Understanding Public vs. Private M&A Deals

Despite an array of differences, the ultimate goals of public and private M&A are largely the same: to generate value for the acquirer.

Value should be what underpins every transaction, but as we uncover in the sections below, extracting value from public and private M&A is achieved quite differently.

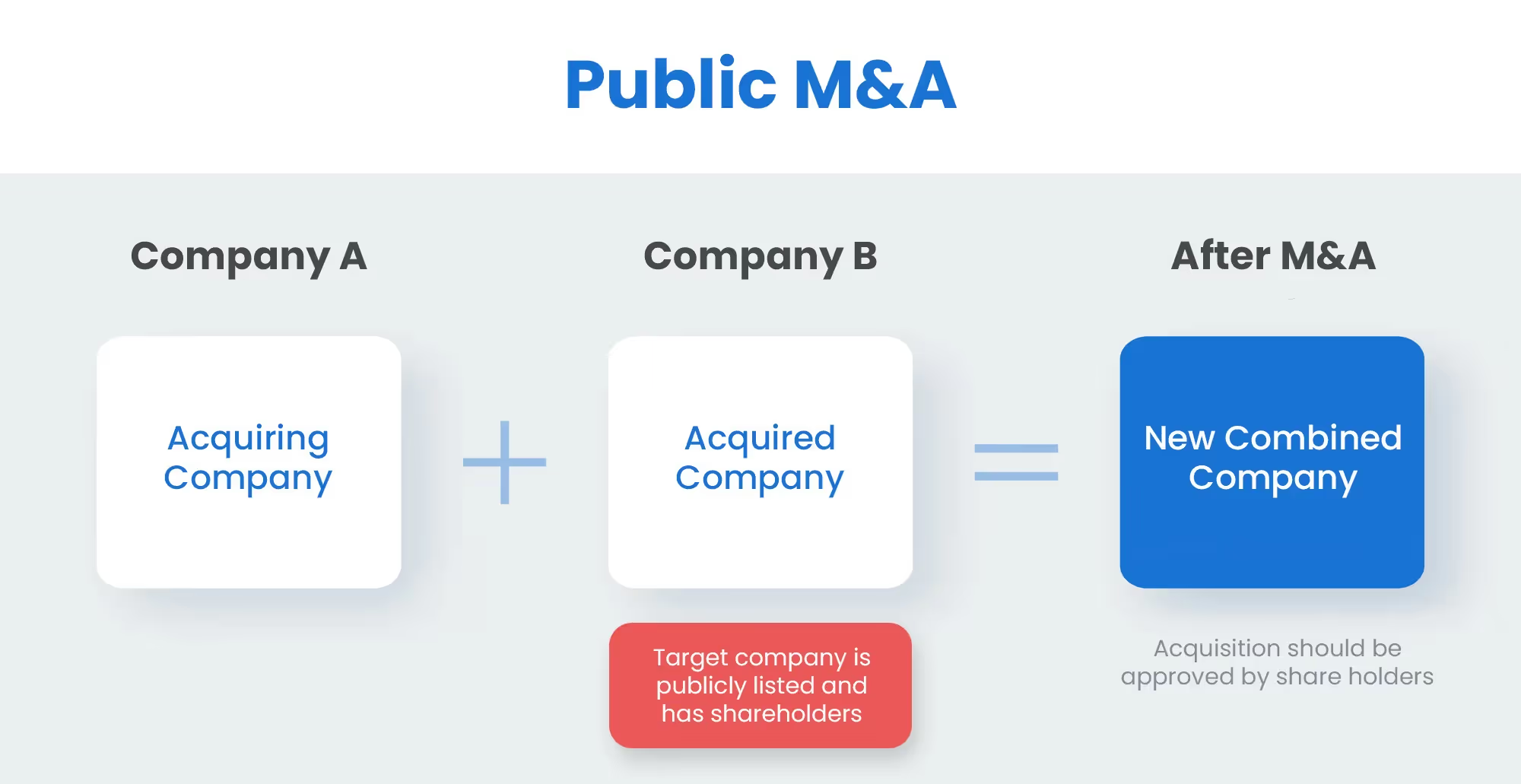

In public M&A, the buyer is acquiring a company whose stock is already being sold on an equity index.

Private M&A, by contrast, involves companies that are not publicly traded, and have very few disclosure requirements.

This gives us a staring point for two quite distinct forms of M&A transactions.

We at DealRoom help dozens of companies execute private and public M&A and have some insights to share with you. So let's start.

What does Public M&A mean?

Public M&A refers to transactions where the target company is publicly listed (i.e. its stock is publicly traded on a stock market index).

What does Private M&A mean?

