.avif)

In the typical business plan, the SWOT analysis is little more than an afterthought, hidden away at the back of the document.

It is often filled in with truisms: the company’s strengths include an experienced management team and a strong brand, its weaknesses include a short-term lack of access to capital, the biggest threat is a recession and its opportunities include new products and markets.

This generic, poorly executed SWOT analysis is what passes for a corporate development strategy at most small to midsize companies.

And it partly explains why they’ll only ever be small and midsized companies.

Putting together a winning corporate development strategy is crucial for the long-term growth of your business.

And that goes for whether you’re a mid-sized company just past $10 million in annual revenue or a startup that’s yet to break even.

We at DealRoom help many corporate development teams organize their M&A process and in this article we'll dive into corporate development strategy and to start creating it.

You can also checkout the M&A benchmarking tool that we built, based on responses from over 150 deal teams:

So, what is a Corporate Development Strategy?

A corporate development strategy is an actionable plan with the goal of growing / restructuring a business or establishing partnerships. The strategy typically looks to create opportunities through M&A or divestitures. To create a corporate development strategy, teams look inward at a company’s products or services, along with competitor’s offerings and trends.

Pinning Down Corporate Development

Corporate development is the practice of defining the nexus of opportunities that exist for your company, evaluating them and ultimately, capitalizing on them.

M&A transactions are the major component, but it’s more holistic than that. It can also include identifying new partners and suppliers, where to outsource, how to optimize productivity, which lines of product or service should be introduced (or removed) and more.

The end game in many of these options is M&A: what begins as a decision to move into a new line of products or services regularly lead to the decision to acquire a firm in that space.

The decision to enter a new market may begin with a partner search before developing into an acquisition. And optimizing productivity is sometimes just a synonym for adopting new technologies...or acquiring a company with expertise in it.

There’s an ever-expanding list of examples where this kind of corporate development is visible:

- When Starbucks wanted to expand from coffee into tea, instead of starting from scratch, it acquired the upstart tea brand, Tazo, for $8m (in 2017, it sold out to Unilever for $384 million)

- Luxottica partnered up with Sunglass Hut to distribute its range of eyewear before deciding it wanted to buy it for $462 million in 2001;

- One more good example of acquiring technology is provided by eBay’s acquisition of Paypal back in 2002 for $1.5 billion.

This is corporate development in its essence.

In business, there are no guarantees of success, but having a good corporate development strategy at least maximizes the chances of achieving it.

Too often, what firms believe to be a corporate development strategy is nothing more than a series of ideas, not too different from that SWOT analysis mentioned at the outset of this article. A winning strategy demands a lot more than than a 4-square matrix…

%20(2).png)

You’re going to need a waterfall chart.

