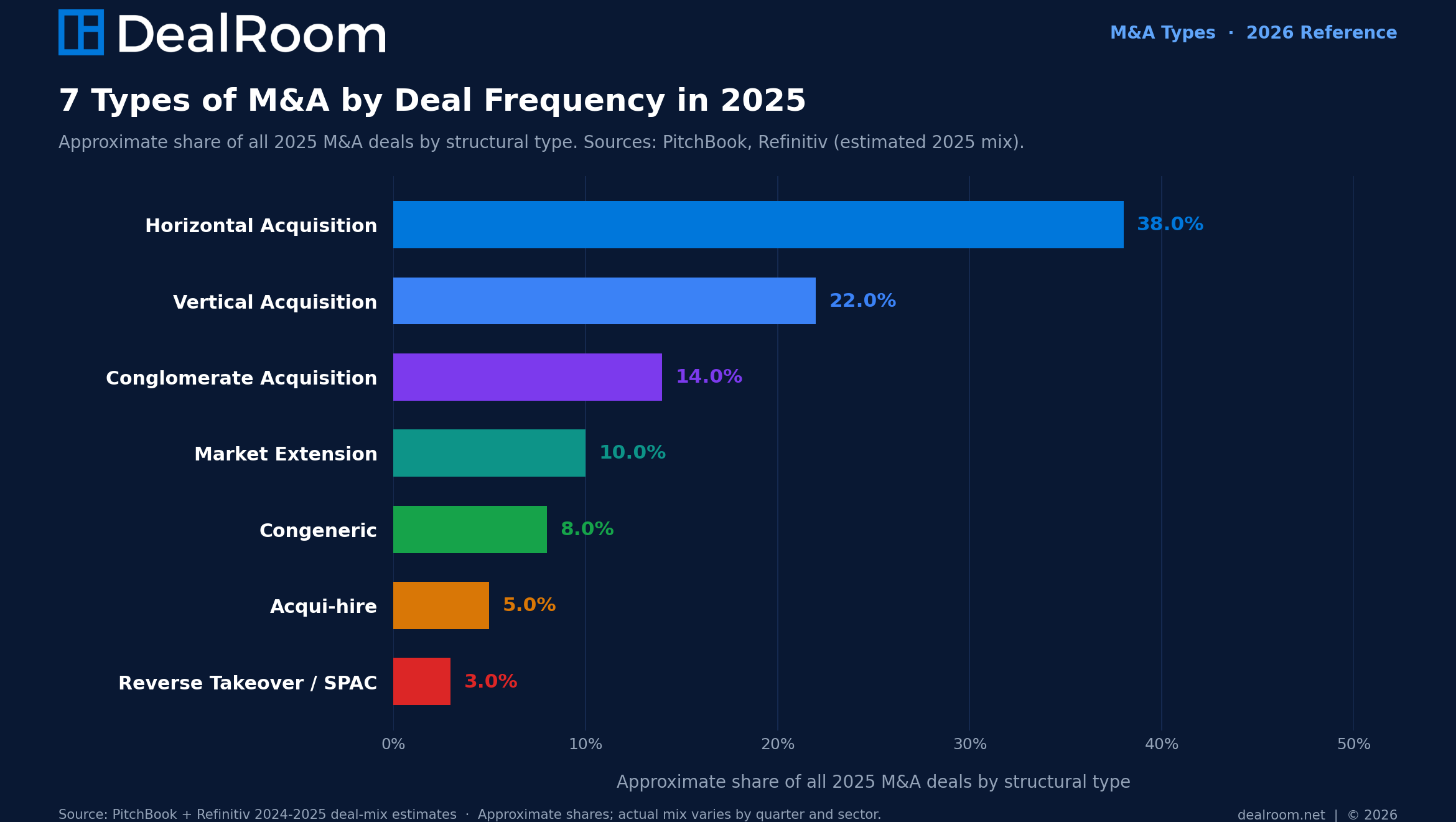

There are 7 main types of mergers and acquisitions: horizontal (Disney + 21st Century Fox, $71B 2019), vertical (Amazon + Whole Foods, $13.7B 2017), conglomerate (Berkshire Hathaway + BNSF Railway, $44B 2009), market extension (Walmart + Flipkart, $16B 2018), congeneric (Google + Fitbit, $2.1B 2021), acqui-hire (Microsoft + Inflection AI, ~$650M 2024), and reverse takeover / SPAC (Lucid Motors + Churchill Capital IV, $24B 2021). Horizontal acquisitions are the most common structural type (~38% of all 2025 M&A deals), followed by vertical (~22%) and conglomerate (~14%).

