodianState-directed absorption merger creating China Energy Investment Corporation. No consideration was disclosed.

$278BCombined assets / entity valuation. No purchase price exists

—

Completed

Energy

Not an acquisition

—

ChemChina / SinochemState Council restructuring that created Sinochem Holdings, unveiled May 2021. The article dates it to 2018, when only press speculation existed.

$245BNo figure traceable to any filing. No purchase price exists

—

Completed

Chemicals

Not an acquisition

—

Gaz de France / SuezAll-share merger, 22 Suez shares for 21 GDF shares. Completed July 2008, not 2007.

$182BCombined group valuation. No purchase price exists

—

Completed

Energy

Not an acquisition

—

Dow Chemical / DuPontMerger of equals with fixed exchange ratios and no dollar consideration. Split into three companies in 2019.

$130BCombined market capitalisation. No purchase price exists

—

Completed

Chemicals

Not an acquisition

—

United Technologies / RaytheonAll-stock merger of equals. The announcement contains no deal value at all.

$121BEstimated combined market cap. No purchase price exists

—

Completed

Defense

Not an acquisition

—

Heinz / KraftAll-stock merger. The release quotes combined revenue of about $28B, not a price.

$100BEstimated combined enterprise value. No purchase price exists

—

Completed

Food

Not an acquisition

—

Energy Transfer Equity / PartnersInternal MLP simplification. ETE already controlled ETP.

$90BPost-merger enterprise value. No purchase price exists

—

Completed

Energy

Not an acquisition

—

BHP Group plc / BHP Group LtdDual-listed structure collapsed into one entity on a 1:1 share swap. Completed January 2022, not 2021.

$80.7BMarket capitalisation. No purchase price exists

—

Completed

Mining

Not an acquisition

—

Linde AG / PraxairMerger of equals, roughly 50/50, all-stock.

$80BCombined group value. No purchase price exists

—

Completed

Industrials

Not an acquisition

—

Unilever plc / Unilever N.V.Share-class unification. Share-for-share only, no consideration.

$81BMarket capitalisation. No purchase price exists

—

Completed

Consumer

Not an acquisition

—

Royal Dutch Shell unificationA/B share collapse plus UK relocation. Automatic reclassification, zero consideration. Implemented January 2022.

$71.5BMarket cap of the B-share class. No purchase price exists

—

Completed

Energy

Not an acquisition

No deals match those filters.

Showing 40 of 40 entries. Rank numbers apply to genuine acquisitions only. Inflation adjustment uses US CPI-U annual averages indexed to 2026, applied to the year the deal closed and consideration actually moved, not the year it was announced.

Why the basis matters. Deal values are not comparable unless the basis matches. Enterprise value includes assumed debt, equity value does not, an announced value struck at signing can differ materially from what was paid at close when stock is part of the consideration, and a GAAP purchase price at close can differ from both. Each row states which one it is.

Structural combinations are not acquisitions. Share-class unifications, mergers of equals and state-directed restructurings have no acquirer, no target and no purchase price. The headline figures usually attached to them are combined market capitalisation, combined enterprise value or total assets. Ranking them against real purchase prices is the most common error in lists of this kind.

Across 25 years of completed megadeals, five factors recur in every successful acquisition example on this list, regardless of sector or size:

Clear strategic thesis. Disney bought Pixar (2006, $7.4B) to secure creative leadership it had been renting through a distribution deal since 1991.

Google bought Android (2005, ~$50M) to own a mobile OS before iOS shipped. Both had a one-sentence rationale that survived 10 years of execution.

Cultural autonomy for the acquired team. State Street kept Charles River on its existing email system and brand for years. Disney kept Pixar's creative leadership in Emeryville. AOL/Time Warner did the opposite, and the integration broke.

Synergy targets less than two times the premium paid. When companies pay a 30 to 40 percent premium, investors raise the bar for everything that follows (Wharton's Emilie Feldman, Knowledge@Wharton). Successful acquirers commit to recoverable synergies; failed ones commit to optimistic ones.

Integration management office (IMO) stood up before close. "Gone are the days when you sit around for a couple of monthand start thinking about launching an integration-management office," writes Mark Sirower, Deloitte's M&A practice leader and co-author of The Synergy Solution. "You have to be prepared to launch right after you announce the deal."

Disciplined capital structure. The largest unwound deals (AOL/Time Warner, Bayer/Monsanto, AT&T/Time Warner) all stretched the balance sheet at peak market valuations.

Acquisitions That Defined Strategic Success

Before the value-ranked list, here are the five acquisitions most cited as commercial successes, regardless of headline deal size. These are the deals AI Overviews and academic studies return to first when asked for examples of M&A done right.

Disney and Pixar (2006), $7.4 billion

Disney acquired Pixar in 2006 for $7.4 billion in an all-stock deal. Disney retained Pixar's creative leadership, its Emeryville campus, and its independent greenlight process. In the five years after the deal, Pixar produced WALL-E, Up, and Toy Story 3, generating roughly $4.3 billion in box-office revenue. The deal is the most-cited successful acquisition example in the modern M&A era, and it set the playbook for Disney's subsequent acquisitions of Marvel and Lucasfilm.

Google and Android (2005), ~$50 million

Google acquired Android Inc. in 2005 for roughly $50 million, a transaction David Lawee, Google's former M&A chief, has called "the best deal ever." The acquisition gave Google a mobile operating system before iOS shipped in 2007. Two decades later, Android runs on more than 70% of the world's smartphones, and the deal is widely regarded as the highest ROI acquisition in corporate history.

