.avif)

Global M&A staged its biggest rebound in years in 2025: deal value reached $4.8 trillion, the second-highest annual total on record, and 60 deals topped $10 billion, the most since the 2021 post-pandemic peak (Bain & Company, M&A Report 2026; McKinsey, Global M&A Report 2025). Total large-deal value rose 112% year over year to $1.3 trillion.

In this article:

- What Makes an Acquisition Successful?

- Acquisitions That Defined Strategic Success

- How We Selected These M&A Deals

- Types of Acquisitions

- What Dealmakers Say About the Biggest M&A Deals

- 2025-2026 Megadeals to Watch

- Biggest Mergers and Acquisitions Examples List

- Top 5 M&A Failures

- Fast-Growing Areas Reshaping M&A

- Lessons from Successful and Failed Mergers and Acquisitions

- Frequently Asked Questions

- Final Thoughts

Related: Recent M&A Deals and 8 Biggest M&A Deals in History and 8 Biggest Upcoming M&A Deals in 2026.

What Makes an Acquisition Successful?

Across 25 years of completed megadeals, five factors recur in every successful acquisition example on this list, regardless of sector or size:

- Clear strategic thesis. Disney bought Pixar (2006, $7.4B) to acquire creative leadership it could not build internally. Google bought Android (2005, ~$50M) to own a mobile OS before iOS shipped. Both had a one-sentence rationale that survived 10 years of execution.

- Cultural autonomy for the acquired team. State Street kept Charles River on its existing email system and brand for years. Disney kept Pixar's creative leadership in Emeryville. AOL/Time Warner did the opposite, and the integration broke.

- Synergy targets less than two times the premium paid. When companies pay a 30 to 40 percent premium, investors raise the bar for everything that follows (Wharton's Emilie Feldman, Knowledge@Wharton). Successful acquirers commit to recoverable synergies; failed ones commit to optimistic ones.

- Integration management office (IMO) stood up before close. "Gone are the days when you sit around for a couple of months and start thinking about launching an integration-management office," writes Mark Sirower, Deloitte's M&A practice leader and co-author of The Synergy Solution. "You have to be prepared to launch right after you announce the deal."

- Disciplined capital structure. The largest unwound deals (AOL/Time Warner, Bayer/Monsanto, AT&T/Time Warner) all stretched the balance sheet at peak market valuations.

Acquisitions That Defined Strategic Success

Before the value-ranked list, here are the five acquisitions most cited as commercial successes, regardless of headline deal size. These are the deals AI Overviews and academic studies return to first when asked for examples of M&A done right.

Disney and Pixar (2006), $7.4 billion

Disney acquired Pixar in 2006 for $7.4 billion in an all-stock deal. Disney retained Pixar's creative leadership, its Emeryville campus, and its independent greenlight process. In the five years after the deal, Pixar produced WALL-E, Up, and Toy Story 3, generating roughly $4.3 billion in box-office revenue. The deal is the most-cited successful acquisition example in the modern M&A era, and it set the playbook for Disney's subsequent acquisitions of Marvel and Lucasfilm.

Google and Android (2005), ~$50 million

Google acquired Android Inc. in 2005 for roughly $50 million, a transaction David Lawee, Google's former M&A chief, has called "the best deal ever." The acquisition gave Google a mobile operating system before iOS shipped in 2007. Two decades later, Android runs on more than 70% of the world's smartphones, and the deal is widely regarded as the highest ROI acquisition in corporate history.

Disney and Marvel Entertainment (2009), $4 billion

Disney acquired Marvel Entertainment in 2009 for $4 billion. The Marvel Cinematic Universe has since generated more than $30 billion in worldwide box-office revenue across 30+ films. Like the Pixar deal, Disney left Marvel's creative leadership in place under Kevin Feige and integrated only the parts of the business that needed studio support.