Each type has a distinct strategic rationale, a typical risk profile, and a different regulatory posture. Below: a side-by-side comparison with definition, rationale, real example, and key risk per type, plus a 6-question wizard that recommends the right type for your strategy.

DealRoom has worked with companies on every manner of deal, so we decided to provide readers with a brief overview of each type of acquisition, along with a series of tools and vizualizations.

We built this simple Types of M&A comparison tool to let you compare different types of M&A:

7 Types of Mergers and Acquisitions: Side-by-Side

Definition, strategic rationale, a real-world deal example, and the key risk for each of the 7 main M&A structural types. 2026 reference.

Or checkout the interactive quiz we built to help you determine which M&A type is the best fit for you:

Find the right M&A type for your strategy

Answer 6 quick questions about your strategic objective, target relationship, and post-close plan. We’ll match you to one of the 7 M&A structural types and explain why.

The 7 Types of M&A

- Horizontal Acquisition

- Market Extension Acquisition

- Vertical Acquisition

- Conglomerate Acquisition

- Congeneric Acquisition

- Reverse Takeover (SPAC)

- Acqui-hire

Below is a more in-depth look at each of the 7 M&A types, along with specific examples of each.

1. Horizontal Acquisition

A horizontal acquisition is when a company buys a direct competitor in the same industry and at the same point in the supply chain.

Strategic rationale: market share, pricing power, scale economies, headcount and overhead consolidation.

Real example: Disney + 21st Century Fox ($71B, 2019) Disney acquired Fox's film and TV studio assets to scale its content library and seed the Disney+ launch.

Key risk: antitrust review and regulatory delay; cultural integration of two organisations of similar size.

The increased scale of the new company should give it greater bargaining power and a stronger competitive position than the two companies had when they were on their own. In most industries, the largest players either obtained or maintained their leadership position through horizontal acquisitions.

How does it create value?

A horizontal merger leads to greater economies of scale in the market(s) in which the company operates. It is also likely to lead to lower operating costs, as the companies can share production facilities, distribution channels, and human capital.

Horizontal Merger Example

The 1999 merger of Exxon and Mobil to create ExxonMobil could be seen as the textbook case of a horizontal merger. Two companies with the exact same output (very rare, given that all consumer products are at least a little different).

The combined firm was the largest in the world at the time of the merger, creating an undisputed leader in the oil and gas industry and creating hundreds of millions of dollars in cost and revenue synergies.

2. Market Extension Acquisition

A market extension acquisition is when a company buys a target that sells the same product but in a different geographic market.

Strategic rationale: geographic expansion without organic build-out; instant local distribution, brand, and regulatory presence.

Real example: Walmart + Flipkart ($16B, 2018) Walmart (US retail) acquired Flipkart (India e-commerce) to enter the Indian retail market.

Key risk: local regulatory and cultural barriers; FX risk; underestimating local-competitor strength (Flipkart vs Amazon India remains intensely competitive).

Cross-border acquisitions are the most common form of market extension, and are particularly prevalent in industries such as food retail and retail banking.

In these industries, the typically high levels of consolidation that exist incentivize new companies entering the market to undertake acquisitions rather than starting greenfield operations in the new geography.

How does it create value?

The market extension merger creates value primarily through revenue synergies. There may also be some technology synergies to be shared across the countries. Cost synergies tend to be lower here, as companies will retain most operations in each country even after the merger.

Market Extension Merger Example

In early 2022, two innovative shipbuilders, Wight Shipyard from the UK and OCEA from France, combined in an all-share merger that gave both increased access to their respective markets and enhanced resources to take on larger players. The market extension merger enabled both companies to double their size.

3. Vertical Acquisition

A vertical acquisition is when a company buys a supplier (backward integration) or a customer / distributor (forward integration) within its own value chain. Strategic rationale: margin capture, supply security, channel control, lower transaction costs.

