US issuers completed 202 IPOs raising $44 billion in 2025, the strongest year for new listings since 2021, according to Renaissance Capital. During the same period, PitchBook and NVCA recorded 995 US venture-backed company acquisitions compared to just 62 public listings. Both metrics are talking about the same market. The IPO window has opened again, and a sale remains by far the more common exit path. As of June 2026 though, the numbers have swung back dramatically. OpenAI confidentially filed for an IPO on June 8, one week after Anthropic and three weeks after SpaceX's S-1. This page will track the upcoming and recent IPOs that matter and read each one like a board would: as one of two competing bids, with a private sale as the other option.

As an M&A advisor for 10 years before building DealRoom, I’ve observed this decision from both sides of the table. The trend holds true every time. The company that prepares for both options chooses their own destiny. The company that only prepares for one gets picked.

IPO or M&A: the 2025 exit math

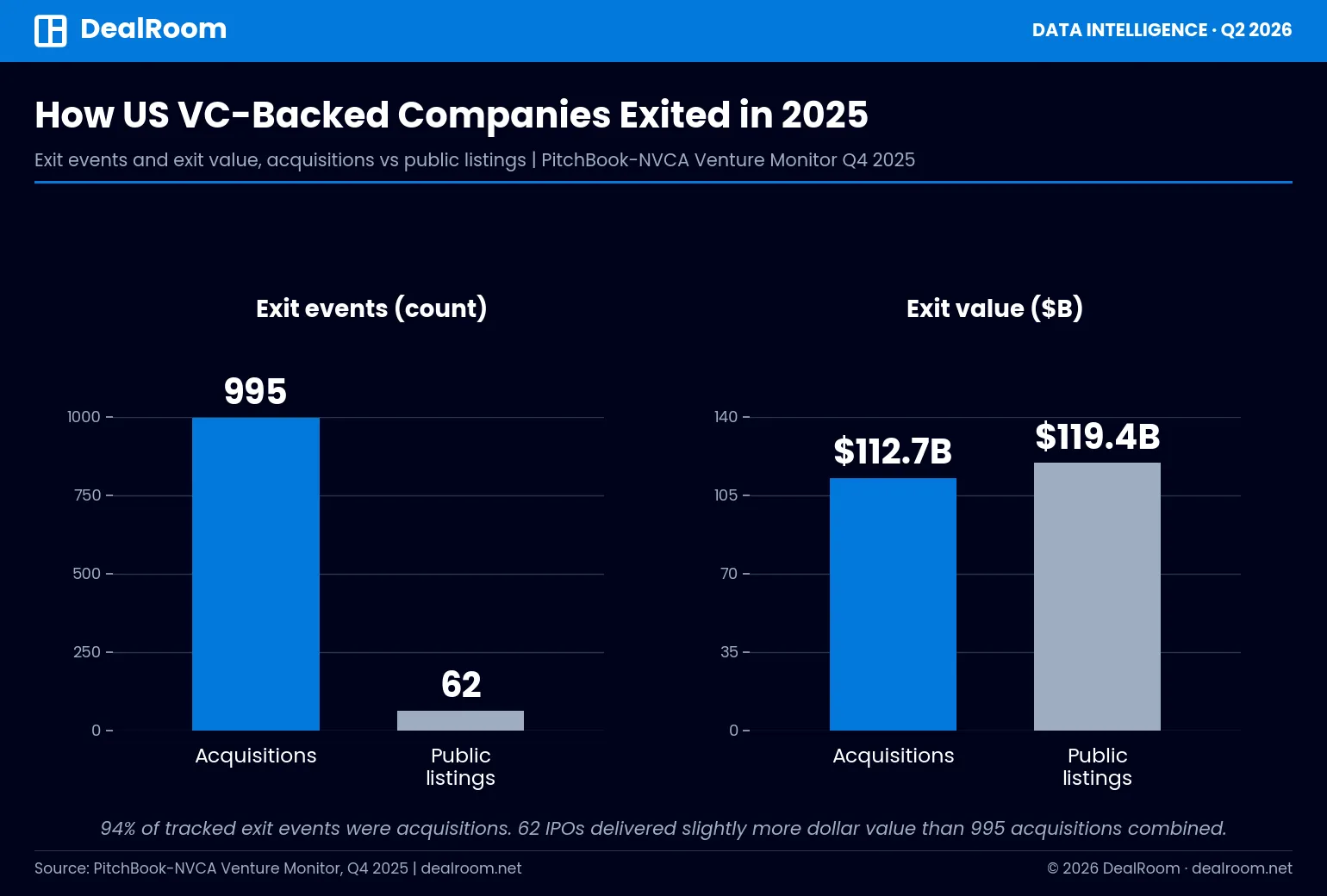

The two routes diverge. PitchBook and NVCA counted 995 acquisitions of US VC-backed companies valued at $112.7 billion in 2025 compared to 62 public listings worth $119.4 billion (Venture Monitor, Q4 2025). 94% of exit events were acquisitions. Listings nudged ahead of the dollar total because a few were gigantic. A sale is the realistic liquidity event for any given company. For the largest company in any vintage, the listing is where all the money pools.

The tumultuous 2026 backdrop is a double-edged sword. Renaissance Capital tallied 34 IPOs that raised $9.9 billion during Q1 2026 after volatility quelled a busy January. Uncertain markets are precisely the environment in which boards want to keep a sale process alive while the S-1 is pending with the SEC.

