.avif)

GlobalM&A reached $2.8 trillion in the first half of 2026 alone up 48% year over year and the strongest first half since records began in 1980 after a$4.6 trillion full-year 2025, itself the highest annual total since 2021 with mega-deals like Chevron-Hess ($53B), Nippon-US Steel ($14.9B), and the pending $85B Union Pacific-Norfolk Southern merger setting the tone for 2026.

You can check out the free interactive table and timeline our developers built to help you dig deeper on the most recent deals (which you won't find anywhere else):

Want to stay on top of all the most important Mergers and Acquisitions deals happening across the globe? We have you covered with our updated Mergers and Acquisitions deals list, which gives you access to the latest deals, upcoming deals, and the largest Mergers and Acquisitions deals of recent times.

You can also look into the future with our free upcoming M&A tracker.

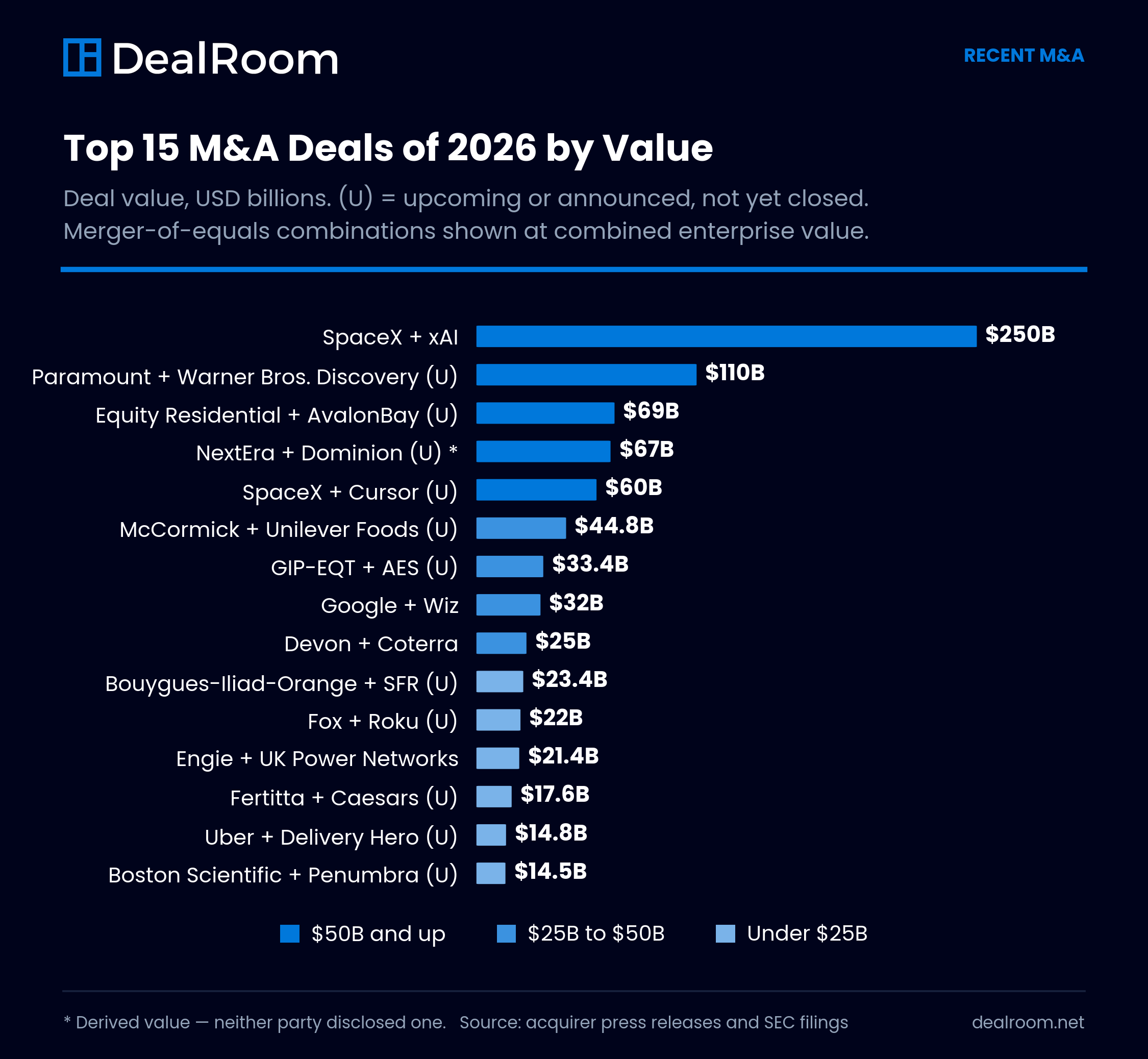

Most Recent M&A Deals: Closed or Closing in 2026

Most Recent M&A Deals (Q1-Q2 2026)

The 12 most-watched deals announced or closed in the first half of 2026, ordered by deal value. Together they represent more than $1.4 trillion in transaction value across energy, healthcare, technology, and financial services.