Real example: Amazon + Whole Foods ($13.7B, 2017) Amazon (e-commerce) acquired Whole Foods (physical retail + fresh-food supplier) to enter grocery and acquire ~470 physical retail locations.

Key risk: integration complexity across very different operating models; channel-conflict if other suppliers or customers feel disadvantaged.

How does it create value?

A vertical merger creates value by lowering costs (thereby creating value) in the value chain, which can then be passed on to consumers, creating a more competitive value proposition, or to shareholders, enhancing shareholder returns.

Vertical Merger Example

In the strictest sense of the term ‘merger’, vertical mergers are extremely rare: The reality is that vertical transactions are usually acquisitions, as a much larger company buys one of its partners or suppliers, enabling it to ensure better control of its value chain.

An example of this occurred when UK frozen food retailer Iceland acquired Loxton Foods in 2012, allowing it to gain control of one of the many producers it worked with and to bring food production in-house.

4. Conglomerate Acquisition

A conglomerate acquisition is when a company buys a target in an unrelated industry, with no direct supply-chain or product overlap.

Strategic rationale: diversification of revenue streams, capital allocation across cycles, capture of underpriced assets.

Real example: Berkshire Hathaway + Burlington Northern Santa Fe ($44B, 2009) Berkshire (insurance + conglomerate holding) bought a Class I freight railroad with no operating overlap; pure capital-allocation play.

Key risk: lack of operating synergies; markets often discount conglomerates ("conglomerate discount") because focused peers outperform.

Everybody is familiar with the names of the world’s largest consumer product conglomerates, such as Procter & Gamble, Nestlé, GlaxoSmithKline, and others. When we think of their product lines, they can include anything from pet food to detergent, dairy products to frozen foods.

Related: Examples of Conglomerate Mergers

How does it create value?

The consensus now among academics is that there isn’t much value created from the merger itself - the value generation comes from each of the companies being managed well, which would have happened without the merger. It is possible that both can gain from a larger consolidated balance sheet and the greater benefits that it brings.

Conglomerate Merger Example

Amazon’s 2017 acquisition of Whole Foods Market is a classic example of a conglomerate transaction. Amazon’s core business in e-commerce, cloud computing, and digital services had little direct overlap with Whole Foods’ brick-and-mortar grocery operations. The deal represented a diversification move rather than a horizontal or vertical expansion, allowing Amazon to enter a new industry while leveraging its scale, logistics capabilities, and customer data across a fundamentally different business model.

Related: Examples of Conglomerate Mergers

5. Congeneric Acquisition

A congeneric acquisition is when a company buys a target in a related (but not directly competing) industry that shares technology, distribution, or customer base.

Strategic rationale: cross-sell into the existing customer base; technology or capability extension into adjacent products.

Real example: Google + Fitbit ($2.1B, 2021) Google (software / Android) acquired Fitbit (wearables hardware) to extend into the wearables category and gather health data for its services.

Key risk: slower payoff than horizontal deals; regulatory scrutiny on data and privacy; integration of different product cultures (Google delayed close by 14 months for EU competition review).

This overlap between the companies creates synergies (whereby the two companies become greater than the sum of their parts). A typical example usually given by corporate finance textbooks, which exhibits this distinction in a simple fashion, is an ice-cream manufacturer buying a wafer manufacturer.

How does it create value?

The product extension merger primarily creates value through revenue synergies, although cost synergies are a secondary benefit. The principal idea for value generation here is that both companies can create significant cross-selling opportunities through the merger.

Congeneric Acquisition Example

The $90 billion all-share merger between mining firm Xstrata and commodities trader Glencore in 2012 is an interesting example of a product-extension merger. Under the deal, the players said they would create a ‘natural resources group’ that could trade the commodities as soon as they were mined. In this respect, it could also be seen as a vertical merger, in that one was upstream of the value chain of the other.

Related: Acquisition Examples

6. Reverse Takeovers / SPACs (Special Purpose Acquisition Companies)

A reverse takeover (or SPAC merger) is when a private company goes public by merging with an already-public shell company or Special Purpose Acquisition Company (SPAC), bypassing the traditional IPO process.

