Given that the three largest companies in the United States by market capitalization in 2021 are software firms, it should come as little surprise that some of the biggest deals of all time have concerned acquisitions in this space.

And this is nothing new: A cursory glance at historical acquisitions by software companies shows that IBM made its first acquisitions as far back as 1912 - Almost 110 years ago.

At DealRoom we help many tech companies organize their M&A process and below, we look at the biggest deals of all time in the tech space.

In putting together this list, we’ve looked at all of the transactions that involved companies not involved in hardware (i.e. chip manufacturers) that typically show up in technology deals.

The fact that so many of these deals go so far back suggests that it won’t be too long before we see new more recent deals added to the list.

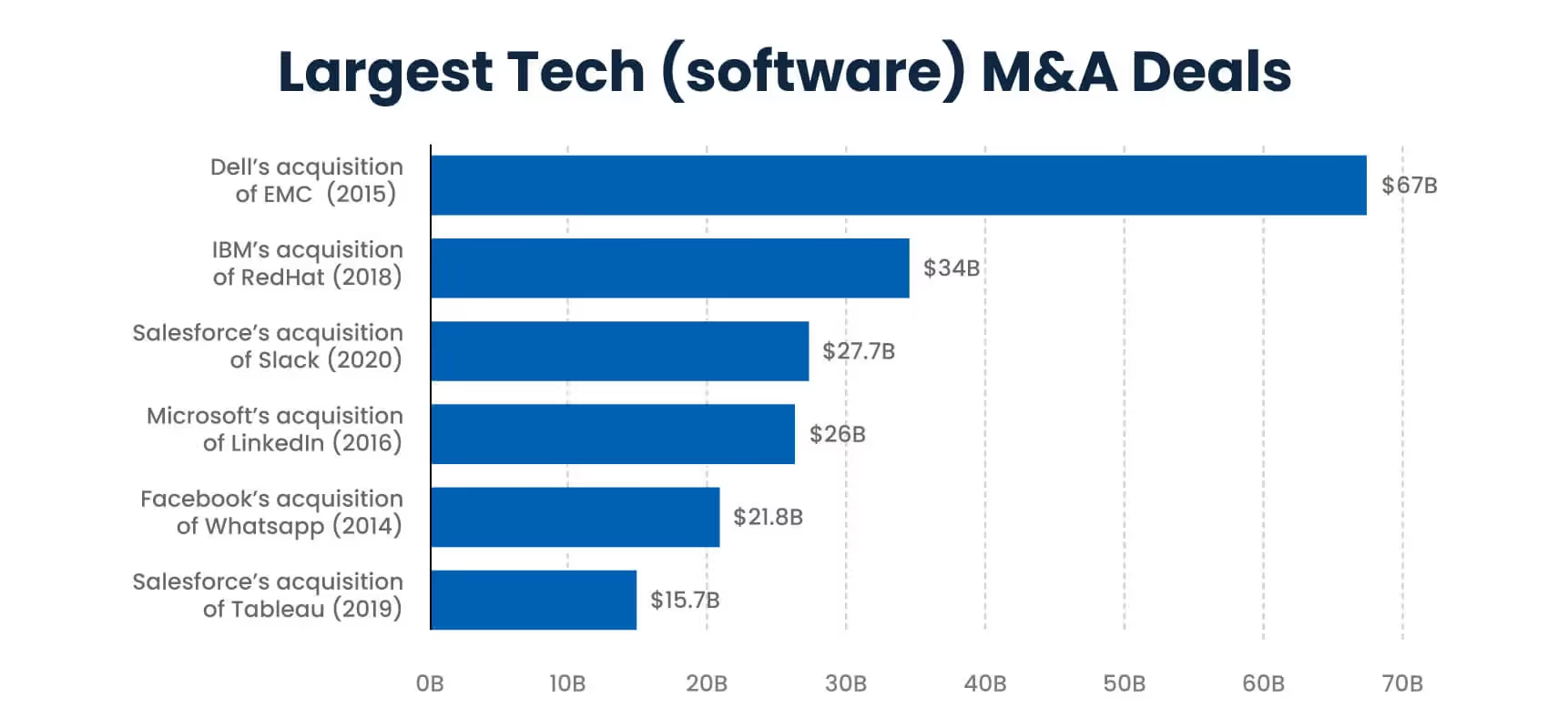

Largest tech (software) M&A deals

- Dell’s acquisition of EMC for $67B (2015)

- IBM’s acquisition of RedHat for $34B (2018)

- Salesforce’s acquisition of Slack for $27.7B (2020)

- Microsoft’s acquisition of LinkedIn for $26B (2016)

- Facebook’s acquisition of Whatsapp for $21.8B (2014)

- Salesforce’s acquisition of Tableau for $15.7B (2019)

So, let's dive into each deal specifically. Btw if you are looking for largest M&A deals of all time you can read about them here.