Largest Closed Deals from 2025

1. T-Mobile acquisition of U.S. Cellular

- Date closed: August 1, 2025

- Value: $4.3 billion

- Industry: Telecommunications

The acquisition of US Cellular by T-Mobile was announced on May 28, 2024, in which the latter acquired the entire customer base and retail presence of the former, including 30% of its spectrum assets. The acquisition was officially closed on August 1, 2025, in which T-Mobile took over $1.7 billion in debt and $2.6 billion in cash, amounting to approximately $4.3 billion after finalizing the acquisition deal with US Cellular. US Cellular’s customer base, which was over 4 million in number, can easily switch to T-Mobile services since they can still retain their existing plans but have the option to switch to T-Mobile’s services if they wish to do so. The acquisition has expanded T-Mobile’s rural presence, especially in 5G connectivity, as it has aligned with its strategy to be the leader in connectivity and value.

2. Mallinckrodt Pharmaceuticals and Endo Pharmaceuticals merger

- Date closed: August 1, 2025

- Value: $6.7 billion

- Industry: Pharmaceutical

The merger between Mallinckrodt Pharmaceuticals and Endo Pharmaceuticals was officially closed on August 1, 2025, in which the latter merged with the former to form a new entity in the therapeutics industry, as it was announced in March 2025. The value of the new entity was approximately $6.7 billion since it was anticipated that it would be able to attain $75 million in pre-tax run-rate operating synergies within the first 12 months after the merger. The savings would be achieved through business function savings, R&D savings, and economies of scale in the operations of the new entity. The entity’s presence in operations would be comprised of 17 manufacturing facilities, 30 distribution facilities, and 5,500 to 5,700 employees in the most significant international markets.

Both companies filed for bankruptcy protection under Chapter 11 due to the opioid litigation cases filed against them. The merger has allowed the new company to consolidate free from the opioid debts of the former companies, which has been a contentious issue in the merger, especially considering the high number of deaths caused by the opioid crisis in the United States.

3. Brookfield Infrastructure Partners acquisition of Colonial Enterprises, Inc.

- Date closed: July 31, 2025

- Value: $9 billion

- Industry: Energy Logistics (Colonial Pipeline)

Brookfield Infrastructure Partners has acquired Colonial Enterprises, Inc., the parent company of Colonial Pipeline, for approximately $9 billion, including outstanding debts. This acquisition has enriched its portfolio of midstream infrastructure in North America, giving it more power to control one of the biggest fuel transportation networks in the United States. Colonial Pipeline has over 5,500 miles of pipeline stretching from Texas to New York, transporting 2.5 million barrels of fuel per day, which translates to almost 45% of fuel consumed on the East Coast of the United States, covering 14 states.

Brookfield acquired full ownership of Colonial Enterprises, which was constructed decades ago, with the transaction closing in the second half of 2025 following regulatory approval in Q4 2025.

4. La Caisse (formerly CDPQ) acquisition of Innergex Renewable Energy

- Date closed: July 21, 2025

- Value: $7 billion

- Industry: Renewable energy

On February 25, 2025, CDPQ, which was later rebranded to La Caisse in June 2025, announced its intention to acquire C$10 billion in an all-cash deal to take Innergex Renewable Energy private. The deal translates to approximately C$13.75 per share of common stock in Innergex Renewable Energy. The offer price represents a 58% premium over Innergex Renewable Energy’s trading price before the announcement.

The acquisition was completed on July 21, 2025, with Innergex Renewable Energy becoming a privately held company after La Caisse completed the acquisition deal. The syndication structure allows Innergex Renewable Energy to be able to attract co-investors with the same vision for the company’s future. The global presence and financial capacity of La Caisse mean that Innergex Renewable Energy can expand globally in industries like energy in Chile, France, and the US.

5. Chevron acquisition of Hess Corporation

- Date closed: July 18, 2025

- Value: $53 billion

- Industry: Energy

Chevron acquired Hess Corporation on July 18, 2025. The acquisition deal was valued at $53 billion. The acquisition deal was announced in October 2023 but was completed on the announced date after Chevron was given the go-ahead to acquire Hess’s 30% stake in the Stabroek Block in Guyana after winning an international arbitration case in Paris.

