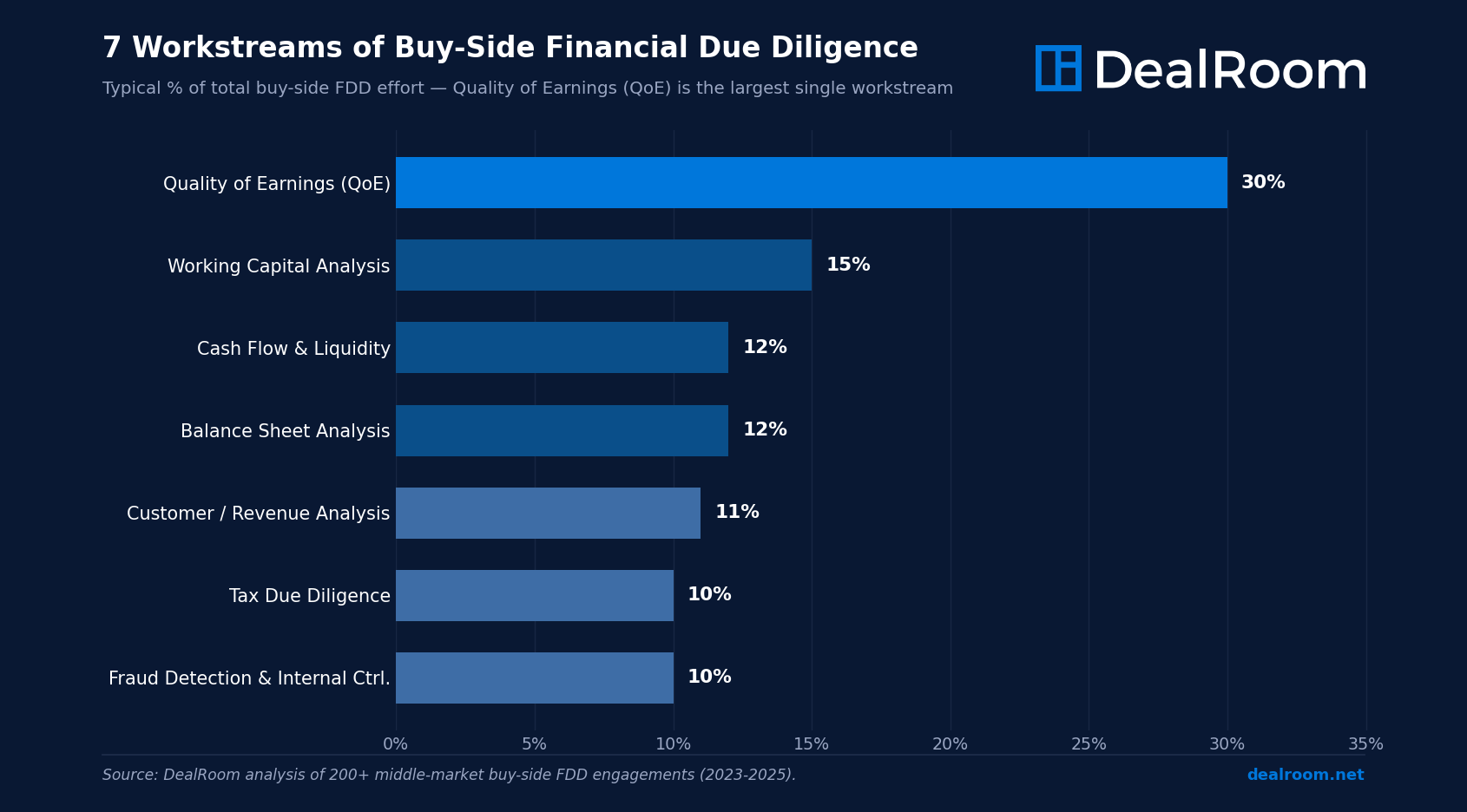

Financial due diligence (FDD) is the buy-side review that validates a target company's earnings, working capital, cash flow, and balance sheet before an acquisition closes. A typical middle-market financial due diligence process runs 4-6 weeks and is structured around 7 workstreams: Quality of Earnings (QoE) which alone drives roughly 30% of total effort followed by Working Capital Analysis (15%), Cash Flow & Liquidity (12%), Balance Sheet Analysis (12%), Customer / Revenue Analysis (11%), Tax Due Diligence (10%), and Fraud Detection & Internal Controls (10%).