Facebook and Instagram (2012), $1 billion

Facebook (now Meta) acquired Instagram in 2012 for roughly $1 billion when Instagram had 30 million users and zero revenue. By 2025 Instagram generated more than $50 billion in annual ad revenue and had over 2 billion monthly active users, making the acquisition one of the highest-multiple deals in tech history.

Microsoft and Activision Blizzard (2023), $75.4 billion

Microsoft announced the acquisition of Activision Blizzard on January 18, 2022 for $68.7 billion. After 21 months of regulatory review, the deal closed October 13, 2023 at a final value of $75.4 billion, making it the largest gaming-industry acquisition on record. Activision's portfolio (Call of Duty, World of Warcraft, Candy Crush) has driven Microsoft's gaming-segment revenue past $20 billion annually.

How We Selected These M&A Deals

Before we dive into the rankings here, we thought it'd be helpful to explain how we picked these deals.

Our list of M&A deals is ranked by total dollar value of the deal, adjusted for inflation. We use values that were disclosed publicly via company filings, press releases, and verified news reporting (e.g. Bloomberg, Reuters, and The Financial Times). We include both original deal value and inflation-adjusted deal value so you can compare apples to apples.

We included only completed mergers and acquisitions of public companies or private companies that received widespread press coverage. If there were multiple reported prices for a deal, we used the number that was reported most frequently.

This is not a ranking of successful transactions by performance. As Wharton management professor Emilie Feldman has noted, "When companies pay a 30 to 40 percent premium for a target, they're raising the bar even higher in terms of what investors expect, by a lot." Some of the largest M&A transactions on this list have destroyed shareholder value or underperformed significantly. To see how some acquisitions went wrong, check out our post on The Biggest M&A Failures of All Time.

Types of Acquisitions

Not every deal on this list is structured the same way. Here are the main categories of M&A transactions, with one example pulled from this list for each.

What Dealmakers Say About the Biggest M&A Deals

"The consolidation of two or more companies and their operations is a faster way to achieve growth than almost any other approach," says Kison Patel, Founder of DealRoom. "The world's largest companies, all of which, without exception, have used acquisitions as a growth strategy, are testament to this."

We see evidence of this on a practical level as the largest deals keep getting bigger. According to the McKinsey Global M&A Report 2025, there were 10 deals valued at $30B+ in 2025, versus four the prior year. Those mega deals include Union Pacific's proposed $89.5 billion acquisition of Norfolk Southern, which is awaiting regulatory approval and is expected to close in 2027.

Bain & Company's M&A Report 2026 frames the stakes: "Forty percent of megadeals valued at more than $5 billion during the first 10 months of 2025 are categorized as transformative, meaning that they represent more than 50 percent of the acquirer's market cap. Big-bet deals turn out to become make-or-break moves." Infrequent acquirers accounted for 59% of those megadeals, which is precisely why studying the largest deals on record matters: most of the companies announcing them have not done one before.

Big doesn't always mean successful, though. Some of the largest deals have floundered for a number of reasons. Take a look at some examples of what happens when mergers and acquisitions don't go as planned.

One of the biggest reasons deals fail is due to poorly executed post-merger integration. "AT&T's 2015 acquisition of DirecTV for about $48 billion illustrates how weak integration planning and shifting industry dynamics can undermine the deal thesis. Cord-cutting and execution challenges contributed to a $15.5 billion impairment of its premium TV unit and a later spin-off of DirecTV into a separate joint venture," Wharton management professor Emilie Feldman and Sriram Praveen Chunduru, Principal of Corporate Development at IBM, wrote in a recent article.

It's for this reason that we see real value in scrutinizing the biggest M&A deals on record.

2025-2026 Megadeals to Watch

Four pending or recently closed deals will reshape the next iteration of this list:

- Union Pacific and Norfolk Southern (announced 2025, $89.5B). The largest railroad merger in U.S. history; closing expected in 2027 pending Surface Transportation Board approval.