The Stabroek Block is an oil field located in Guyana in the Caribbean Sea and has over 11 billion barrels of oil equivalent. ExxonMobil operates the block but has only 45%, with CNOOC owning 25%.

ExxonMobil sought to prevent Chevron from acquiring the remaining 30% of the block on the basis of the right of first refusal. However, the arbitration panel rejected the claims. This paved the way for the completion of the transaction with the Hess Corporation. Analysts have predicted that this transaction will increase production for Chevron to reach the range of 4.2-4.31 million barrels of oil per day in the next few years. This will bring the company on par with ExxonMobil. The transaction was also motivated by the need for Chevron to increase its reserves. The company's proven oil reserves have depleted to 9.8 billion boe as of the end of 2024.

With the acquisition of Hess now complete, Chevron joins other major international oil producers in gaining access to one of the fastest-growing upstream regions of the world.

6. Nippon Steel acquisition of U.S. Steel

- Date closed: June 18, 2025

- Value: $14.9 billion

- Industry: Steel

In one of the most contentious deals, Nippon Steel has finalized the acquisition of U.S. Steel for US$14.9 billion (~$55/share) on June 18, 2025. The acquisition was previously blocked by then-US President Biden but was overturned by US President Trump on June 13, 2025, via executive order, conditional on the signing of a new National Security Agreement (NSA) between Nippon Steel and the US government.

In order for Nippon Steel to complete the acquisition, it has had to agree on numerous conditions that will guarantee the operation of U.S. Steel as a US-based company, including but not limited to, investing close to US$11 billion in US operations by the year 2028, including significant modernization and expansion projects, the maintenance of U.S. Steel’s corporate citizenship, headquarters, management, board, and leadership, including the CEO, within the US.

As part of the deal, the US government will have the power of veto over key decisions that include the relocation of the company, deviations from the investment plan, changes of name, closure of any of the company’s plants, or changes in the executive leadership of the company.

As a result of the acquisition, the company will become the second-largest steel producer in the world with an annual capacity of 86 million tonnes, second only to the Chinese steel producer Baowu Group.

7. KKR & Co. and PSP Investments acquisition of a stake in American Electric Power Co.

- Date closed: June 5, 2025

- Value: $2.8 billion

- Industry: Energy

In January 2025, investment firms KKR & Co. and PSP Investments agreed on the acquisition of a 19.9% minority stake in American Electric Power's transmission businesses operating in the states of Ohio, Indiana, and Michigan for $2.82 billion. This strategic alliance will enable American Electric Power Company to provide reliable service while meeting the increasing demand for electricity in the regions.

The acquisition deal officially closed on June 5, 2025. The deal enables American Electric Power to meet regional electricity demand and to fund its $54 billion 2025-2029 capital plan covering transmission, distribution, and generation projects, while also offsetting $5.35 billion of its equity financing costs.

8. Sanofi acquisition of Dren Bio’s DR-0201

- Date closed: May 27, 2025

- Value: $1.9 billion

- Industry: Pharmaceutical

Sanofi plans to acquire Dren Bio’s DR-0201, a bispecific myeloid cell engager, for an upfront payment of $600 million and up to $1.3 billion in milestone payments, for a total deal value of up to $1.9 billion, in March 2025. This acquisition will add a promising first-in-class bispecific myeloid engager to Sanofi’s portfolio, which will be led by Sanofi’s vision of being a leader in immune reset.

The risk involved by Sanofi is minimal, given that it has made an upfront payment and agreed to pay milestone payments. However, the chances of approvals and launches are still far off, and it is a long-term prospect. Dren Bio will remain an independent company and continue to develop its portfolio of targeted myeloid engager therapies.

9. Payoneer acquisition of Easylink Payment Co., Ltd.

- Date closed: April 9, 2025

- Value: Not disclosed

- Industry: Financial services

Payoneer, a global fintech company, has announced that it has acquired Easylink Payment Co., Ltd., a licensed payment services provider in China. The acquisition was completed in April 2025. Payoneer has become the third foreign payment platform to secure approval to offer online payment services in China.

According to the Payoneer CEO, John Caplan, the acquisition has helped Payoneer strengthen its position in the global arena in the regulatory space, enabling it to offer better products to Chinese companies that seek to expand internationally.

10. Kandu Health and Neurolutions merger

- Date closed: April 8, 2025

- Value: $30 million (in new funding)

- Industry: Healthcare

The merger between Kandu Health and Neurolutions has resulted in the formation of Kandu, Inc., which has the mission of revolutionizing stroke care. The new organization seeks to offer a better solution to stroke survivors through the combination of Neurolutions’ brain-computer interface technology and Kandu Health’s personalized telehealth services.