Private M&A refers to transactions where the target company is private (i.e. its stock is not publicly traded on any stock market index).

Public vs. Private M&A: Key Differences

There are several key differences that tend to exist between public and private M&A transactions.

These include the following:

- Ownership: The ownership of public companies tends to be distributed across several thousand (and sometimes million) shareholders. By contrast, private companies tend to be held by a much smaller group of owners (e.g. a family, partnership or private equity fund).

- Management: Management teams at public companies tend to be more experienced ,with more corporate experience. For example, more than half of CEOs have some finance or accounting experience. In the case of private companies, not only will the management teams be smaller, it could also be that they’ve been promoted to their position because of family connections.

- Information: The level of disclosure that most public companies are obliged to meet - ranging from quarterly audited financial statements to disclosures on all material matters, means that information is much easier to obtain. Private companies, as the name suggests, are far less forthcoming with this information.

- Financials: Closely aligned to the above is the transparency in financial statements that a buyer of a public company can expect. With private companies, by contrast, the relative lack of oversight (with the exception of tax authorities) means different ‘conventions’ are common (cash accounting, to take just one example).

- Valuation: Public companies come with a ready-made valuation - the publicly quoted price for the company. While it’s rarely kept to public M&A, in theory it does provide a very good starting point for a valuation. Private companies have no such ready-made valuations. There are also other issues, such as their lack of liquidity, to account for.

Public M&A Characteristics

Public M&A transactions tend to be characterized by the following:

- Information disclosure.

- Less founder presence.

- Longer time required to gain consensus, with shareholder approval required for material decisions such as M&A.

- Deal structures tend to be more straightforward with public M&A, with combinations of debt and equity used to reach the target company valuation.

- The seller faces far less responsibility for issues that arise after closing - public M&A tends to be viewed from the standpoint of 'buyer beware’.

Private M&A Characteristics

Public M&A transactions tend to be characterized by the following:

- Lack of information disclosure.

- More founder presence.

- Less time required to gain consensus, with only approval from senior management required for the transaction to close.

- Deal structures can become quite convoluted with private M&A and regularly include some form of earn-out structure. Asset purchases are also common.

- The seller can be held financially responsible by the buyer for material omissions during before the transaction closes (for example, a pending lawsuit that wasn’t mentioned).

Public vs. Private M&A: Strategy & Goals

From a transaction standpoint, the goal behind each of these transaction types is the same: to acquire the company while generating as much value as possible.

This means as low a valuation as possible, thorough due diligence, and well planned post-merger integration.

Naturally, there are some differences for each in both cases.

- Valuation: One of the key success drivers of any transaction is the price paid for the target company. In the case of public M&A, shareholders will have to vote on the deal. Companies should avoid being dragged into a bidding war. If the target company voters aren’t interested in selling, it’s usually good to take this as a sign to leave the deal.

- Due Diligence: Although due diligence is important in both public and private M&A, it’s undoubtedly more of a challenge in the latter. Private companies avoid the SEC’s spotlight and may have any number of quirks in their financials, operations, and legal documents. Good practice is to be prepared for these curveballs.

- Post-merger integration (PMI): PMI is equally important in public and private M&A, with one caveat: culture tends to be far better defined in public companies, and anybody undertaking PMI should know this in advance. Private companies may be more easily molded by the acquirer’s culture but it tends to be more of a challenge in public M&A.

When a Private Company Acquires a Public Company

There is a final quirk here. Sometimes a private company will acquire a public company, not just to add value, but to go public itself.

This is known as a reverse takeover, a reverse merger, or a reverse IPO (an IPO in the sense that the company is going public for the first time, just not through the traditional process outlined in this article.

This is an increasingly popular form of transaction (as witnessed by the growth of SPACs), whereby the buyer purchases the target company (itself a public company), and then becomes a ‘shell’, with only its organizational structure remaining.

The shares of the company will be redistributed among the shareholders as per the terms agreed in the acquisition.

The best-known reverse merger of all was that of Berkshire Hathaway, the publicly listed holding company of Warren Buffett, the Sage of Omaha.

A former textile company, Buffett liquidated the textile company in 1985, but merged all of his other assets into the publicly listed Berkshire Hathaway, to become one of the world’s largest companies by market capitalization.

DealRoom has helped hundreds of companies with public and private M&A, allowing it to gain specific insights into both.

The project management tools that the DealRoom platform provides users with work equally well whether you’re planning a public or a private transaction.

Talk to us today about how we can add value to your M&A process.

.avif)

The Future of M&A: What Lies Ahead? (2024)

Get this guide and learn where the future of M&A is headed in today's volatile market conditions

.avif)

.avif)

.avif)

.avif)

Get your M&A process in order. Use DealRoom as a single source of truth and align your team.