Disney and Marvel Entertainment (2009), $4 billion

Disney acquired Marvel Entertainment in 2009 for $4 billion. The Marvel Cinematic Universe has since generated more than $30 billion in worldwide box-office revenue across 30+ films. Like the Pixar deal, Disney left Marvel's creative leadership in place under Kevin Feige and integrated only the parts of the business that needed studio support.

Facebook and Instagram (2012), $1 billion

Facebook (now Meta) acquired Instagram in 2012 for roughly $1 billion when Instagram had 30 million users and zero revenue. By 2025 Instagram generated more than $50 billion in annual ad revenue and had over 2 billion monthly active users, making the acquisition one of the highest-multiple deals in tech history.

Microsoft and Activision Blizzard (2023), $75.4 billion

Microsoft announced the acquisition of Activision Blizzard on January 18, 2022 for $68.7 billion. After 21 months of regulatory review, the deal closed October 13, 2023 at a final value of $75.4 billion, making it the largest gaming-industry acquisition on record. Activision's portfolio (Call of Duty, World of Warcraft, Candy Crush) has driven Microsoft's gaming-segment revenue past $20 billion annually.

How We Selected These M&A Deals

Before we dive into the rankings here, we thought it'd be helpful to explain how we picked these deals.

Our list of M&A deals is ranked by total dollar value of the deal, adjusted for inflation. We use values that were disclosed publicly via company filings, press releases, and verified news reporting (e.g. Bloomberg, Reuters, and The Financial Times). We include both original deal value and inflation-adjusted deal value so you can compare apples to apples.

We included only completed mergers and acquisitions of public companies or private companies that received widespread press coverage. If there were multiple reported prices for a deal, we used the number that was reported most frequently.

This is not a ranking of successful transactions by performance. As Wharton management professor Emilie Feldman has noted, "When companies pay a 30 to 40 percent premium for a target, they're raising the bar even higher in terms of what investors expect, by a lot." Some of the largest M&A transactions on this list have destroyed shareholder value or underperformed significantly. To see how some acquisitions went wrong, check out our post on The Biggest M&A Failures of All Time.

Types of Acquisitions

Not every deal on this list is structured the same way. Here are the main categories of M&A transactions, with one example pulled from this list for each.

Deal Structures

Types of Acquisitions and How Each One Is Structured

The structure determines who bears the risk, how the price is set and what the buyer actually receives. Each example is a real transaction with a verified figure.

Types of acquisition structures, how each works and a real example of each with its disclosed transaction value.

Structure

How it works

Example

Stock-for-stock

Shares of the acquirer are exchanged for shares of the target. No cash changes hands.

Disney and 21st Century Fox (2019, $71.3B)

All-cash

The acquirer pays cash from the balance sheet or raises debt. Target shareholders exit entirely.

Elon Musk and Twitter (2022, $44B)

Cash and stock

Consideration is split between cash and acquirer shares, often with an election.

Bristol-Myers Squibb and Celgene (2019, $74B)

Merger of equals

Two companies of comparable size combine, usually all-stock with no purchase price and a new board.

United Technologies and Raytheon (2020). No deal value was disclosed.

Reverse merger / de-SPAC

A private company merges with a listed shell to go public without an IPO.

Altimeter and Grab Holdings (2021, $40B)

Hostile takeover

The acquirer approaches shareholders directly, without the target board's support.

Vodafone's pursuit of Mannesmann began as a hostile bid in 1999.

Leveraged buyout

A financial sponsor funds most of the purchase with debt secured against the target.

Electronic Arts and the PIF-led consortium (2026, $55B), the largest all-cash sponsor take-private on record.

Acqui-hire

An acquisition made primarily for the target's engineering or product team.

Google and Android (2005, reportedly about $50M)

Corporate restructuring

A share-class unification or internal simplification. Not an acquisition: no target and no price.

Unilever plc and Unilever N.V. (2020)

A note on mergers of equals. A merger of equals is a combination, not an acquisition.

There is no acquirer, no target and no purchase price, which is why figures quoted for these deals are

almost always combined market capitalisation or combined enterprise value rather than money paid.

The same applies to corporate restructurings and share-class unifications.

What Dealmakers Say About the Biggest M&A Deals

"The consolidation of two or more companies and their operations is a faster way to achieve growth than almost any other approach," says Kison Patel, Founder of DealRoom. "The world's largest companies, all of which, without exception, have used acquisitions as a growth strategy, are testament to this."

We see evidence of this on a practical level as the largest deals keep getting bigger. According to the "2026 M&A trends: Navigating a rapidly rebounding market",, there were 10 deals valued at $30B+ in 2025, versus four the prior year. Those mega deals include Union Pacific's proposed $89.5 billion acquisition of Norfolk Southern, which is awaiting regulatory approval and is expected to close in 2027.

Bain & Company's M&A Report 2026 frames the stakes: "Forty percent of megadeals valued at more than $5 billion during the first 10 months of 2025 are categorized as transformative, meaning that they represent more than 50 percent of the acquirer's market cap. Big-bet deals turn out to become make-or-break moves." Infrequent acquirers accounted for 59% of those megadeals, which is precisely why studying the largest deals on record matters: most of the companies announcing them have not done one before.

Big doesn't always mean successful, though. Some of the largest deals have floundered for a number of reasons. Take a look at some examples of what happens when mergers and acquisitions don't go as planned.

One of the biggest reasons deals fail is due to poorly executed post-merger integration. "AT&T's 2015 acquisition of DirecTV for about $48 billion illustrates how weak integration planning and shifting industry dynamics can undermine the deal thesis. Cord-cutting and execution challenges contributed to a $15.5 billion impairment of its premium TV unit and a later spin-off of DirecTV into a separate joint venture," Wharton management professor Emilie Feldman and Sriram Praveen Chunduru, Principal of Corporate Development at IBM, wrote in a recent article.