The merger has been designed to address the gaps in stroke care that exist in the current state of the art, which is limited to the short-term solution available in the market. The new organization has $30 million in new funding, courtesy of Ally Bridge Group and AMED Ventures, and is seeking to move the solution forward in the market.

11. Transcarent and Accolade merger

- Date closed: April 8, 2025

- Value: $621 million

- Industry: Healthcare

The digital health platform Transcarent has acquired Accolade in a deal that was closed on April 8, 2025, for $621 million.

Currently, with over 20 million members and 1,700+ employer and health plan clients, the company is dedicated to providing a more complete and personalized healthcare experience.

12. Forcepoint acquisition of Getvisibility

- Date closed: April 7, 2025

- Value: Not disclosed

- Industry: Tech

Forcepoint, a global data security company, has completed its acquisition of Getvisibility, a company based in Ireland that offers AI-Powered Data Security Posture Management and Data Detection and Response solutions.

This acquisition is likely to improve Forcepoint’s Data Security Everywhere solution by integrating Getvisibility’s unique AI technology, providing better real-time data security threats in hybrid cloud and generative AI environments.

13. Stifel Financial acquisition of B. Riley Employee Advisors

- Date closed: April 7, 2025

- Value: Not disclosed

- Industry: Financial services

Stifel Financial Corp has completed its acquisition of B. Riley Financial’s Employee Brokerage Unit on April 7, 2025. This acquisition brings $4 billion in client assets and 36 financial advisors to Stifel Financial’s Global Wealth Management division.

This acquisition is worth $27 million to $35 million and is an asset purchase deal, and the value depends on how many advisors are joining Stifel Financial. This acquisition is a part of the company’s strategy to expand its presence in the market by acquiring wealth management companies.

Stifel Financial has been focusing on acquiring wealth management companies to expand its presence in the market.

14. NeoGenomics acquisition of Pathline

- Date closed: April 7, 2025

- Value: Not disclosed

- Industry: Healthcare

NeoGenomics, a leading company in the field of cancer diagnostics, has officially acquired Pathline, LLC on April 7, 2025. Pathline, LLC is a CLIA/CAP/NYS-certified laboratory located in New Jersey. The acquisition will enable NeoGenomics to expand its service offerings in the Northeast region, making its comprehensive range of cancer tests and lab services more accessible to more patients and physicians in the Tri-State region.

Pathline, LLC was founded in 2009 and has been providing lab services to hospitals, cancer centers, and physician practices, mostly in the Northeast region. With this acquisition, NeoGenomics will be able to accelerate its growth in its molecular and hematology oncology tests.

15. Aptean acquisition of Logility

- Date closed: April 5, 2025

- Value: $442.75 million

- Industry: Tech

Aptean, a global industry-specific software company, has officially announced its acquisition of Logility Supply Chain Solutions, Inc., a company specializing in AI-first supply chain management software. This acquisition has been completed on April 3, 2025, after receiving approval from shareholders of Logility.

The acquisition of Logility has strengthened Aptean’s position in the industry, adding AI-powered supply chain planning software to its offerings. This software enables businesses to build a more sustainable and digital supply chain. Aptean has acquired all outstanding shares of Logility’s common stock for $14.30 in cash per share. The stock has ceased trading on Nasdaq or any other stock exchange.

16. Novartis acquisition of Anthos Therapeutics

- Date closed: April 3, 2025

- Value: $3.1 billion

- Industry: Pharmaceutical

Pharmaceutical company Novartis has completed its acquisition of clinical-stage biopharma company Anthos Therapeutics, specializing in cardiometabolic diseases, on April 3, 2025, for up to $3.1 billion. The deal includes an upfront payment of $925 million, and the remaining will depend on milestones achieved in the future.

Novartis has been making efforts to strengthen its cardiovascular portfolio and keep its focus on its areas of interest.

17. Nano Dimension acquisition of Desktop Metal

- Date closed: April 2, 2025

- Value: $179.3 million

- Industry: Manufacturing

Nano Dimension, the digital manufacturing leader, has officially acquired Desktop Metal, the manufacturer of industrial 3D printing systems. The company has completed its previously announced acquisition of Desktop Metal in an all-cash transaction for approximately $179.3 million, or $5.295 per share, in a deal first announced in July 2024.

The acquisition of Desktop Metal will strengthen the company’s position in the industry by providing a complete portfolio of advanced manufacturing solutions for various industries, including aerospace and defense, automotive, consumer electronics, industrial automation, and medical technology.