Strategic rationale: faster path to public markets than a traditional IPO; price certainty pre-merger; capital flexibility (PIPE structure).

Real example: Lucid Motors + Churchill Capital IV ($24B, 2021) Lucid Motors (private EV maker) merged with Churchill Capital IV (SPAC) to go public, the largest SPAC merger to date at the time.

Key risk: post-merger price collapse if growth expectations don't hold (the median 2021 SPAC has lost 60%+ of value); regulatory scrutiny under tightened SEC SPAC rules from 2024.

A SPAC or Special Purpose Acquisition Company is a shell company that raises capital through an IPO with the sole purpose of merging with or acquiring a private company. For the target company, it's a faster, cheaper alternative to a traditional IPO.

SPAC vs. traditional IPO: the key differences

Pros & Cons of going public via SPAC:

Pros:

- Speed to market — significantly faster than a traditional IPO

- Price certainty — terms are negotiated, not subject to market volatility

- Access to the SPAC sponsor's expertise and network

Cons:

- Dilution risk for shareholders if warrants are exercised

- Reputational concerns — SPAC-listed companies faced heavier post-merger scrutiny during the 2020–2022 boom

- Less regulatory oversight can cut both ways

Notable SPAC examples include DraftKings, Virgin Galactic, and Lucid Motors — all of which used SPACs to go public during the 2020–2021 surge, when over 600 SPACs launched in a single year.

7. Acqui-hire

At a time when the biggest companies in the world are defined as much by their talent and intellectual property as their capital assets, the acqui-hire form of acquisition is a proven way for companies to ensure that they’re winning the talent race in their industry.

This is most commonly seen in the technology sector, where a shortage of programmers at the very highest levels means that the big tech companies will do almost anything to get their hands on value-adding talent - including buying their company.

Acqui-hire Acquisition Example

Facebook’s 2010 acquisition of Drop.io is a well-known acqui-hire example.

Drop.io was a small file-sharing startup with limited commercial traction. Following the acquisition, Facebook shut down Drop.io’s product, but retained its founder and core team. Most notably, Sam Lessin, the CEO of Drop.io, joined Facebook and later held senior product leadership roles. The primary motivation behind the deal was not Drop.io’s technology or customer base, but the opportunity to bring experienced entrepreneurial and technical talent into Facebook during a period of rapid growth.

The table below breaks down the most common M&A types and how they differ in practice. It shows what each deal structure typically aims to achieve, where synergies come from, and what tends to go wrong after close.

| M&A Type | Primary Goal | Typical Synergies | Integration Complexity | Common Risks |

|---|---|---|---|---|

| Horizontal Acquisition | Increase market share and scale | Cost: economies of scale; Revenue: pricing power | High | Antitrust scrutiny; culture clashes; integration drag |

| Market Extension Acquisition | Expand into new geographies | Revenue: new customers; Cost: limited overlap | Medium | Regulatory differences; market misreads |

| Vertical Acquisition | Control supply chain and margins | Cost: lower input costs; Revenue: pricing flexibility | Medium | Operational complexity; supplier lock-in |

| Conglomerate Acquisition | Diversify into new industries | Revenue: diversification; Cost: minimal synergies | High | Management distraction; weak strategic fit |

| Congeneric Acquisition | Expand product or service offerings | Revenue: cross-selling; Cost: shared functions | Medium | Overestimated synergies; product overlap |

| Reverse Takeover (SPAC) | Achieve public listing efficiently | Capital access; Talent credibility | High | Valuation risk; governance gaps |

| Acqui-hire | Acquire talent and expertise | Talent acquisition; leadership depth | Low | Talent attrition; limited IP value |

And this explainer breaks down how to choose the right type of M&A:

Common Integration Challenges by Deal Type

Each acquisition type has its own integration challenges. Most are predictable, yet many still get underestimated.

Horizontal acquisitions struggle with culture first. Teams overlap, and roles get cut. Morale drops fast if decisions drag. Antitrust scrutiny can also limit how quickly systems and pricing can be combined, slowing value capture.

Vertical acquisitions introduce operational dependencies. The buyer becomes tied to internal suppliers or distribution paths that may not perform as expected. Lock-in reduces flexibility if demand shifts or costs rise.