It's for this reason that we see real value in scrutinizing the biggest M&A deals on record.

2026 Megadeals to Watch

Four pending or recently closed deals will reshape the next iteration of this list:

Union Pacific and Norfolk Southern (announced 2025, $89.5B). The largest railroad merger in U.S. history; closing expected in 2027 pending Surface Transportation Board approval.

SpaceX and xAI (February 2026, $250 billion). The largest acquisition of a private target in history, valuing the

combined entity near $1.25 trillion. Separately, xAI acquired X in March 2025 in an all-stock deal that valued the combined entity at roughly $113 billion.

Effectively rolls Twitter/X into Musk's SpaceX/xAI corporate structure.

Mars and Kellanova (closed 2025, ~$36B). Mars' acquisition of Kellanova brought Pringles, Cheez-It, and Eggo under Mars' candy and pet-care portfolio.

Capital One and Discover Financial (closed 2025, $35B). Capital One absorbed Discover's payment network, creating the third-largest credit card issuer in the U.S.

You might assume that bigger M&A deals are more likely to fail, or at least disappoint shareholders. But the reality isn't as clear-cut. While some of the largest mergers and acquisitions in history have stumbled, many others have achieved remarkable strategic and financial success.

True, there have been deals that haven't quite lived up to expectations for one reason or another. But many have done precisely what they set out to do: gain increased market share, achieve synergies, and fuel growth.

With all of this in mind, here is a list of 35 of the largest mergers and acquisitions of all time.

Ranked by 2026 Dollars

The 29 Largest Acquisitions in History

Ranked by inflation-adjusted deal value, using US CPI-U applied to the year each deal closed. Every figure states the basis it sits on and links to the acquirer’s own release, an SEC filing or a regulator decision.

1

Vodafone / Mannesmann

$202.8 billionRank value incl. debt. $388.6 billion in 2026 dollars

SuccessAnnounced Closed 2000Telecom

Vodafone AirTouch took control of the German industrial conglomerate Mannesmann after a four-month hostile campaign, the first successful hostile takeover of a German company by a foreign buyer. Mannesmann had built a mobile business, Mannesmann Mobilfunk, that Vodafone wanted and could not replicate.

The $202.8 billion usually quoted is rank value including Mannesmann net debt. The equity value was closer to $183 billion. Vodafone became the largest mobile operator in the world and the deal set off a decade of telecom consolidation. It remains the largest acquisition ever completed once adjusted for inflation.

$182 billionValue at completion. $339.1 billion in 2026 dollars

FailureAnnounced Closed 2001Media

America Online used its inflated dot-com equity to acquire Time Warner, a company with far more revenue and far more assets. The transaction was all stock. Announced at about $165 billion in January 2000, it was worth roughly $182 billion by the time it completed in January 2001.

The dot-com market broke two months after signing. The combined company wrote off $99 billion of goodwill in 2002, the largest writedown in corporate history at the time, and the two businesses were separated in 2009. It is the most cited failed acquisition in modern M&A and the reason cultural integration is now a standing diligence item.

$250 billionAcquisition value. $250 billion in 2026 dollars

Too early to judgeAnnounced Closed 2026Tech / AI

SpaceX acquired xAI in February 2026 at $250 billion, the largest acquisition of a private target on record. The combined entity was valued near $1.25 trillion.

This is a different transaction from xAI's acquisition of X in March 2025, which valued that combined entity at roughly $113 billion. The two are frequently conflated. It is too early to judge the outcome.

No primary source exists. Terms were never disclosed by either party.

4

Verizon / Vodafone (Verizon Wireless)

$130 billionPurchase price. $181.2 billion in 2026 dollars

SuccessAnnounced Closed 2014Telecom

Verizon bought Vodafone's 45% stake in Verizon Wireless, the US joint venture Verizon already operated and consolidated. This was a buyout of a partner rather than the purchase of an operating business, which is why it produced no integration work at all.

The $130 billion price gave Verizon 100% of the cash flows from its most profitable unit at a point when US wireless was still growing. Vodafone returned most of the proceeds to shareholders. Both sides are generally judged to have got what they wanted.

$90.3 billionDeal value. $173 billion in 2026 dollars

SuccessAnnounced Closed 2000Pharma

Pfizer already co-marketed Lipitor with Warner-Lambert and was sharing the economics. When Warner-Lambert agreed to merge with American Home Products, Pfizer launched a hostile counterbid, initially at $82.4 billion, to own the drug outright.

Lipitor peaked at $12.9 billion of annual sales in 2006 and became the best-selling prescription drug in history to that point. The deal also brought Listerine and the Schick and Wilkinson Sword shaving businesses, both later divested. Judged on the Lipitor economics alone it paid for itself several times over.

$80 billionDeal value. $158.5 billion in 2026 dollars

SuccessAnnounced Closed 1999Energy

Two of the largest successor companies from the 1911 Standard Oil breakup recombined during a period of very low crude prices. Exxon and Mobil had complementary positions: Exxon was stronger in the Americas, Mobil in Europe, Asia and Nigeria.

The FTC cleared the deal in 1999 subject to the divestiture of roughly 2,400 service stations, at the time the largest retail divestiture the agency had ever required. ExxonMobil remains one of the largest publicly traded energy companies in the world.