The deliverables are an Adjusted EBITDA bridge, a Net Working Capital target for the purchase agreement, a debt and cash schedule, and a risk register of red-flag findings. Unlike an audit (which gives an opinion on historical statements), FDD produces a forward-looking valuation and risk view the acquirer uses to negotiate price, structure escrow, and plan integration. Sell-side FDD mirrors the same 7 workstreams but is prepared by the seller to pre-empt buyer findings and support a higher valuation. Use the interactive 53-item checklist below to track your draft, or compare buy-side vs sell-side scope side-by-side to scope your engagement.

We've built tools to help you through the financial due diligence process. First, use the free interactive financial due diligence interactive checklist:

Financial Due Diligence Checklist (7 Workstreams, 53 items)

Tick off each item as you review. Filter by workstream or search across all items. Progress saved per session.

And this buy-side versus sell-side due diligence side-by-side comparison:

Buy-Side vs Sell-Side Financial Due Diligence

Side-by-side comparison of focus, documents, timeline, and team across both perspectives.

What is Financial due diligence?

Think of financial due diligence as a deep investigation into a company’s financial statements—its income statement, balance sheet, and cash flow reports. While an audit verifies the accuracy of these documents, financial due diligence goes beyond. It's about asking questions like, "Are the numbers sustainable?" and "What are the hidden liabilities?"

For example, consider a small tech startup with impressive revenue growth. Everything looks solid at first glance, but financial due diligence reveals that a single large client accounts for 60% of their sales. What happens if that client leaves? This is the kind of insight you gain through financial due diligence—understanding the true quality of earnings.

The financial due diligence checklist

When conducting financial due diligence, you and your team should approach the process like an audit committee, working through seven distinct workstreams that together cover the financial health of the target. The seven workstreams below account for 100% of typical buy-side financial due diligence effort. Quality of Earnings is the largest single workstream, followed by Working Capital, Cash Flow and Liquidity, Balance Sheet, Customer and Revenue, Tax, and Fraud Detection. Use the interactive checklist embed above to track progress on all 53 standard items.

1. Quality of Earnings (QoE)

Quality of Earnings is roughly 30% of buy-side financial due diligence effort, the single largest workstream, and covers EBITDA reconciliation, identification of one-time and non-recurring items, and pro-forma run-rate adjustments. The deliverable is an Adjusted EBITDA bridge that takes management's reported figure to a normalized, defensible run-rate number used in valuation.

- Reconcile reported EBITDA to audited or bank books, line by line.

- Identify one-time and non-recurring items: litigation settlements, restructuring charges, owner perks, gains or losses on asset sales.

- Apply pro-forma adjustments for recent acquisitions, dispositions, and divestitures so the trailing-twelve-months figure reflects the go-forward business.

- Apply run-rate adjustments for recent hires, cost actions, and pricing changes.

- Review the revenue recognition policy for ASC 606 compliance, particularly for subscription, contract, or milestone-based revenue.

- Build an EBITDA bridge from reported, to management-adjusted, to QoE-adjusted, with a supporting schedule for every adjustment.

- Analyze gross margin and EBITDA margin trends across the last three to five years, and explain any inflection.

Sell-Side Financial Due Diligence: Why Sellers Now Commission Their Own QoE

Ten years ago, sell-side QoE was reserved for mega-deals. Today it's standard practice in most middle-market processes and increasingly common at the lower end. Sellers commission a sell-side QoE report before launching the sale process for three reasons:

- Narrative control. The seller's QoE sets the EBITDA baseline buyers anchor on. A clean, well-supported sell-side QoE can lift the marketed multiple by 0.5-1.0x.

- Pre-empt buyer findings. Issues a buyer would otherwise discover (and use to chip price) get surfaced and addressed in the seller's report with management's framing.