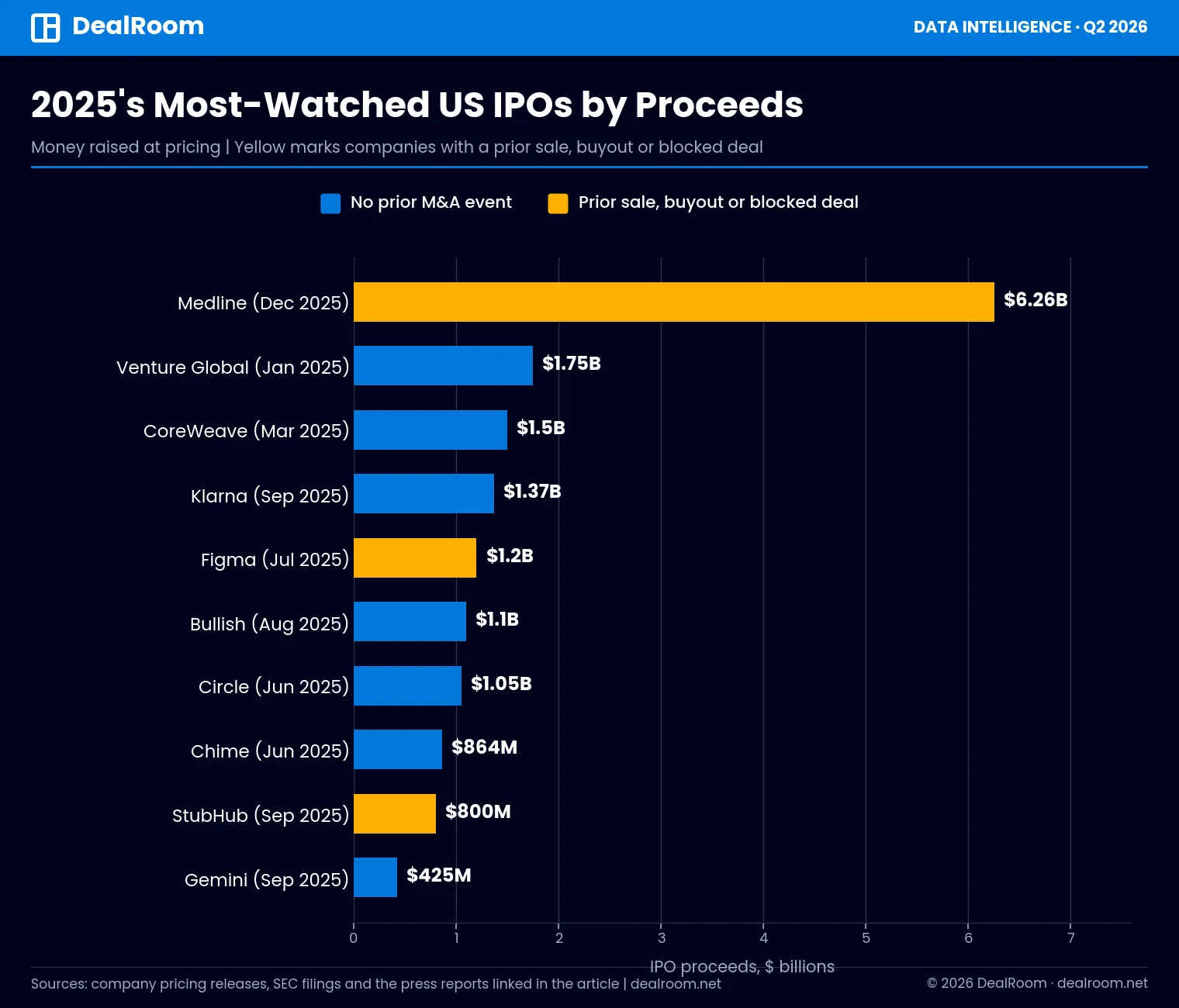

The 2025 IPO class, reframed: ten listings and their M&A backstories

These are the 10 most popular US offerings of 2025 by dollar raised at pricing. Start with the right column. Several had shares bought, sold or locked up prior to the exchange opening. That’s the piece of the IPO story most folks who follow IPOs ignore. Our list of the biggest IPOs of all time has the back story.

Could they have sold instead? Three readings from the 2025 class

Figma: the blocked sale that became the year's best debut

Adobe agreed to acquire Figma for $20 billion in September 2022. European and UK regulators refused to approve it. Adobe paid a $1 billion breakup fee when the companies parted ways in December 2023. Twenty months later Figma priced its IPO at a $19.3 billion valuation. Figma closed day one up 250% at $115.50. Regulators forced Figma’s owners to experience that upside. Few boards have that decision made for them. That’s exactly why there should be a real framework for the IPO vs sale decision, not a reflex.

Chime and Klarna: what waiting costs when the window moves

Chime filed at $11.6 billion, shy of half its $25 billion private valuation peak in 2021. Klarna’s journey was more tortuous: a $45.6 billion private peak in 2021, followed by an 85% tumble to $6.7 billion in 2022, only to go public at $15.1 billion in September 2025. Both companies are now public and trading. Both also demonstrate that an exit valuation is not permanent. If a board rejects a legitimate offer, it isn’t “locking in” a price. It is gambling that the door doesn’t close.

Medline: the IPO as a buyout's exit

The $6.26 billion IPO by Medline, the largest of 2025, was the exit for the $34 billion buyout led by Blackstone, Carlyle and Hellman & Friedman back in 2021. We highlighted the backlog of pressure built up behind sponsor-held assets in our State of M&A report. Buyout funds were holding about $1.1 trillion of dry powder out of roughly $4 trillion of dry powder across private capital. Equity that continues to concentrate will eventually need to recycle. When the IPO window opens, sponsor exits like Medline will be first through the door.