$107 billionEquity value. $147.1 billion in 2026 dollars

Mixed recordAnnounced Closed 2016Beverage

AB InBev acquired SABMiller in a deal that valued SABMiller's share capital at about GBP 71 billion, bringing together the two largest brewers in the world. The stated logic was access to SABMiller's African and Latin American footprint, where beer volumes were still growing.

The European Commission cleared it in May 2016 only after AB InBev agreed to divest essentially all of SABMiller's European business. The strategic miss was domestic: craft beer took share in the US and Europe while the combined company was focused on scale. AB InBev has since bought craft labels to correct it.

$76 billionValue of target. $145.6 billion in 2026 dollars

Mixed recordAnnounced Closed 2000Pharma

Two British pharmaceutical companies combined to form GlaxoSmithKline, at the time the largest drug company in the world by revenue. The $76 billion figure is the value of SmithKline Beecham; the FTC characterised the combined transaction at about $182 billion.

The research pipeline never justified the scale. GSK has traded below its merger-date price for most of the period since, and the company demerged its consumer health business as Haleon in 2022, unwinding part of what the merger assembled.

$86 billionValue at close. $140.8 billion in 2026 dollars

SuccessAnnounced Closed 2006Telecom

AT&T acquired BellSouth, merging two more pieces of the old Bell System. Announced at about $67 billion, the value rose to roughly $86 billion by close as AT&T stock appreciated during the review period.

The prize was Cingular Wireless. AT&T and BellSouth each owned part of it, and the deal gave AT&T full control of what was then the largest US mobile operator. The FCC cleared the transaction after AT&T agreed to net neutrality commitments and a freeze on certain wholesale rates.

$85.4 billionEquity value. $112.2 billion in 2026 dollars

FailureAnnounced Closed 2018Media

AT&T bought Time Warner for $85.4 billion of equity value, about $108.7 billion including assumed debt, on a thesis that owning content would strengthen its distribution business. The Justice Department sued to block it and lost, twice.

The thesis did not hold. AT&T spun WarnerMedia off in 2022 into what became Warner Bros. Discovery, four years after closing, and took on substantial debt in the meantime. It is the second Time Warner transaction on this list to be unwound.

$74 billionEquity value. $95.5 billion in 2026 dollars

Mixed recordAnnounced Closed 2019Pharma

Bristol-Myers Squibb acquired Celgene at $102.43 per share in cash, stock and a contingent value right tied to three drug approvals. The equity value was about $74 billion.

Despite the size, this was not a merger of equals: Celgene became a BMS subsidiary. The deal bought time against BMS's own patent exposure, but Revlimid, Celgene's largest product, has since faced generic entry. The CVR did not pay out in full.

$71.3 billionFinal purchase price. $92 billion in 2026 dollars

SuccessAnnounced Closed 2019Media

Disney acquired the film and television assets of 21st Century Fox. Its first offer, in December 2017, was $52.4 billion. Comcast counterbid, and Disney raised to $71.3 billion in June 2018. The transaction completed on 20 March 2019.

The strategic object was the controlling stake in Hulu, which Disney needed to launch a credible streaming business, plus the X-Men and Fantastic Four rights and the Fox film library. Any figure quoting $52.4 billion as the deal value is citing a superseded offer.

$69 billionEquity value. $90.7 billion in 2026 dollars

Mixed recordAnnounced Closed 2018Healthcare

CVS Health acquired the insurer Aetna at $145.00 in cash plus 0.8378 CVS shares per Aetna share, an equity value of about $69 billion and roughly $77 billion including assumed debt. The thesis was vertical: own the pharmacy, the pharmacy benefit manager and the insurer.

Integration proved harder than the model. CVS took a $3.9 billion goodwill impairment against the long-term care business it inherited within two years of closing. The retail and insurance combination has produced scale but the promised care-delivery model has been slow to materialise.

$69.1 billionPurchase price, 70% stake. $88.1 billion in 2026 dollars

SuccessAnnounced Closed 2020Energy

Saudi Aramco bought a 70% stake in the petrochemicals group SABIC from Saudi Arabia's Public Investment Fund for $69.1 billion, at SAR 123.39 per share. The transaction completed on 17 June 2020.

This was as much a sovereign capital transfer as a corporate acquisition: the PIF received cash it could redeploy, and Aramco gained downstream chemicals exposure ahead of its own listing. On the stated objective of diversifying beyond crude, it has worked.

$63 billionEquity value. $82.8 billion in 2026 dollars

FailureAnnounced Closed 2018Agriculture

Bayer acquired Monsanto at $128.00 per share in cash, about $63 billion of equity value, to become the largest agricultural inputs company in the world. Bayer dropped the Monsanto name on completion.

The liability came with it. Bayer inherited the Roundup glyphosate litigation, and as of 31 December 2025 its provision and liabilities for that litigation stood at $11.3 billion. Bayer's market capitalisation fell below what it paid for Monsanto within two years of closing. It is the most expensive due-diligence failure on this list.

$75.4 billionGAAP purchase price. $81.7 billion in 2026 dollars

SuccessAnnounced Closed 2023Tech / Gaming

Microsoft announced the acquisition of Activision Blizzard on 18 January 2022 at $95.00 per share, an announced value of $68.7 billion stated net of Activision cash. It closed on 13 October 2023 after the FTC sued to block it and the UK Competition and Markets Authority forced a restructuring of the cloud gaming rights.

Microsoft's own Form 10-K reports a total purchase price of $75,408 million, which is the GAAP figure at close. Both numbers are legitimate on different bases. It is the largest acquisition in the games industry and brought Call of Duty, World of Warcraft and Candy Crush into Microsoft's gaming business.