1. Dell’s acquisition of EMC for $67B (2015)

Dell’s acquisition of EMC, itself effectively a conglomerate of software companies, is not only the biggest software industry acquisition on record.

It is also one of the most controversial: It needed approval on the EMC side from the Chinese government, one of the company’s major shareholders AND Dell had to take on nearly $50 billion in debt to fund it.

However, as a private company, Dell was able to avoid much of the scrutiny that would have dogged other transactions of this scale.

Despite everything, the deal was a relative success: Dell went public again in 2018 - thought to be motivated by the need to fund this deal - and is now valued at nearly four times the value as it was at that time.

2. IBM’s acquisition of RedHat for $34B (2018)

IBM currently looks like a company in decline, and maybe one of the first signs of that was the acquisition of RedHat back in 2018.

An all-cash deal (rarely a good idea in transactions of this scale), the motivation behind the deal was to allow IBM to do more work on the cloud, one of the company’s four key growth drivers (the others being social, mobile, and analytics).

The deal would also allow IBM to acquire the RedHat human capital base - which industry onlookers say it was badly lacking. Jim Whitehurst, former CEO of RedHat, is now President at IBM and expected to become CEO: at some stage in the future.

Perhaps full judgement should be reserved on this deal until that occurs.

3. Salesforce’s acquisition of Slack for $27.7B (2020)

The acquisition of Slack by Salesforce at the end of 2020 marked the icing on the cake for a highly acquisitive period for Slack.

Slack as an application grew very rapidly due to it's modern design and incredible convenience for communication comparing with old messengers like Skype. Their awesome design team and their ui and ux design service brought flexibility and speed to product development process and helped the company get popularity.

The assumption, looking in from the outside, was that the dealmakers at Salesforce looked at their clients’ activity on their platform and decided that work was going to be changed forever by the impact of Covid-19, and began snapping up companies accordingly.

On closing the deal, Salesforce said that it was going to incorporate Slack’s communication software into every software’s offering, with its CEO going as far as to call it ‘a match made in heaven.’

A doubling of its share price in the intervening period (of a little under two years!) suggests that investors tended to agree.

4. Microsoft’s acquisition of LinkedIn for $26B (2016)

It would be generous to say that Microsoft’s history of acquisitions is ‘hit and miss.’

Just three years before the LinkedIn deal, former CEO Steve Ballmer pushed through a $7.9B deal for Nokia’s handset division.

The deal was a disaster.

The $26B deal for LinkedIn was an all-cash affair, making it another risky bet for Microsoft, who were aiming to use LinkedIn to improve its enterprise offering.

This time it got it right.

In 2021, Linkedin announced that it had passed $10B in revenue for the first time, tripling revenue in the five years since the acquisition closed.

It was also reported that LinkedIn’s user base had rocketed to 774 million users, making it by some distance the largest professional network in the world. It seems Microsoft’s record on M&A may have turned a corner.

5. Facebook’s acquisition of Whatsapp for $21.8B (2014)

The first downloadable mobile application ever was the long since forgotten HTML browser, Doris.

A pretty incongruous start for something now so ubiquitous.

Slightly more than a decade later and a mobile app became what was at the time, the most expensive transaction for a software application of all time.

Facebook paid $4B in cash, and the remainder in shares, which eventually made the deal worth a cool $21.8B. As some onlookers commented at the time, the deal was worth more than Iceland’s GDP.

As of the end of 2021, it looks as though the deal was another one of Facebook’s masterstrokes, with Whatsapp currently having close to 800 million users, and adding business accounts to the platform along the way.

6. Salesforce’s acquisition of Tableau for $15.7B (2019)

The fact that Salesforce has two acquisitions in the top six biggest software transactions of all time says everything about its ambitions.

Tableau is the world’s most used piece of software in the business intelligence (BI) and data visualization space.

Critically, Salesforce was able to make an all-share deal, which shareholders loved - Salesforce has been able to triple its stock price in less than two years, at a time when most companies on the stock market were being hammered.

The acquisition was also the latest signal that Salesforce was determined to build an end-to-end software ecosystem for enterprises of all kinds.

On closing the deal, Salesforce CEO Marc Benioff said:

“Tableau helps people see and understand data, and Salesforce helps people engage and understand customers. It's truly the best of both worlds for our customers.,"

Want to make software transactions happen?

DealRoom has been integral in hundreds of software deals closing over the past decade.

Talk to use today about how our lifecycle management software can help your software industry M&A transactions achieve success.

.png)

.png)

.avif)

.avif)

.avif)

.avif)