18. Hope Bancorp and Territorial Bancorp merger

- Date closed: April 2, 2025

- Value: $78.6 million

- Industry: Financial services

Hope Bancorp, the parent company of Bank of Hope, has completed its merger with Territorial Bancorp Inc., the holding company of Territorial Savings Bank in Honolulu, Hawaii.

As of April 2, 2025, Territorial Savings Bank will continue to serve the community under the same name, Territorial Savings, a division of Bank of Hope, keeping its 100+-year legacy alive. With this merger, Bank of Hope became the largest regional bank dedicated to serving multicultural communities in the continental United States and Hawaii.

19. Ballymore Safety Products acquisition of Valley Craft Industries

- Date closed: April 1, 2025

- Value: Not disclosed

- Industry: Manufacturing

Ballymore Safety Products, a company sponsored by One Equity Partners, has acquired Valley Craft Industries, a Minnesota-based manufacturer of material handling equipment, drum handling equipment, and storage solutions.

The acquisition is the fourth for Ballymore Safety Products since 2021 and marks a new Midwest headquarters for the company. Further, the acquisition provides a substantial increase in Ballymore Safety Products’ U.S. manufacturing capacity and product offerings—a move that further solidifies its leadership in delivering safety, vertical access, and material handling solutions in the U.S.

20. Lantheus acquisition of Evergreen Theragnostics

- Date closed: April 1, 2025

- Value: $1.0025 billion

- Industry: Pharmaceutical

Lantheus Holdings, a pharmaceutical company focused on pharmaceutical products in the form of radiopharmaceuticals, completed its acquisition of Evergreen Theragnostics.

The acquisition was announced in January and consists of a $250 million upfront payment and a possible milestone payment of up to $752.5 million.

The acquisition strengthens Lantheus's leadership in the entire spectrum of radiopharmaceuticals.

21. Renasant Corporation and The First Bancshares, Inc. merger

- Date closed: April 1, 2025

- Value: $1.2 billion

- Industry: Financial services

Renasant Corporation, a bank holding company headquartered in Tupelo, Mississippi, completed its merger with Hattiesburg-based The First Bancshares, Inc.

The merger is an all-stock deal that was first announced in July 2024 and is valued at around $1.2 billion.

The merger of the two banking institutions means that the new entity will have over 250 banking, lending, mortgage, and wealth management locations in the Southeastern United States, including Mississippi, Alabama, Florida, Georgia, Louisiana, North Carolina, and South Carolina. This merger has therefore positioned Renasant as one of the leading banking institutions in the Southeastern United States.

22. Seagate acquisition of Intevac

- Date closed: March 31, 2025

- Value: $95.87 million

- Industry: Tech

Seagate Technology has announced the completion of the acquisition of Intevac, Inc., which specializes in the production of thin film processing systems. The acquisition started when the company initiated the cash tender offer for all outstanding shares of Intevac common stock at $4.00 per share. The tender offer was completed on March 28, 2025. In the tender offer, almost 88% of the outstanding shares of Intevac common stock were acquired by Seagate Technology.

The acquisition was completed on March 31, 2025, when the merger of the two companies took place. In the merger, Intevac became a wholly owned subsidiary of Seagate Technology. In the acquisition, the shares of Intevac have been suspended from trading on the Nasdaq Global Select Market.

23. AMD acquisition of ZT Systems

- Date closed: March 31, 2025

- Value: $4.9 billion

- Industry: Tech

Advanced Micro Devices (AMD) completed the acquisition of ZT Systems for $4.9 billion on March 31, 2025. The acquisition was completed by paying cash and stock to the shareholders of the target company. ZT Systems is known for the production of AI infrastructure as well as general-purpose compute infrastructure for hyperscale computing companies.

The acquisition of ZT Systems by AMD has been completed to enhance the data center segment of the company. In the acquisition, AMD has the aim of leveraging the skills of ZT Systems in the production of large-scale computing systems.

24. xAI acquisition of X (formerly Twitter)

- Date closed: March 28, 2025

- Value: $33 billion

- Industry: Tech

xAI, an AI company owned by tech mogul Elon Musk, has acquired social media company X, formerly Twitter, in an all-stock deal that has valued xAI at $80 billion and X at $33 billion, including $12 billion of debt.

This deal is a merger that will see the superior AI technology of xAI and the user base of X come together to better serve users and move the world forward in knowledge and innovation. The acquisition of Twitter by Musk for $44 billion in 2022 and renaming Twitter to X marked the beginning of a journey that has seen these two companies get to this merger deal. This deal will be beneficial to both companies since they will be able to better their products and advance AI technology.