The success of acqui-hires is driven by retention. If key people leave, the deal loses its purpose. Incentives, reporting lines, and autonomy matter more than process integration.

Conglomerate acquisitions suffer from weak strategic focus. Leadership attention spreads thin. Without a clear operating model, the acquired business drifts instead of improving.

How to Choose the Right Type of Acquisition for Your Strategy

Most companies don’t sit down and decide to pursue a specific type of acquisition. The strategy usually makes that decision for them.

1. Start with the Outcome You Want

If the goal is growth, consider horizontal or market-extension deals. These expand revenue, customers, or geography. They usually come with heavier integration work and more overlap to unwind.

If the goal is efficiency, vertical or congeneric acquisitions make more sense. These deals focus on cost control, margin improvement, or tighter operations. The value often comes from process changes, not headline growth.

If the goal is diversification, conglomerate deals enter new markets or products. These reduce dependence on one business line but increase execution risk. Management attention gets stretched fast.

2. Assess Your Risk Tolerance

Some deals look great on paper but fall apart in execution. Complex integrations, cultural mismatch, and regulatory scrutiny add real friction. The more transformative the deal, the higher the risk.

3. Consider Time-to-Value

Some acquisitions pay off quickly through cost savings or cross-selling. Others take years to justify the price. If leadership expects near-term results, that narrows the field fast.

In practice, companies don’t choose an acquisition type. They choose a strategy, and the structure follows - whether they plan it or not.

Regulatory & Antitrust Considerations Across M&A Types

Not all acquisitions trigger the same level of regulatory attention.

Horizontal mergers face the most scrutiny. Combining direct competitors raises clear concerns around pricing power, market concentration, and customer choice. Even mid-market deals can attract regulators if the overlap is obvious.

Cross-border deals add another layer of complexity. Different countries bring different approval processes, timelines, and enforcement standards. Data privacy, labor rules, and national interest reviews often surface late if teams are not prepared.

Early due diligence reduces risk more than legal cleanup after signing. Market share analysis, customer concentration, and regulatory exposure should be reviewed before the deal structure is locked. Waiting too long limits options and slows deal progress.

Frequently Asked Questions

What are the different types of M&A?

The main types of mergers and acquisitions are horizontal, vertical, conglomerate, and market-extension deals. Each serves a unique purpose, from increasing market share to expanding supply chains or diversifying operations.

What is a horizontal merger?

A horizontal merger occurs when two companies in the same industry and at the same stage of production combine. It helps reduce competition and often creates cost advantages through shared resources.

What is a vertical merger?

A vertical merger occurs between companies at different stages of the supply chain. For example, a manufacturer may merge with a supplier to gain better control over production and pricing.

What is a conglomerate merger?

A conglomerate merger involves companies in unrelated industries. These deals aim to diversify business risk and build broader corporate portfolios.

What is a market-extension merger?

A market-extension merger happens when companies selling similar products in different regions join forces. This helps them reach new markets and grow their customer base.

What is the difference between a merger and an acquisition?

In a merger, two firms agree to form a new entity. In an acquisition, one company purchases another and assumes control of its operations, assets, and management.

Why do companies pursue mergers and acquisitions?

Companies pursue M&A deals to grow faster, gain market share, enter new regions, or access technology and talent. M&A can also improve efficiency by combining complementary strengths.

Key Takeaways

- Mergers and acquisitions come in multiple distinct forms, and each type (horizontal, vertical, conglomerate, congeneric, market extension, reverse takeover, and acqui-hire) creates value in different ways depending on whether the goal is scale, market access, supply-chain control, diversification, public listing, or talent acquisition.

- Choosing the right type of acquisition early is a strategic decision that shapes target selection, deal structure, and post-merger outcomes, making a clear understanding of M&A types critical to long-term corporate development success.

In the most basic terms, an acquisition is a transaction in which one company buys another. But as this article shows, that transaction can take many different forms and have many underlying motivations.

Understanding these will help you assess whether your corporate development strategy adequately addresses your company’s long-term goals. If you want to dive deeper, check out this video on M&A best practices:

Or talk to us at DealRoom about how we can help you in this process.

.avif)

.avif)

.avif)