When the sale wins: dual-track deals that never reached the bell

The most compelling evidence that an IPO trajectory generates M&A pricing power is the deals done just days before pricing. Qualtrics originally expected to sell 20.5 million shares at between $18 and $21. That values the company at about $3.9 billion to $4.5 billion. Days before the stock was set to begin trading, SAP agreed to pay $8 billion in cash. That’s nearly double the high end of its expected IPO price range (via Fortune's account of the timing of events). SAP’s CEO at the time told analysts that Qualtrics’ IPO had already been oversubscribed when SAP signed the deal.

Bill McDermott, who was SAP's CEO at the time, laid out on the call why a strategic buyer would pay double what IPO math was implying:

“The legacy players who carried their ’90s technology into the 21st century just got clobbered. We have made existing participants in the market extinct.”

Source: TechCrunch's report on the SAP-Qualtrics call, November 2018. That is capability pricing. An IPO prices a company against its public peers. A strategic buyer prices what the company does to the buyer's competitive position, which is why the premium can clear any realistic public-market outcome.

Cisco executed the same playbook just one year earlier. AppDynamics filed at $12 to $14 per share ($1.7 billion valuation). Cisco offered $3.7 billion two days before the company was expected to price, more than doubling what was to be its public valuation. TechCrunch wrote that the final negotiation lasted about 72 hours, which speaks volumes about how quickly a motivated strategic buyer can move when a hard deadline is in place.