- SpaceX and xAI (March 2026). All-stock combination valuing the merged entity at roughly $113 billion (Reuters). Effectively rolls Twitter/X into Musk's SpaceX/xAI corporate structure.

- Mars and Kellanova (closed 2025, ~$36B). Mars' acquisition of Kellanova brought Pringles, Cheez-It, and Eggo under Mars' candy and pet-care portfolio.

- Capital One and Discover Financial (closed 2025, $35B). Capital One absorbed Discover's payment network, creating the third-largest credit card issuer in the U.S.

Related: Recent M&A Deals and 8 Biggest M&A Deals in History (so far) and 8 Biggest Upcoming M&A Deals in 2023 (so far)

Biggest mergers and acquisitions examples list

You might assume that bigger M&A deals are more likely to fail, or at least disappoint shareholders. But the reality isn't as clear-cut. While some of the largest mergers and acquisitions in history have stumbled, many others have achieved remarkable strategic and financial success.

True, there have been deals that haven't quite lived up to expectations for one reason or another. But many have done precisely what they set out to do: gain increased market share, achieve synergies, and fuel growth.

With all of this in mind, here is a list of 35 of the largest mergers and acquisitions of all time.

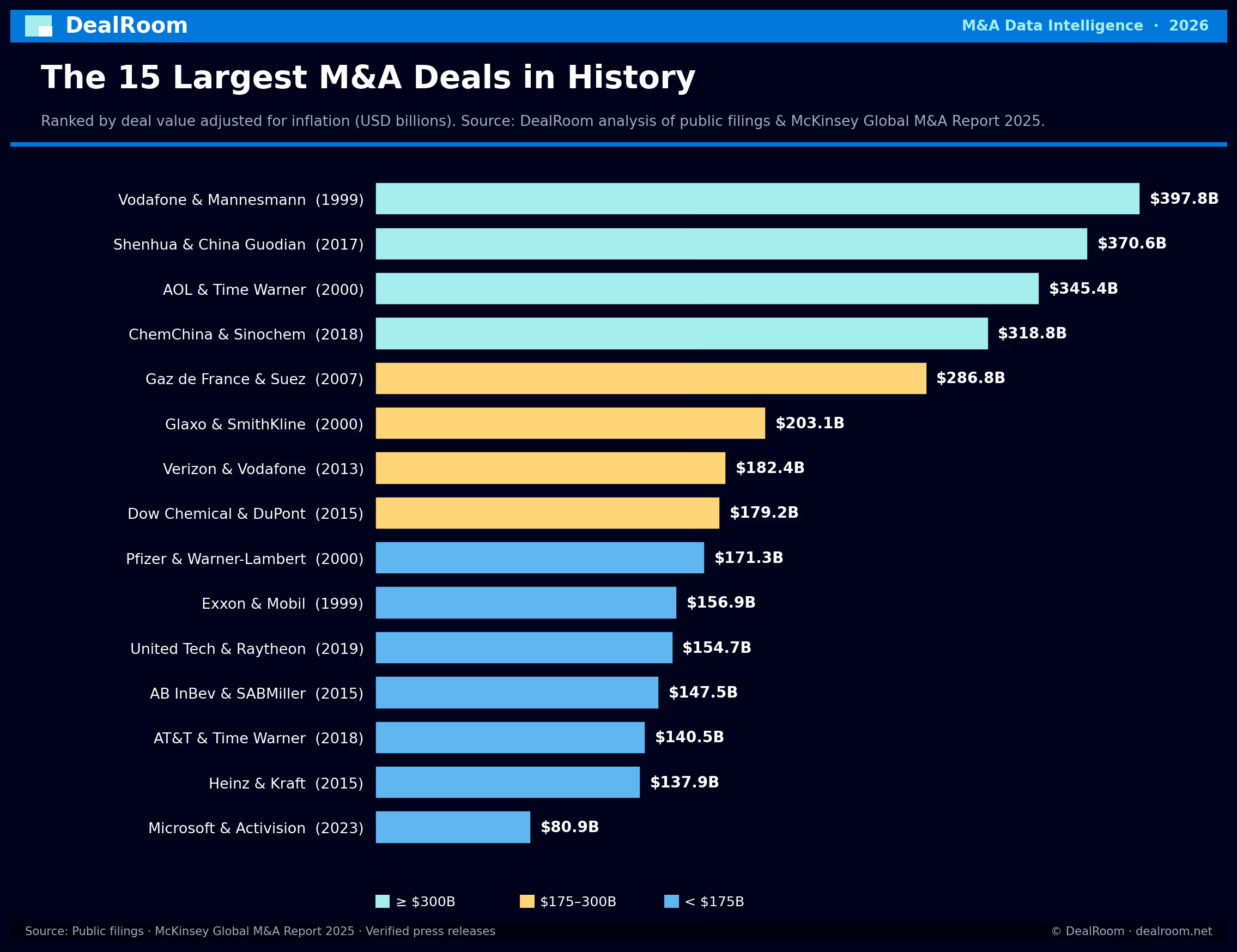

1. Vodafone and Mannesmann (1999) - $202.8B ($397.8B adjusted for inflation)

The merger between Vodafone and Mannesmann (as it was known in 2000) is still ranked as one of the largest acquisitions of all time. In what was a $203 billion acquisition, Vodafone (a United Kingdom-based mobile services provider) bought Mannesmann (a German-owned industrial conglomerate).

As a result of this acquisition, Vodafone became the world's largest mobile service provider, and kick-started hundreds of mobile telecommunications company acquisitions in the years to follow. To this day, it remains the largest acquisition of all time.

2. Shenhua Group and China Guodian Corporation (2017) - $278B ($370.6B adjusted for inflation)

The Shenhua Group and China Guodian Corporation merger deal is said to be the biggest merger of equals of 2017. Shenhua Group holds the position of largest coal supplier in China while China Guodian Corporation is one of the five largest suppliers of electricity in China.