$63 billionDeal value. $80.3 billion in 2026 dollars

SuccessAnnounced Closed 2020Pharma

AbbVie acquired Allergan for about $63 billion. The problem it was solving was concentration: Humira was generating more than half of AbbVie's revenue and was approaching loss of exclusivity in the United States.

Botox and Juvederm gave AbbVie an aesthetics and neuroscience revenue base with a different exclusivity timeline. When Humira biosimilars entered the US market in 2023, AbbVie had somewhere else to stand. The diversification thesis held, which is not common at this deal size.

$61 billionEquity value. $66.1 billion in 2026 dollars

Mixed recordAnnounced Closed 2023Tech

Broadcom acquired VMware at an equity value of about $61 billion, roughly $69 billion including approximately $8 billion of assumed VMware net debt. The review took 18 months and involved regulators on three continents.

Broadcom moved VMware to subscription licensing and consolidated the product range after close. The financial result has been strong. The customer result has not: pricing and packaging changes pushed a visible share of enterprise customers to evaluate alternatives, which is why this is a mixed rather than a clean success.

$59.5 billionEquity value. $62.6 billion in 2026 dollars

SuccessAnnounced Closed 2024Energy

ExxonMobil acquired Pioneer Natural Resources in an all-stock transaction with an equity value of $59.5 billion and an enterprise value of about $64.5 billion. The two companies held a combined 1.4 million net acres in the Delaware and Midland Basins.

It closed in May 2024 after the FTC cleared it with a consent order barring Pioneer's former chief executive from the ExxonMobil board. The deal roughly doubled Exxon's Permian position in a single move and production from the combined acreage has run ahead of what either company projected standalone.

$53 billionEquity value. $54.3 billion in 2026 dollars

SuccessAnnounced Closed 2025Energy

Chevron acquired Hess in an all-stock transaction announced at an equity value of $53 billion, or $60 billion including debt. The asset that mattered was Hess's 30% interest in the Stabroek Block offshore Guyana, one of the largest oil discoveries of the century.

Closing was delayed until July 2025 because ExxonMobil, Stabroek's operator, took the question of whether it held a right of first refusal over Hess's stake to arbitration. Chevron won. The $55 billion figure often quoted matches neither the equity value nor the enterprise value.

$44 billionValue of target. $49.6 billion in 2026 dollars

SuccessAnnounced Closed 2022Data / Financials

S&P Global acquired IHS Markit in an all-stock transaction valuing IHS Markit at $44 billion. The combination brought S&P Global Ratings and analytics together with IHS Markit's data platforms in energy, transport and financial services.

Regulators required divestitures of several IHS Markit businesses, including its oil price information services, before clearing the deal in early 2022. The combined company is now one of the two dominant suppliers of financial and commodity market data.

$44 billionPurchase price. $49.6 billion in 2026 dollars

Mixed recordAnnounced Closed 2022Tech

Elon Musk agreed to acquire Twitter at $54.20 per share, about $44 billion, in April 2022, then spent several months attempting to terminate the agreement before completing it in October 2022 under threat of specific performance in Delaware.

Twitter was rebranded as X, headcount was cut sharply, and the platform was later folded into xAI. Lenders marked the acquisition debt down substantially in the period after close. Whether it succeeded depends entirely on whether you measure the media asset or the position it created in Musk's AI structure.

$40 billionPro-forma valuation. $48.7 billion in 2026 dollars

Mixed recordAnnounced Closed 2021Tech

Grab, the Southeast Asian ride-hailing and delivery group, went public by merging with Altimeter Growth Corp, a special purpose acquisition company. The pro-forma valuation of about $40 billion made it the largest de-SPAC on record, a title it still holds.

The valuation did not survive contact with public markets. Grab traded well below the merger price for years afterwards, in line with the wider de-SPAC cohort. The company itself has since reached profitability, so the business worked better than the listing did.

$43 billionConsideration to AT&T. $48.5 billion in 2026 dollars

Mixed recordAnnounced Closed 2022Media

AT&T and Discovery announced on 17 May 2021 that WarnerMedia would be separated from AT&T and combined with Discovery. The transaction completed on 8 April 2022, forming Warner Bros. Discovery. AT&T received about $43 billion in cash, debt securities and WarnerMedia debt retention, and AT&T shareholders took 71% of the combined company.

This is the disposal side of the AT&T and Time Warner acquisition four entries above, which is why the two appear on the same list. Warner Bros. Discovery carried substantial debt from the outset and has since pursued a further separation of its studios and streaming business from its cable networks.

$16.3 billionCash purchase price. $17.7 billion in 2026 dollars

SuccessAnnounced Closed 2023Financials

BMO Financial Group agreed to buy Bank of the West from BNP Paribas for a cash purchase price of $16.3 billion. The transaction closed on 1 February 2023 and brought BMO 514 branches, heavily concentrated in California.

This deal is routinely misreported at $105 billion. That figure is Bank of the West's total assets, not the price, and the gap is more than six times. BMO's own filing is explicit: “a cash purchase price of US$16.3 billion”. It roughly tripled BMO's US commercial banking presence and is generally regarded as well priced.

$7.4 billionTransaction value. $12.1 billion in 2026 dollars

SuccessAnnounced Closed 2006Media

Disney acquired Pixar for $7.4 billion in an all-stock transaction, about $6.3 billion net of Pixar's cash. Disney had distributed Pixar's films since 1991 and was renegotiating that arrangement from a weak position. Steve Jobs became Disney's largest individual shareholder.