- Compress confirmatory diligence. A buyer who trusts the sell-side QoE may scope confirmatory FDD to 2-3 weeks instead of 5-6, accelerating to close.

The trade-off: a sell-side QoE costs $75K-$300K (middle market) and requires the seller to disclose findings the buyer would not necessarily have discovered. Sellers with clean books almost always recoup the cost in valuation. Sellers with messier financials should think twice once disclosed, an issue cannot be un-disclosed.

2. Working Capital Analysis

Working Capital Analysis is roughly 15% of buy-side financial due diligence effort and covers net working capital target setting, days sales outstanding, days payable, and inventory days trend analysis, and seasonality normalization. The deliverable is the net working capital peg locked into the purchase agreement, plus the post-close true-up methodology.

- Compute trailing-twelve-month average operating working capital (accounts receivable plus inventory minus accounts payable minus accrued expenses), excluding cash, debt, and deferred revenue.

- Track days sales outstanding (DSO), days payable outstanding (DPO), and days inventory outstanding (DIO) on a 36-month rolling basis to spot trend breaks.

- Adjust for seasonality by computing 12-, 24-, and 36-month averages, and weight months consistently with the closing date.

- Pull an accounts receivable aging report (current vs 30, 60, 90, and 120-plus days) and reserve for collectibility risk.

- Define the working capital peg: the agreed dollar target locked into the purchase agreement.

- Document the post-close true-up window (typically 60 to 90 days) so the buyer can recompute actual delivered working capital and adjust price dollar-for-dollar against the peg.

3. Cash Flow and Liquidity

Cash Flow and Liquidity Analysis is roughly 12% of buy-side financial due diligence effort and covers free-cash-flow reconciliation, capital-expenditure split between maintenance and growth, and the debt schedule with covenant review. The deliverable is the cash bridge from EBITDA to reported cash and the debt and cash schedule used to compute equity value at close.

- Reconcile free cash flow for the last five years, starting from EBITDA and working down through changes in working capital, capex, taxes paid, and interest paid.

- Split capex between maintenance (required to keep the business running) and growth (required only to expand). Acquirers underwrite to maintenance capex.

- Build a complete debt schedule: principal balance, interest rate, maturity date, covenants, prepayment penalties, and change-of-control triggers.

- List off-balance-sheet liabilities including operating leases under ASC 842, contingent liabilities, and earn-out obligations.

- Analyze the cash conversion cycle (DSO plus DIO minus DPO) and explain any deterioration.

- Run a sensitivity analysis: if operating cash flow drops by 30%, can the company still cover loan interest and required capex?

- Define minimum cash for ongoing operations so the closing cash balance can be set correctly.

4. Balance Sheet Analysis

Balance Sheet Analysis is roughly 12% of buy-side financial due diligence effort and covers asset write-down and impairment review, intangible-asset and goodwill testing, and pension and post-retirement obligation analysis. The deliverable is a schedule of off-balance-sheet exposures (operating leases under ASC 842, contingent liabilities, related-party balances) folded into the indicative valuation.

- Review asset write-downs, impairments, and reserve releases for the last three years.

- Test intangible assets and goodwill for impairment indicators, particularly where the carrying value sits well above current operating performance.

- Quantify pension and post-retirement obligations, including funded status and other post-employment benefits.

- Review deferred tax assets and liabilities, including any valuation allowance against deferred tax assets that may be released or written down.

- Identify all related-party balances and disclosures, and confirm that pricing on related-party transactions is at arm's length.

- Validate cash and cash equivalents (restricted vs unrestricted) and reconcile to bank statements for the last three months.

- Review marketable assets that could be liquidated (excess inventory, idle real estate, surplus equipment) and assess whether they would fetch more or less than book value.

5. Customer and Revenue Analysis

Customer and Revenue Analysis is roughly 11% of buy-side financial due diligence effort and covers customer-concentration analysis, cohort retention and churn modeling, and pricing review. The deliverable is a revenue-quality scorecard (concentration risk, retention durability, pricing power) that supports the projection model.

- Compute customer concentration: top 10 and top 25 customers as a percentage of total revenue, plus top customer as a percentage of total.