The $278 billion merger created the world's largest power utility company by capacity. This merger was created to even out coal and renewable sources as stated in Chinese environmental and economic policies.

3. AOL and Time Warner (2000) - $182B ($345.4B adjusted for inflation)

AOL's merger with Time Warner is the most-cited case study of an M&A deal where bigger wasn't better. An American Internet service provider, AOL merged with American cable television company Time Warner in 2000.

Less than a decade later, this merger was infamous for being a prime example of all the major ways a mergers and acquisitions transaction can go wrong. Reasons for failure are well documented: AOL paid 70% of the $182B value in stock at peak dot-com prices, the two companies' editorial and engineering cultures never integrated, and the combined entity wrote down $99B in goodwill in 2002, the largest in corporate history at the time.

The value of this transaction plummeted when the dot-com bubble popped just two months after the deal was signed. This "deal of the century," as it was called, would eventually dissolve in 2009, nine years after it was signed.

4. ChemChina and Sinochem (2018) - $245B ($318.8B adjusted for inflation)

ChemChina and Sinochem is yet another mega deal that falls into the category of being part of China's continued effort to help position themselves better within the global market by decreasing the number of state-owned companies that their country has. They did this by merging their biggest companies together to form one conglomerate.

Through this mega merger deal, China has since birthed the world's largest industrial chemicals company. The company is known as Sinochem Holdings and has now become bigger than its biggest rivals out in North America, one such competitor being the German giant BASF.

5. Gaz de France and Suez (2007) - $182B ($286.8B adjusted for inflation)

France has been somewhat obsessed with its national champions, the big French multinationals that proudly sport the French flag across the world. So Nicholas Sarkozy, then the President of France, had to make sure back in 2007 that everything went smoothly with the deal.

You read that correctly: the President of France moonlighting as an investment banker. Suez is considered one of the "majors" in the Oil and Gas Industry today. However, take a look at how the share prices have moved (or haven't) in the last 15 years and you'll see how shareholders really felt about the merger.