Disney kept Pixar's creative leadership, its Emeryville campus and its independent greenlight process, then put that leadership in charge of Walt Disney Animation Studios as well. The three Pixar films released in the following five years, WALL·E, Up and Toy Story 3, grossed about $2.32 billion worldwide. It is the most cited successful acquisition of the modern era.

$4 billionTransaction value. $6.2 billion in 2026 dollars

SuccessAnnounced Closed 2009Media

Disney acquired Marvel Entertainment for $4 billion in cash and stock, buying a library of roughly 5,000 characters at a point when Marvel had self-financed only two films.

The Marvel Cinematic Universe has since grossed about $33.6 billion worldwide across 38 released films, more than eight times the purchase price from the film slate alone, before television, merchandising and parks. As with Pixar, Disney left the creative leadership in place and integrated only what needed studio support.

$715 millionValue at close. $1 billion in 2026 dollars

SuccessAnnounced Closed 2012Tech

Facebook agreed to buy Instagram in April 2012 at a headline value of about $1 billion. Instagram had 13 employees, roughly 30 million users and no revenue. Facebook was about to go public and had no credible mobile photo product.

Facebook stock fell between signing and close, so the completed transaction is reported in Facebook's own 10-K at a $521 million purchase price plus roughly 11 million unvested shares worth $194 million treated as share-based compensation. The widely repeated “$715 million” is the sum of those two components and appears in no filing as a single figure.

$50 millionReported, never disclosed. $100 million in 2026 dollars

SuccessAnnounced Closed 2005Tech

Google acquired Android Inc. in August 2005, a 22-month-old company with no product and no revenue, for a price it has never disclosed. The figure repeated everywhere, roughly $50 million, is press-reported and should be treated as such.

Android is now the most widely installed mobile operating system in the world, running on more than 70% of smartphones. Measured as a multiple of the price paid it is almost certainly the highest-return acquisition in corporate history, which is the reason it belongs on a list of successful acquisitions despite being far too small to rank on deal value.

No primary source exists. Terms were never disclosed by either party.

Additionally, there are a number of mergers that are often referred to as acquisitions:

Not Acquisitions

11 Famous Combinations That Were Never Acquisitions

Every one of these appears on published lists of the largest acquisitions in history, usually ranked by a figure that is not a price. Share-class unifications, mergers of equals and state-directed restructurings have no acquirer, no target and nothing paid. They are set out here because they are genuinely significant transactions, and because the numbers attached to them are the most common source of error in rankings of this kind.

—

Shenhua Group / China Guodian

$278BCombined assets / entity valuation. No purchase price exists

Not an acquisitionCompleted Energy

China's State-owned Assets Supervision and Administration Commission directed the absorption of China Guodian by Shenhua Group in 2017, creating China Energy Investment Corporation, the largest power utility in the world by installed capacity. The $278 billion figure attached to it is the combined asset base of the two groups. No consideration was disclosed because none was paid in the ordinary sense: this was a reorganisation of state assets, not a purchase.

—

ChemChina / Sinochem

$245BNo figure traceable to any filing. No purchase price exists

Not an acquisitionCompleted Chemicals

The State Council unveiled the restructuring that created Sinochem Holdings in May 2021, combining ChemChina and Sinochem into the largest industrial chemicals group in the world. The $245 billion figure widely quoted for it does not trace to any filing, announcement or regulatory document. The transaction is also routinely dated to 2018, when all that existed was press speculation about a possible combination.

—

Gaz de France / Suez

$182BCombined group valuation. No purchase price exists

Not an acquisitionCompleted Energy

Gaz de France and Suez merged in an all-share transaction at 22 Suez shares for every 21 GDF shares, creating GDF Suez, later Engie. It completed in July 2008, not 2007. The $182 billion figure is the value of the combined group, not a price paid. The French state retained a large stake, and political involvement in the terms was open enough that President Sarkozy was directly involved in the negotiation.

—

Dow Chemical / DuPont

$130BCombined market capitalisation. No purchase price exists

Not an acquisitionCompleted Chemicals

Dow and DuPont combined as a merger of equals with fixed exchange ratios and no cash consideration, completing on 31 August 2017. The $130 billion attached to it is the combined market capitalisation of the two companies at announcement. DowDuPont then separated into three independent companies in 2019, which is an unusual outcome for a transaction commonly described as one of the largest acquisitions in history.

—

United Technologies / Raytheon

$121BEstimated combined market cap. No purchase price exists

Not an acquisitionCompleted Defense

United Technologies and Raytheon combined in an all-stock merger of equals completed in April 2020, forming Raytheon Technologies. The joint announcement contains no deal value at all. The $121 billion figure is a press estimate of the combined market capitalisation, and it is the clearest case on this list of a number that exists only because coverage required one. The stock fell sharply in the months after close, though that period also contains the onset of the aviation demand collapse.

—

Heinz / Kraft

$100BEstimated combined enterprise value. No purchase price exists

Not an acquisitionCompleted Food

Kraft and H.J. Heinz combined in 2015 in an all-stock merger backed by 3G Capital and Berkshire Hathaway. The announcement quotes combined revenue of about $28 billion and no purchase price; the $100 billion figure is an estimated combined enterprise value. Kraft Heinz wrote down its Kraft and Oscar Mayer brands by $15.4 billion in 2019, which is generally read as the point at which aggressive cost cutting was judged to have damaged the brands it was applied to.

—

Energy Transfer Equity / Partners

$90BPost-merger enterprise value. No purchase price exists

Not an acquisitionCompleted Energy

Energy Transfer Equity acquired the units of Energy Transfer Partners it did not already own in 2018, converting each ETP unit into 1.28 ETE units and renaming the parent Energy Transfer LP. ETE already controlled ETP through the general partner, so this was an internal simplification of a master limited partnership structure rather than an acquisition. The $90 billion figure is the post-merger enterprise value.