25. Rafael Holdings, Inc. and Cyclo Therapeutics, Inc. merger

- Date closed: March 26, 2025

- Value: Not disclosed

- Industry: Pharmaceutical

Rafael Holdings has merged with Cyclo Therapeutics after obtaining approval from shareholders of both companies.

As part of the deal, Rafael Holdings has agreed to distribute its shares of Class B common stock to shareholders of Cyclo Therapeutics, giving them 22% of outstanding shares of the merged entity on a pro forma basis, calculated on an exchange ratio of 0.3525.

Rafael Holdings’ President & CEO Bill Conkling said the merger marks an important milestone in the development of clinical-stage products that target serious unmet medical needs.

26. World Wide Technology acquisition of Softchoice Corp.

- Date closed: March 17, 2025

- Value: $1.3 billion (C$1,478,242,241)

- Industry: Tech

Technology integration company World Wide Technology (WWT) announced that it had completed its acquisition of Softchoice Corporation, a Canadian-based information technology solutions company specializing in software and cloud solutions. The acquisition was completed on March 4, 2025.

The acquisition is a great move for WWT as it enhances its software, cloud computing, cybersecurity, and artificial intelligence capabilities in North America. Additionally, Softchoice’s extensive footprint in Canada and focus on delivering solutions to small and midsized businesses make it a great fit for WWT.

27. Diversified Energy acquisition of Maverick

- Date closed: March 14, 2025

- Value: $1.275 billion

- Industry: Energy

Diversified Energy Company PLC completed its acquisition of Maverick Natural Resources, a portfolio company of EIG Global Energy Partners.

The acquisition is a great milestone for Diversified as it expands its Permian Basin presence, particularly in the Northern Delaware Basin. Additionally, the acquisition enhances its presence in the Western Anadarko Basin. The acquisition is a great move for Diversified as it targets acquiring mature fields with low decline rates and generating consistent cash flows.

28. Rio Tinto acquisition of Arcadium Lithium

- Date closed: March 6, 2025

- Value: $6.7 billion

- Industry: Energy

On March 6, 2025, Rio Tinto completed its acquisition of Arcadium Lithium plc for a consideration of $6.7 billion in an all-cash deal.

With the acquisition of Arcadium Lithium, Rio Tinto is strengthening its position as a world leader in lithium production and driving the energy transition forward.

With the acquisition of Arcadium Lithium, Rio Tinto is in a position to significantly boost its lithium production capacity in the future. It plans to produce over 200,000 tonnes per year of lithium carbonate equivalent by 2028. With the acquisition of Arcadium Lithium, Rio Tinto is in an excellent position to meet the growing demand for lithium products as a result of the rising demand for electric vehicles and renewable energy storage.

29. TKO Group Holdings acquisition of IMG, On Location Experiences, and Professional Bull Riders (PBR)

- Date closed: February 28, 2025

- Value: $3.25 billion

- Industry: Sports and event management

TKO Group Holdings (TKO) announced that it has closed the $3.25 billion all-equity acquisition of IMG, On Location Experiences, and Professional Bull Riders (PBR) from Endeavor Group Holdings.

With the acquisition of IMG, On Location Experiences, and Professional Bull Riders by TKO Group Holdings, TKO Group Holdings has acquired some of the biggest brands in the sports and entertainment industry under its umbrella, which already comprises the UFC and WWE. With the acquisition of IMG, Endeavor has a 59% stake in TKO Group Holdings.

30. IBM acquisition of HashiCorp

- Date closed: February 27, 2025

- Value: Not disclosed

- Industry: Tech

IBM has announced that it has officially closed the $6.4 billion acquisition of HashiCorp, a leading company that provides the industry’s most advanced products for the development of multi-cloud infrastructure.

With the acquisition of HashiCorp, IBM has acquired all outstanding shares of HashiCorp at $35 per share in an all-cash transaction. The acquisition is a significant milestone in the journey to become the leader in hybrid cloud and AI.

As part of this acquisition, IBM intends to combine HashiCorp's technology with its existing products like Red Hat OpenShift and Ansible Automation.

31. Stryker acquisition of Inari Medical

- Date closed: February 19, 2025

- Value: $4.9 billion

- Industry: Medical devices

Stryker Corporation completed its acquisition of Inari Medical Inc. on February 19, 2025, for a consideration of $4.9 billion in an all-cash deal. All outstanding shares of Inari Medical have been acquired by Stryker for a price of $80 per share. Inari is known for its pioneering medical device products for treating venous thromboembolism without using thrombolytics.

Inari's medical device products include FlowTriever for treating pulmonary embolism and ClotTriever for peripheral thrombectomy. Both products are a great fit for Stryker's Neurovascular business and for expanding their footprint in interventional endovascular procedures. Kevin Lobo, Stryker's Chair and CEO, says that this acquisition is a step in the right direction for Stryker in their quest to establish themselves in this field.