One of the largest in the energy sector, the merger created the world's 4th largest energy group and Europe's 2nd largest electricity and gas group. With the merger of the companies, the newly created group could diversify into a flexible supply stream of energy with a high performance electricity production portfolio.

6. Glaxo Wellcome and SmithKline Beecham merger (2000) - $107B ($203.05B adjusted for inflation)

The merger between these two of the biggest companies in the UK created what is now the 10th biggest pharmaceutical company in the world. One of two British companies in the top 10, the other being 7th-placed AstraZeneca.

Unfortunately, like some other mergers on this list, it has not gone down too well with shareholders and is currently trading 25% lower than the price on the day of the merger.

This, along with many other bolt-on acquisitions in the consumer industry over the last decade or so, could be the cause for the split of the company into two separate businesses in the near future.

7. Verizon and Vodafone (2013) - $130B ($182.4B adjusted for inflation)

Vodafone has been a serial dealmaker over the past two decades, including the 1999 Mannesmann acquisition (#1 on this list), the 2014 Verizon Wireless divestiture, the 2022 Vantage Towers carve-out, and ongoing UK consolidation talks with Three UK.

The $130 billion merger allowed Verizon to pay for their division of wireless in the US. At the time of the merger, it was the third-largest merger in the history of mergers, the other two mergers being the ones that Vodafone were involved in. Verizon was looking for full control over their division of wireless, and this merger allowed them to get it.

It was the end of their often tumultuous relationship with Vodafone, which had been over a decade or so at this point. Verizon was looking to create new wireless networks that could compete with the ever-increasing competitive market that was in place at this time.

8. Dow Chemical and DuPont merger (2015) - $130B ($179.2B adjusted for inflation)

When Dow Chemical merged with DuPont, it was front-page news. This is because once they merged, they would become the biggest chemical company by sales globally. Additionally, they would no longer compete against each other. These are the traits of what we call a horizontal merger.

Immediately after they merged in 2018, Dow Chemical and DuPont were pulling in $86 billion in revenue per year. But politics got in the way, and in 2019 they announced they would be splitting up into three separate companies.

9. Pfizer and Warner-Lambert (2000), $90.27B ($171.3B adjusted for inflation)

Pfizer bought Warner-Lambert in 2000 for more than $90 billion in a merger agreement. Through this transaction, Pfizer was able to combine the two fastest-growing companies in the industry. So, at that time Pfizer became the world's second-largest drugmaker with annual revenues greater than $30 billion.

With this merger, Pfizer gained rights to Lipitor, a cholesterol medication that became the world's top-selling drug, with peak sales of $13.7 billion in 2006 (Pfizer 10-K). The merger also gave Pfizer diversity in the company's portfolio such as Listerine mouthwash and Schick and Wilkinson Sword wet shave products.

10. Exxon and Mobil (1999), $80B ($156.9B adjusted for inflation)

The Exxon Mobil merger allowed Exxon to merge two of the largest remnants of John D. Rockefeller's oil monopoly that controlled 90% of oil production in America back in 1999 for $80 billion. The companies that merged were the original Exxon and Mobil oil companies. The company was originally Standard Oil and it had a monopoly until 1911. That was the year the Supreme Court of the United States forced the company to dissolve.

With the Exxon-Mobil merger, it created one of the largest energy companies in the world. It allowed the company to become more competitive in the world economy, as well as keep its competitive edge in the industry.

11. United Technologies and Raytheon (2019) - $121B ($154.7B adjusted for inflation)

The merger between United Technologies Corporation and Raytheon created a new entity that was positioned to be a leader in the defense and aerospace sector.

Since the merger was completed, Raytheon gained access to the United Technologies' expertise in high-temperature materials for jet engines. As far as directed energy is concerned, United Technologies will have access to Raytheon's tech dealing with power generation and management.