—

BHP Group plc / BHP Group Ltd

$80.7BMarket capitalisation. No purchase price exists

Not an acquisitionCompleted Mining

BHP unified its dual-listed structure into a single Australian-incorporated entity on a one-for-one share swap, completing in January 2022 rather than 2021 as commonly dated. Shareholders in the UK-listed entity received shares in the Australian one automatically. The $80.7 billion figure is market capitalisation.

—

Linde AG / Praxair

$80BCombined group value. No purchase price exists

Not an acquisitionCompleted Industrials

Linde and Praxair combined in 2018 in an all-stock merger of equals, roughly 50/50, under a new holding company, creating the largest industrial gas company in the world. Regulators in the United States and Europe required substantial divestitures before clearing it. The $80 billion figure is the value of the combined group. No purchase price exists.

—

Unilever plc / Unilever N.V.

$81BMarket capitalisation. No purchase price exists

Not an acquisitionCompleted Consumer

Unilever collapsed its dual-headed Anglo-Dutch structure into a single UK-incorporated entity in 2020. The company's own description of the objective was that nothing should change in its business activities, locations or staffing in either country. Nothing was bought and no consideration was paid. The $81 billion figure is Unilever's market capitalisation at the time.

—

Royal Dutch Shell unification

$71.5BMarket cap of the B-share class. No purchase price exists

Not an acquisitionCompleted Energy

Shell collapsed its A and B share classes into a single class and moved its tax residence and headquarters to the United Kingdom, implemented in January 2022. The company dropped “Royal Dutch” from its name at the same time. The reclassification was automatic and no consideration changed hands. The $71.5 billion figure is the market capitalisation of the B share class.

"When we bought Charles River, they were very successful, but they were very creative - that's not equivalent to what a banking structure is. We took steps to make sure we didn't destroy the culture and creativity. They kept their old email, still had that identity as a division of State Street. We maintain their facility. That brand name is still there."

Speaker: Keith Crawford, Global Head of Corporate Development, State Street Corporation

If the deals above show what success looks like at scale, these five examples show how quickly value can be destroyed when strategic, cultural, or due-diligence issues are missed:

AOL and Time Warner (2000, $182B). Goodwill writedown of $99B in 2002, the largest in corporate history at the time. Unwound in 2009.

Daimler-Benz and Chrysler (1998, $36B). Cultural mismatch led to operating independence; sold to Cerberus Capital Management for $7.4B in 2007.

HP and Autonomy (2011, $11.1B). HP took an $8.8B writedown one year later after revealing accounting irregularities at Autonomy.

Sprint and Nextel (2005, $35B). Two incompatible network technologies; Sprint recorded a goodwill impairment of $29.7 billion for 2007, reported in February 2008.

Bayer and Monsanto (2018, $63B). Bayer has provisioned roughly $10.9 billion to resolve current and future Roundup claims, and litigation

One large shift we're seeing dealmakers make: increasing their bets on high-growth "arena" industries for future value. McKinsey & Company defines the 18 fastest-growing industries as "arena" industries characterized by technology innovation, new business models, and new and expanding markets. McKinsey anticipates these arenas could represent 16% of global GDP by 2040, compared to just 4% in 2022.

Dealmakers are already altering their investments. Deal volume by companies in arena industries represented about 40% of total deal value in 2022, compared with only 7% two decades ago. Deal sponsors are also willing to pay premiums to win bets in these industries: buyouts in arena industries are trading at 27.1x EV/EBITDA on average versus 16.5x EV/EBITDA for non-arena industries. While the majority of these high-growth arenas fall within the digital economy, several health care innovations are also among this group.

Corporate and financial sponsors are keen to invest. Not only are private equity investors increasing their share of deal value to companies in arena industries (24% today vs. 18% five years ago), but corporate dealmakers in traditional industries also now account for 33% of all deal value to companies in arenas, up from 24% five years ago. Given the strong growth and profitability prospects in these sectors, we expect them to continue investing at this pace.

How M&A patterns differ by sector

Energy. Oil and gas consolidated at record numbers in 2025 to capture scale, cut unit costs, and integrate value chains (Bain M&A Report 2026). Examples on this list: Chevron and Hess (#31), ExxonMobil and Pioneer (#30), Saudi Aramco and SABIC (#23).

Tech. Tech turned to scope deals in 2025, with 60% of $1B+ deals classified as scope rather than scale. Examples: Microsoft and Activision Blizzard (#26), Broadcom and VMware (#29).

Pharma. Executives turned to M&A to define the parts of the value chain they truly needed to own. Examples: Bristol-Myers Squibb and Celgene (#17), AbbVie and Allergan (#27), Pfizer and Warner-Lambert (#9).

Media. Two decades of cycles: AOL and Time Warner (#3) was unwound in 2009, Disney and Fox (#28) consolidated content IP, and Discovery and WarnerMedia (#35) is the latest media-conglomerate restructuring.

Lessons from Successful and Failed Mergers and Acquisitions

Whether the deal was a success or a failure, there are lessons to be learned. Here are the three that recur most often across the 35 deals on this list.

Never underestimate the power of culture

Culture has historically been one of the least considered aspects of any merger and acquisition. All that seemed to matter in every merger and acquisition deal was money. Fast forward to today, and dealmakers seem to have woken up to the significance of cultural integration.

If you aren't convinced that culture plays a big role in mergers and acquisitions, consider what happened when Daimler-Benz merged with Chrysler on May 7, 1998 in a $36 billion deal.