The stocks issued by Inari have been delisted from the Nasdaq Global Select Market.

32. Quikrete acquisition of Summit Materials

- Date closed: February 10, 2025

- Value: $11.5 billion

- Industry: Construction/building materials

Quikrete Holdings Inc. completed its acquisition of Summit Materials Inc. for a consideration of $11.5 billion in an all-cash deal that included debt repayment on February 10, 2025.

This is a strategic move to create a vertically integrated powerhouse in the construction materials sector and drive growth in products and operational efficiencies in North America. In addition, as a result of this acquisition, Summit has been delisted from the NYSE and is currently a privately held subsidiary of Quikrete.

33. Swisscom acquisition of Vodafone Italia

- Date closed: December 31, 2024

- Value: $8.6 billion

- Industry: Telecommunications

Swisscom has acquired Vodafone Italia for an all-cash consideration of €8 billion on 31st December 2024. The strategic objective is to merge Vodafone Italia with its Italian subsidiary, Fastweb, to create a telecom giant.

Walter Renna, CEO of the new company, said that it is a game-changer for the Italian telecom market and is geared to propel Italy’s digital future. This acquisition is geared to create value for Swisscom shareholders in the form of cash flow and dividends.

This new company is geared to become a telecom giant by combining Fastweb’s fixed network leadership with Vodafone Italia’s leadership in mobile services and is geared to offer innovative and competitive offers to households, enterprises, and public institutions.

Key M&A Trends Shaping 2026

The M&A activity in 2026 is affected by a number of factors, including macro and micro factors, in addition to changes in the regulatory environment. The key M&A trends that are defining 2026 are:

AI and Automation: The Biggest Driver of Tech M&A

The most dominant driver of mergers and acquisitions in the technology sector is artificial intelligence. CB Insights counted 266 AI M&A deals in Q12026, up 90% year over year and found big tech buyers are acquiring AIcompanies an average of 4.5 years after founding, against 7.6 years across allAI M&A.

The acquisitions in the technology sector are mostly in data infrastructure, LLM Ops, and AI security with the aim of incorporating intelligent automation technology.

Cross-Border Deals Making a Resurgence

The supply chain was disrupted for firms in the aftermath of the global economic crisis. However, with the improvement in the economic environment, cross-border M&A deals are making a resurgence.

The clean energy sector, semiconductor manufacturing sector, and logistics sector in 2026 are seeing the highest number of cross-border M&A deals building on the surge that began in 2025.

In addition to that, acquisitions are taking place with the aim of diversifying supply chains.

Private Equity Is Making a Resurgence with a Twist

The private equity firms took a cautious approach in the recent past in terms of M&A activity. However, since 2025, private equity firms have been making a comeback in M&A activity with a twist a trend that has accelerated into 2026.. The acquisitions are not taking place at the same scale as in the past.

The size of these acquisitions is small. The idea behind these acquisitions is to add value to the existing portfolio firms. Additionally, the increase in carve-outs and divestitures that began in 2025 has continued into 2026.

Family-owned firms are also seeing an increase in acquisitions. These acquisitions are seen in the healthcare sector, manufacturing sector, and industrial services sector.

M&A in the Climate Tech and Sustainability Sector

The sector of sustainability continues to remain a key strategic priority. M&A in this sector is seen to boost ESG strategies. M&A in climate technology, which includes EV charging stations, carbon capture technology, and water conservation technology, is seen to gain momentum.

These acquisitions are helping companies meet regulatory and investor demands. Additionally, these acquisitions are creating opportunities for new business models in clean energy and sustainable business.

Healthcare Consolidation

The healthcare sector continues to remain a key sector for M&A in 2026. Vertical integration in the sector is seen to gain Healthcare M&A: Pharma's Patent-Cliff Era Drives 2025-2026 Consolidation

Healthcare M&A in 2025-2026 is dominated by big pharma acquiring clinical-stage biotechs to refill pipelines. Between 2025 and 2030, over $300 billion in prescription drug revenues will lose exclusivity, according to Evaluate. The deals fall into three buckets.

Biotech bolt-ons by big pharma ($1B-$10B)

- Eli Lilly / Centessa Pharmaceuticals — $7.8B (Mar 2026). Sleep-disorder therapies pipeline.

- Eli Lilly / Kelonia Therapeutics — $7B (Apr 2026). Cancer cell-therapy platform.

- Gilead Sciences / Tubulis — $3.15B upfront + $1.85B milestones (Apr 2026). Antibody-drug conjugate (ADC) oncology.