It begins with a waterfall chart

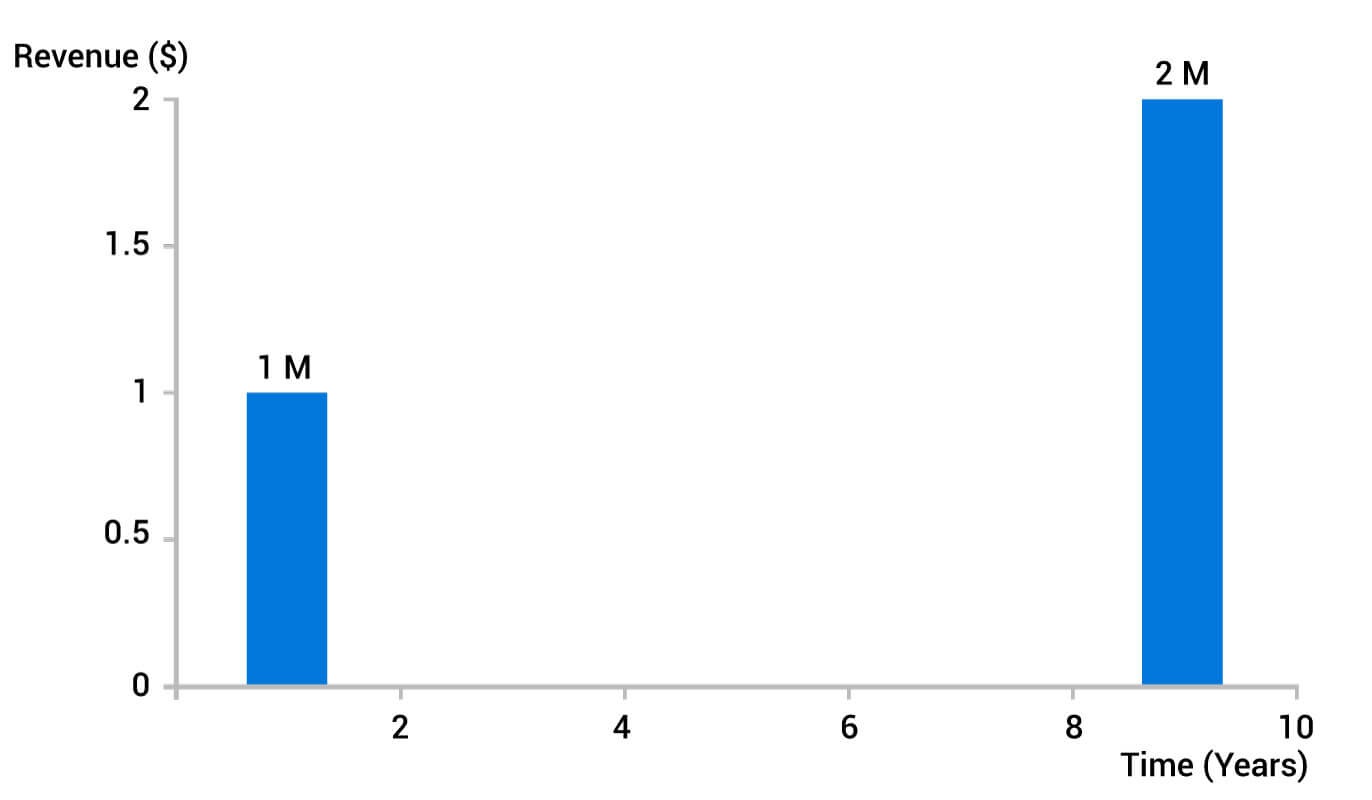

Picture where you want your business to be in ten years’ time in terms of a simple number: its' revenue.

If like most owners of an SME, you’re more used to thinking on a 2- to 5-year time horizon, this will be a useful exercise.

You don’t have to get too specific - round numbers are fine, as long as they’re realistic. And realistic doesn’t mean conservative - this exercise may even work better for now if you overreach a little.

Now, write your company’s revenue for this year on the left-hand side of a page and at the far right-hand side, write the figure you came up with for its revenue 10 years from now.

Now, as if building a bar chart, draw a vertical bar for each, the size of which should roughly correspond to the revenue in each year (i.e. $1 million of sales should be a third of the height of $3 million of sales).

Now you should have two bars at either end of the page, representing your sales this year and your sales in ten years’ time.

How you get from one to the other will be decided by the effectiveness of your corporate development strategy. The vertical distance between the two represents the disparity in revenue between both years.

.jpeg)

Assuming that distance, as per the example, is $2 million, you’ve got to answer the question - “what’s going to generate these sales?”

A waterfall chart, showing where you predict each dollar of revenue will come from over the period will help you to answer.

This isn’t so much an exercise in forcing you to be realistic as encouraging you to think about how you can generate ambitious growth. It’s about turning the

- ‘if I acquire this business, how much growth can I expect?’

into

- ‘I want to quadruple my revenue in ten years, so which company should I acquire to achieve that?’

In other words, revenue is the destination. The parts between the two endpoints are the means to getting there.

So, supposing, for the sake of round numbers, that your growth over 10 years was 200%, representing revenue growth of over 11.5% per year. However, it’s unlikely that all of the growth will be organic.

Even if your company is young and experiencing double-digit growth, that can only hold true for so long. So, let’s suppose that 30% of the total growth over the next 10 years is organic. Draw a bar on your page representing that growth right next to the bar on the left representing this year’s figures.

Still, a long way to go to reach the 10-year figure, right?

This is what makes this a useful first exercise in constructing a corporate development strategy. What steps will enable you to bridge the gap between the two figures?

Suppose you fill in another one - new markets. People frequently believe that they can grow revenues in new markets even faster than their home markets but this is seldom the case. It usually takes more time and money than the home market. Here, we could say 10% of the growth will be down to new markets.

That still leaves 60% of the growth you projected unaccounted for. Price increases over a ten-year period should allow you to account for a further 5%, and new product development (NPD) may bring in, say, 15%. That leaves 40%.

A good way to bridge this gap is M&A, but here’s a reality check: 40% of 200% growth on current revenue would mean that the company (or companies) that you acquire have 80% of your current revenue. So, you’re basically buying a direct competitor in terms of size - all quite possible, but certainly more challenging.

Conclusion

The genesis of a winning corporate development strategy is you deciding where you want your business to be in a decade from now.

By undertaking the brief exercise we have outlined above, you give yourself the best chance of deriving a strategy that achieves your objectives.

As we shall see, you don’t have to rigidly stick to the plan - there will be opportunities along the way, and inevitably, some drawbacks.

But understanding what you want is key to you getting it. In the next article, we will discuss how to put together a corporate development strategy in more detail.

.avif)

.avif)