Wiz is a recent example. Wiz declined a $23 billion offer from Google in 2024 to continue progressing towards an IPO. They took $32 billion in March 2025 and closed in March 2026. Wiz had unique scale and category dominance to allow a board to say no once and then cash out later at a higher price. Most boards only get one offer.

How a dual-track process works

A dual-track process is one where you prepare an IPO and run a private sale process simultaneously. The private sale process typically is run as a quiet auction. Cooley's deal team authored the canonical article on dual track processes for the Harvard Law School Forum on Corporate Governance. Here is the practitioner version (presented in the order the work occurs).

- Build once, use twice. Audited financials, a clean cap table and a populated data room feed the S-1 drafting and buyer diligence at the same time. The duplicated cost of a dual track shrinks fast when the underlying artifacts are shared. Our due diligence guide covers the artifact list.

- File confidentially. Filing a confidential S-1 puts the SEC review clock in motion without making your financials public. OpenAI, Kraken and Discord all did this. It also allows your bankers to hold testing-the-waters meetings with public investors while the company is still dark.

- Open the quiet auction. A short list of strategic and financial buyers sign NDAs and receive a process letter. The live IPO is revealed as a legitimate option. The Cooley authors are candid that a feigned track undermines credibility with both crowds.

- Let the calendar do the work. Right before your roadshow date, every buyer has a true deadline, as opposed to a contrived one. Qualtrics and AppDynamics both signed inside of the final week because of this.

- Compare on certainty-adjusted terms. The board compares the indicative IPO range to the best bid: cash at closing vs. a locked-up position in a volatile stock, regulation risk on the deal vs. pricing risk on the listing, as well as the continued expenses of being public.

- Close one track and stand the other down. If the sale signs, the S-1 is withdrawn. If the listing prices, buyers are told the process is over. Either way you didn't waste the losing workstream; it set the price.

The Cooley authors clearly explain why the structure pays for itself:

“Conversely, knowledge that a company may be pursuing an IPO exit could drive the M&A valuation higher, particularly with strategic buyers. The optionality afforded by a dual-track process should be maintained for as long as possible to keep maximum pressure on timing, valuation and general competitive tension.”

Michal Berkner and Josh Kaufman, partners at Cooley LLP, via the Harvard Law School Forum on Corporate Governance. Maintained optionality is the entire product. The moment one track becomes a bluff, both lose pricing power.

The board's framework: six factors that decide between an IPO and a sale

Every board discussion of exits ultimately comes down to these six trade-offs. Think of the table as a checklist, not a scoring model. Weights vary by company and by window.

Monzo is a recent case study proving just how contested these weights become. In December 2025, its board reportedly ousted its CEO over when to list. He wanted to list earlier; directors wanted more scale first. The framework above is not hypothetical. It’s the debate playing out in boardrooms today.

The scorecard below turns that framework into a quick self-assessment for operators and deal teams. It will give you a leaning, not a verdict.

For acquirers: what to do when the target is on an IPO track

An S-1 is public diligence for free. As soon as a target publicly files, you get audited financials, risk factors, customer concentration and the cap table. Read it like you would any CIM. Load it into your deal pipeline with a dated trigger: the anticipated pricing window.

Qualtrics signed days before pricing, and AppDynamics signed just two days before pricing. Once management starts pitching the deal to public shareholders, your board-approved reference price converts to an order book and your premium math becomes more difficult every hour.

Relative to an IPO, the buyer’s structural advantage is something the seller can count on: cash at closing, no financing condition, no lock-up, no first-earnings call risk. In our State of M&A report we called the strongest acquirers strategic collaborators transacting to transform: thinking big and buying into adjacent capabilities intentionally, not opportunistically. It’s that kind of discipline that allows a buyer to pay a Qualtrics-type premium confidently and walk away when the numbers don’t work.

Run your own clock. If you're on an IPO bankers' calendar, then reactive buyers start off at a disadvantage. Playing vs. a listing requires a calibrated buy-side process, complete with pre-approved approvals and a diligence plan that folds into weeks. You develop that kind of corporate development muscle before the S-1 filing, not afterward.