- Sanofi / Dren Bio (DR-0201) — $0.6B + milestones (Mar 2025, closed). Single-asset deal for a B-cell engager in autoimmune.

- UCB / Neurona Therapeutics — up to $1.15B (Apr 2026). Cell therapy for neurological disorders.

- Novartis / Anthos Therapeutics — $3.1B (Feb 2025, closed). Anti-thrombotic Factor XI inhibitor — Novartis re-acquired the asset it spun out.

Mid-cap pharma combinations ($10B-$15B)

- Sun Pharma / Organon — $11.75B (Apr 2026). Largest biotech deal of 2026 to date. Sun Pharma gains established Organon women's health and biosimilars portfolio.

- Mallinckrodt / Endo Pharmaceuticals — $6.7B (Aug 2025, closed). Two restructured specialty-pharma names combined to scale post-bankruptcy.

- Angelini Pharma / Catalyst Pharmaceuticals — $4.1B (Apr/May 2026). Italian privately-held Angelini's first major US footprint, focused on rare disease.

Med-tech and devices ($1B-$15B)

- Boston Scientific / Penumbra — $14.5B (announced 2025, expected close 2026). Stroke and peripheral interventional platform.

- Stryker / Inari Medical — $4.9B (Feb 2025, closed). Venous thromboembolism (VTE) market entry.

- Johnson & Johnson / Shockwave Medical — $17B (May 2024, closed). J&J's largest med-tech deal — calcium-modification for coronary artery disease.

The constant across all three buckets: buyers aretypically paying 25–50% over the prior close, with outliers approaching 80%, signaling that strategic buyers see the patent cliff as forcing them to act fast rather than wait for assets to mature.

Strategic Portfolio Rebalancing

Large firms are seen to have been rethinking their business portfolios. Companies are seen to have been shedding businesses that are not core to their business.

Additionally, companies are seen to have been acquiring businesses that are strategically important for their digital transformation strategies. These have created spin-offs, carve-outs, and acquisitions in businesses that are in a state of flux.

The companies are looking to invest in those businesses that have good growth prospects in the areas of digital services, cloud infrastructure, and customer experience technology to boost relative competitiveness.

Regulatory Headwinds

Antitrust and regulatory pressure has been one of the major factors that has been affecting M&A in 2025.

In the US and Europe, M&A deals that have the potential to reduce competition in the industry have come under significant pressure from the government and have been called 'killer acquisitions.'

Therefore, M&A deals have been structured in a manner to avoid such pressure by either doing a minority deal or a strategic alliance that has less probability of attracting the ire of the government.

Focus on Operational Synergies

Since 2025, the focus of M&A has shifted to operational efficiency and real-time value creation.

The buyers are looking to focus more on the importance of integration planning, cost savings, and EBITDA improvements.

In the place of strategic M&A, the buyers are looking to create value on a real-time basis in the business, which is changing the parameters of the success of M&A deals.

Frequently Asked Questions

Why do companies do mergers and acquisitions?

Companies do mergers and acquisitions for strategic growth, market share, capabilities, markets, competition elimination, or cost savings through strategic synergy.

How are M&A deals financed?

M&A deals can be financed in the form of cash, stocks, debts, or a combination of all these factors, depending on the financial position of the companies involved in the deal as well as the reasons behind the M&A deals.

How long does an M&A deal take to close?

From 2005 through 2024 the median time between signing and closing was about 6.4 months, a 25% increase over twenty years, with roughly 16% of deals now taking more than a year, according to McKinsey.

What challenges do M&A deals face?

M&A deals face cultural, regulatory, valuation, operational, as well as synergies challenges.

What was the Disney-Pixar M&A deal? Was it a merger or a takeover?

The M&A deal between Disney and Pixar was a takeover. The Walt Disney Company acquired Pixar Animation Studios in 2006 in an all-stock transaction valued at $7.4 billion, which was called a “merger” because of the long-standing relationship between the companies.

Why did Exxon and Mobil merge?

Exxon and Mobil merged in 1999 to form ExxonMobil to reduce costs as well as attain competitiveness in the world market, where the price of oil was low.

What was an example of a vertical merger?

The example of the M&A deals in the form of a vertical merger is the PepsiCo and PepsiAmericas M&A deal of 2005, where PepsiAmericas was a bottling company, thus enabling PepsiCo to have better control over the business.

Key Takeaways

Deal-making in 2026: M&A activity continues to be driven by AI, healthcare, and energy — the three biggest sub-sectors by deal value in both 2025 and 2026 to date. Bookmark this page to stay updated on the latest M&A deals throughout 2026, plus our M&A resources library for related guides and templates.