- Break revenue out by product, segment, and geography to identify hidden concentration or declining lines.

- Build cohort retention and churn analysis: track each annual cohort's revenue retention over time.

- Compute customer acquisition cost and payback period, particularly for subscription or recurring-revenue businesses.

- Analyze recent pricing changes and build a price, volume, and mix bridge to explain reported revenue growth.

- Review forward bookings and pipeline (12 to 24 months out) and assess conversion rates against historical norms.

- Read the top 10 customer contracts: term, renewal, exclusivity, termination for convenience, and most-favored-nation clauses.

6. Tax Due Diligence

Tax Due Diligence is roughly 10% of buy-side financial due diligence effort and covers federal, state, and local filing review, net-operating-loss and carryforward analysis, and transfer-pricing and multi-state nexus review. The deliverable is a tax exposure schedule and a Section 382 limitation analysis for post-acquisition NOL utilization.

- Review federal, state, and local tax filings for the last three years.

- Quantify net operating losses (NOLs) and tax credit carryforwards, including any limitations.

- Run a Section 382 limitation analysis to determine how much of the target's NOLs the acquirer can use post-close.

- Review international tax positions and transfer-pricing documentation, particularly for cross-border transactions.

- Test sales tax and VAT compliance, including a multi-state nexus analysis.

- List pending audits and tax disputes, with reserves and exposure estimates.

- Reconcile tax basis to book basis on major assets so the acquirer understands depreciation and amortization implications.

7. Fraud Detection and Internal Controls

Fraud Detection and Internal Controls Review is roughly 10% of buy-side financial due diligence effort and covers SOX-style controls assessment, segregation-of-duties review, and bank reconciliation and vendor-master-file analysis. The deliverable is an internal-controls risk register flagging items that warrant escrow, indemnity coverage, or representation-and-warranty insurance carve-outs.

- Run a SOX-style internal controls review even when the target is private and not subject to SOX, focusing on financial-reporting controls.

- Test segregation of duties: the same person should not be able to initiate, approve, and record a transaction.

- Read recent management letters and recommendations from the target's auditor.

- Review whistleblower and ethics-hotline activity for the last three years.

- Sample 3 to 6 months of bank reconciliations to confirm completeness and accuracy.

- Run a vendor master file analysis to identify duplicate vendors, related-party vendors, and dormant vendors that suddenly received payments.

- Look for revenue recognition red flags: channel stuffing (Q4 revenue spikes followed by Q1 returns), bill-and-hold arrangements, and round-tripping with customers or suppliers.

- Watch for these common signals of asset misappropriation, financial-statement fraud, and corruption: complex business arrangements with no clear commercial purpose, end-of-quarter transactions that look out of pattern, recent changes in auditor, sudden growth that does not reconcile with industry trends, receivables growing faster than revenue, mid-period changes in accounting policy, and insider stock sales.

Buy-side financial due diligence

When we think of financial due diligence in an M&A transaction, we’re typically thinking about due diligence from the buy-side perspective.

Now, picture this: you're on the buy-side of an M&A transaction, preparing to acquire a growing e-commerce business. Everything looks good on paper. The revenue is strong, profits are steady, and they have a loyal customer base. But, during the financial due diligence process, you discover that the company’s growth has been fueled by heavy discounts and promotional pricing. Their EBITDA (earnings before interest, taxes, depreciation, and amortization.) looks inflated because they’ve been sacrificing margins for volume.

In this case, buy-side financial due diligence has saved you from overvaluing the company. You realize that after the acquisition, sustaining that growth without compromising profit margins will be a challenge.

Read more: How to Efficiently Conduct Buy-Side Due Diligence

Sell-side financial due diligence

Despite the tendency to think of financial due diligence as a buy-side practice, there is also a need for the sell-side in a transaction to conduct its own financial due diligence.

On the sell-side, imagine you're the CFO of a manufacturing company about to go up for sale. You’re preparing your financial statements for potential buyers. Through your own financial due diligence, you uncover some underutilized assets - an old warehouse that’s no longer in use and some outdated machinery. Highlighting these assets’ potential value in the sale boosts your company’s valuation, giving you a stronger negotiating position.