If you miss the window, there is still life after the bell. There is a standard 180-day lock-up period post listing, and previously unreachable IPO companies that break issue start to become reachable again. StubHub ended its first day of trading below the offering price. Companies in this position receive very different phone calls six months after the bell than they do six months before it.

The 2026 pipeline through an M&A lens

No watch list has featured companies like those on the run to market in 2026. SpaceX submitted its S-1 on May 20, 2026, aiming to price at a $1.75 trillion valuation, TechCrunch reported. Anthropic filed for its IPO on June 1 following its $65 billion funding round in late May. OpenAI filed confidentially on June 8 at an $852 billion private valuation. None of the above are investable companies. They're still interesting to dealmakers: the flood of public-market capital these companies will absorb sets the pricing backdrop for every smaller IPO and dual-track process behind them.

Sources: TechCrunch on SpaceX's filing, on OpenAI's filing, on Anthropic's filing and its May round, Databricks' announcement and CNBC on the completed round, Benzinga on Discord's reported filing and TechCrunch on the 2021 Microsoft talks, CNBC on Kraken, CNBC on Visa-Plaid with TechCrunch on Plaid's 2025 secondary and 2026 employee sale, Revolut's announcement and TechCrunch on Monzo.

Frequently Asked Questions

What does dual-track process mean?

Dual track process refers to running an IPO process and a private M&A sale process simultaneously, typically in the form of a quiet auction. The company files a confidential S-1 while the bankers reach out to a short list of buyers under NDA. The board remains open to both options until the last minute and chooses which path to close based on which offers more certainty-adjusted value. Both Qualtrics and AppDynamics completed dual track processes with a sale just days before their IPO pricings were expected to occur.

Do companies receive a better valuation from an IPO or from a sale?

It depends who is bidding. SAP acquired Qualtrics for roughly twice the high end of its IPO range. Cisco acquired AppDynamics for about 2x its expected IPO price. Strategic acquirers who can capitalize on synergies can exceed public market valuations. A notable counterexample is Figma. Their $20B sale was blocked by regulators in 2023. In 2025, Figma priced its IPO 250% higher than the offer price and closed its first day of trading up 250% from there.

How many IPOs were there in 2025 and how does this compare to M&A?

According to Renaissance Capital, there were 202 IPOs that raised $44 billion in 2025. This marked the busiest year for IPOs since 2021. PitchBook and NVCA tracked 995 acquisitions of US venture-backed companies and 62 public listings of venture-backed companies during 2025. Venture-backed companies were 16 times more likely to be sold than go public by deal count.

Which companies have filed IPOs recently?

SpaceX's S-1 was filed on May 20, 2026. Anthropic's IPO filing was announced on June 1, 2026. OpenAI confidentially submitted an S-1 on June 8, 2026. Other confidential filings rumored in the press include Kraken in November 2025 and Discord in January 2026.

What do you do when a target files for an IPO?

View the filing as a deadline and the prospectus as gratis diligence. The opportunity to sign a deal will likely end when the roadshow begins. Bid with conviction with price including cash at closing, no financing condition and a confirmatory diligence plan that's measured in weeks, not months. SAP and Cisco each closed within days of their target's intended pricing dates.

What is an IPO lock-up and why does it matter in M&A?

An IPO lock-up is simply a contractual prohibition (usually lasting 180 days) preventing insiders from selling their shares following a listing. It matters to dealmakers in two ways. First, it's part of what a seller sacrifices by opting for an IPO instead of a cash sale. IPO proceeds received by insiders are delayed and uncertain. Second, expiration of the lock-up is typically when a newly public company with a poor chart once again becomes vulnerable to a takeover bid.

Methodology

Exit-mix data is from PitchBook-NVCA Venture Monitor, 4th Quarter 2025. IPO market counts are from Renaissance Capital's 2025 Annual Review and Q1 2026 Review. Deal values, IPO prices and proceeds are sourced to filings and publications cited at first reference and were verified June 2026. The 2025 listings table includes the year's ten most-watched US IPOs by reported proceeds; it is a curated watch list, not a comprehensive league table. Pipeline counts reflect public filings and named-outlet reporting as of June 11, 2026. Confidential filings have no public financials, so the listed valuations are the latest private marks.

.avif)