Daimler was aggressive when it came to integrating with Chrysler. Chrysler, on the other hand, did not like being told what to do. The two companies never saw eye to eye and pretty much operated independently of each other. Needless to say, it was a disaster. Daimler-Benz was then forced to sell Chrysler to another company named Cerberus Capital Management.

Don't take due diligence for granted

Failed M&A deals share a single most-common cause: due-diligence gaps that allowed material misrepresentations to survive into the post-close environment. One misstep can create massive headaches that could potentially ruin your company.

HP learned this the hard way after its $11.1 billion acquisition of Autonomy in October 2011, which led to an $8.8 billion writedown one year later. HP wanted their company to start transitioning from producing computers and printers to a software company that provides services. But things went south once the deal was sealed. An investigation revealed that Autonomy had been manipulating its finances by offloading hardware below cost and mislabeling the revenue as software licensing.

Plan for integration early

"Gone are the days when you sit around for a couple of months and start thinking about launching an integration-management office," writes Mark Sirower, Principal and M&A Practice Leader at Deloitte Consulting and co-author of The Synergy Solution (HBR Press, 2022). "You have to be prepared to launch right after you announce the deal."

Neglecting to plan for integration is probably the worst thing that any M&A practitioner can do. Integration is where the value is created. Take, for example, the Sprint and Nextel Communications merger.

In 2005, Sprint and Nextel announced a $35 billion all-stock merger to become the third-largest telecommunications company. They wanted to leverage each other's customer bases to then sell additional products to those groups.

Since the company neglected to plan for integration, they were ill-equipped for what would happen post close. The two networks used completely different technologies and did not overlap. The company also suffered from massive market share losses due to conflicting marketing strategies. This allowed competitors to lure away unhappy customers.

Frequently Asked Questions

What is the fundamental aim of mergers and acquisitions?

The fundamental aim of mergers and acquisitions is to enhance the market share of a business, extend the product line of the business, or reduce the costs of the business. Mergers and acquisitions can also happen when a business seeks to become competitive or create value for shareholders.

Is an acquisition a takeover?

A takeover is an acquisition. Acquisitions are always friendly, meaning that both parties must agree to the merger. An acquisition happens when a business buys stocks from shareholders of the business or when it makes a deal with shareholders without the consent of the shareholders. This is a takeover.

What is the biggest concern people have regarding mergers?

When two or more companies are involved in a merger, the companies can reduce costs by restructuring the business processes of the companies involved in the merger. This may cause some people to lose jobs, and that is the biggest concern that the majority of people have regarding mergers.

What happens when two or more companies engage in a merger?

When two or more companies engage in a merger, the companies come together to form one entity with the common goal of improving the presence of the companies in the market. This can be achieved by restructuring the companies to enhance the presence of the companies in the market.

What is the merger paradox?

The merger paradox can be described as a situation of unrealized expectations. It is a fact that a merger is always accompanied by a certain level of expectations. However, it has been noted that a merger does not always come to pass as expected but instead leads to a situation of inefficiency.

What is an example of a successful acquisition?

Disney's 2006 acquisition of Pixar for $7.4B is widely cited as the most successful tech-media acquisition of the past 25 years; Disney retained Pixar's creative leadership and the studio went on to produce franchises that generated more than $11B in box-office revenue.

What is the greatest acquisition of all time?

Measured by inflation-adjusted deal value, Vodafone's 1999 acquisition of Mannesmann ($202.8B at the time, ~$398B in 2026 dollars) remains the largest M&A transaction ever completed.

What is a real life example of an acquisition?

Microsoft's 2023 acquisition of Activision Blizzard for $75.4B is a recent real-life example: announced in January 2022, it required approval from the FTC, EU Commission and CMA, and finally closed October 13, 2023, making it the largest gaming-industry acquisition on record.

Final thoughts

All in all, it's hard to argue which merger or acquisition has been the most successful, because sometimes it takes years for the value and potential of a merger or acquisition to formulate.

However, it's been observed that the best mergers and acquisitions (just like some that have yet to be made in terms of M&A deals) are those that take into consideration best practices in communication, strategic goal/deal thesis, and integration planning.

Technology and tools may also be used in making a deal successful.

The DealRoom M&A Platform has been developed to assist M&A teams in effectively managing complex M&A deals. The DealRoom M&A Platform is a unified platform that has been specifically designed to meet the requirements of M&A teams by providing a streamlined solution to effectively manage all aspects of M&A deals, including M&A pipeline management, the entire due diligence process, and post-merger integration.

Get the latest M&A tips & news delivered straight to your inbox

We’ll email you 1-3 times per week—and never share your information.

1. Higher valuation of companies with mature human-AI collaboration frameworks

2. Increased focus on worker skill complementarity during integration

3.Growing importance of ethical AI governance in acquisition targets

4. New due diligence categories evaluating human-machine interaction quality

Learn how to approach diligence, build a diligence team, the art of asking good questions, why due diligence is an iterative process, and the importance of data integrity. No degree or prior experience required.

Led by:

This is some text inside of a div block.

This is some text inside of a div block.

James Harris

Principal of Corporate Development Integration at Google

50+ courses by M&A Experts

Get access to diligence, integration, divestment and strategy courses. 100% online and at your own pace.

Get Diligence Ready

Learn diligence strategy and critical skills, diligence requests, workflow management and receive certificate of completion

Discover why DealRoom is the best merges and acqusitions software for Corporate Development teams managing multiple deals. Simplify your M&A lifecycle, boost efficiency, and reduce friction — all in one platform.

.avif)

.avif)

.avif)