This proactive approach to financial due diligence not only attracts more interest from buyers but also ensures you’re not caught off guard during negotiations. This can also serve as a form of internal audit, helping to uncover issues that would otherwise have gone unchecked.

Read more: How to Efficiently Conduct Sell-Side Due Diligence

Understanding the importance of financial due diligence

Financial due diligence should be at the core of the due diligence process, because every other element of the business you’re analyzing will affect financial due diligence in some way.

Need investment in operations? That will affect financials.

The company is facing an upcoming legal dispute? That’s likely to cost you.

The target needs new management? Looks like you’re going to be paying redundancy soon.

Thus, whether the due diligence you’re undertaking is operational, legal or human resources, as in the cases above, or any other area of due diligence, it pays to keep costs in mind.

And while the checklist we provide below is strictly concerned with the explicit financial elements of the target company, every kind of due diligence is in some way financial.

The question, ‘what are the hidden costs here?’ is the essence of what the process is all about.

“Time pressure drives data quality problems. You can’t fix one without the other.”

- Matt Melsen

Shared at The Buyer-Led M&A™ Summit (watch the entire summit for free here)

Frequently Asked Questions

What is financial due diligence?

Financial due diligence is a detailed review of a company’s financial records before an investment, merger, or acquisition. It helps buyers confirm that the target’s financial performance, assets, and liabilities are accurate and reliable.

What is the main purpose of financial due diligence?

The purpose is to verify the financial health of a business. It helps investors assess whether the reported earnings, cash flow, and balance sheet figures reflect the company’s true value and risk profile.

How do you conduct financial due diligence?

Start by gathering financial statements for the past three to five years, review revenue streams, margins, and expenses, and check for consistency between financial reports and tax filings. Also analyze debt, working capital, and future cash flow projections.

What documents are needed for financial due diligence?

You’ll need audited financial statements, management accounts, tax returns, debt agreements, customer contracts, and forecasts. These records allow buyers to test accuracy and spot potential red flags.

Who conducts financial due diligence?

Due diligence is typically carried out by financial analysts, accountants, or advisory firms on behalf of investors, private equity funds, or corporate acquirers.

How long does financial due diligence take?

The process usually takes between two and six weeks, depending on company size, data availability, and deal complexity.

What is the difference between financial and legal due diligence?

Financial due diligence focuses on financial performance, accounting accuracy, and future projections. Legal due diligence examines ownership, contracts, and compliance issues.

Conducting financial due diligence with DealRoom

The DealRoom M&A platform is designed to simplify and streamline the financial due diligence process, offering built-in playbooks to help you get started quickly. These playbooks act as a step-by-step guide, ensuring that you cover all necessary aspects of due diligence efficiently.

With DealRoom, you have a centralized location to conduct all your due diligence and manage requests. You can invite all stakeholders—whether they are from your team, the target company, or external advisors—and assign granular permissions to control who sees what information. This ensures secure collaboration while giving you complete control over document access.

Each request within DealRoom allows for in-platform conversations, so you can handle all communications directly in the request thread. This eliminates the need for email back-and-forth, reducing time spent tracking conversations and ensuring nothing gets lost in translation.

Additionally, the platform has a virtual data room (VDR) where you can easily drag and drop relevant documents. Each document is indexed and stored in the VDR, ensuring everything is organized and accessible right when you need it. This integration between requests and document management is key to keeping your due diligence process smooth and efficient.

.png)

DealRoom offers DealRoom AI, a powerful feature that can analyze uploaded documents, answer specific questions, extract key information, and even generate summary reports. This feature helps reduce document review time by up to 80%, making the entire process faster and more accurate. Check out the interactive demo - Here!

Key Takeaways

Conducting financial due diligence is like peeling back the layers of an onion. Every new layer reveals something important, and sometimes what you find can completely change the deal. Whether you’re on the buy-side or sell-side, financial due diligence helps you make informed decisions, uncover hidden risks, and ultimately secure a better outcome.

Use DealRoom M&A Platform to streamline your financial due diligence process. Execute the process more efficiently and realize synergies faster.

.png)

.png)