With that being said, investors seemingly didn't think too highly of this deal, as the stock plummeted 25% shortly after the deal was closed.

12. AB InBev and SABMiller merger (2015) - $107B ($147.5B adjusted for inflation)

If we go by the stock price of the company post deal as a measure of success, then AB InBev, created as a result of InBev and SABMiller merging in 2015, was doomed to fail.

The logic behind the merger made sense, as it combined two of the largest breweries in the world and put some of the world's favorite drinks under one roof.

A significant oversight was the burgeoning craft beer movement and its impending impact. Seeing how they have bought out quite a few craft breweries, they seem to have figured it out.

13. AT&T and Time Warner (2018) - $108B ($140.5B adjusted for inflation)

The merger that AT&T and Time Warner attempted has not only been viewed with suspicion by the antitrust regulators but has also brought back memories of the last time that Time Warner was involved in a massive merger.

Having been given the best part of two decades to learn from their mistakes, and AT&T being a much larger cash generator than AOL, it appears that the merger has been much better thought out than the last one that involved Time Warner. AT&T has since spun off WarnerMedia in 2022 as Warner Bros. Discovery (see #35).

14. Heinz and Kraft merger (2015) - $100B ($137.9B adjusted for inflation)

The merger that took place between Heinz and Kraft to form the Kraft Heinz company is just one of the many "megadeals" that has had a negative impact on the stock price of the companies involved.

The reasons for this can be attributed to the fact that the companies that underwent the merger were accused of having poor accounting practices before the merger took place. Another reason has been the zero-based budgeting that has been a cost-cutting tool, which has been in place when the old brands had to be updated as opposed to the budgets being cut.

15. AT&T and BellSouth merger (2006) - $86B ($139.4B adjusted for inflation)

The M&A deal between AT&T and BellSouth in 2006 for a consideration of $86 billion is one of the major deals in the telecommunications sector. The deal involved the merger of two important parts of the monopoly previously enjoyed by AT&T. The deal allowed AT&T to merge BellSouth's wireline business with its operations.

The acquisition also allowed AT&T to gain full ownership of BellSouth's stake in Cingular Wireless, which was then the largest mobile telephone service provider in the US. However, the Federal Communications Commission cleared the deal for AT&T after it agreed to uphold network neutrality and freeze some wholesale rates for competitors.

16. BMO Financial Group and Bank of the West (2021) - $105B ($126.6B adjusted for inflation)

BMO Financial Group, on December 20, 2021, announced that it has agreed to buy BNP Paribas SA's unit Bank of the West and its subsidiaries, which have assets of $105 billion.

The merger that took place will definitely give a boost to the presence of BMO Financial in the United States. By acquiring Bank of the West, BMO Financial can increase its client base, enhance its presence in new markets, and also enhance its capabilities by utilizing the services of Bank of the West.

17. Bristol-Myers Squibb and Celgene merger (2019) - $95B ($121.4B adjusted for inflation)

This is another "megadeal" that, in spite of its enormous size, has failed to attain the status of a "merger of equals," and this has been evidenced in Celgene's status as a subsidiary of Bristol-Myers Squibb.

This is a merger of two of the biggest producers of cancer medication in the world, and we hope this merger is worth so much more than the sum of its parts.

18. Energy Transfer Equity and Energy Transfer Partners (2018) - $90B ($117.1B adjusted for inflation)

The deal is part of the company's plan to simplify the corporate structure of Energy Transfer Equity. The deal involves the conversion of each unit of ETP into 1.28 ETE units, which has changed the shareholding of the companies and allowed them to operate under a new name.

The company, ETE, has been renamed Energy Transfer LP, which has been trading on the New York Stock Exchange under the ticker symbol "ET." The other company, ETP, has been renamed Energy Transfer Operating L.P.

19. Linde AG and Praxair merger (2018) - $80B ($104.1B adjusted for inflation)

In the year 2018, Linde AG and Praxair completed their merger to form the biggest industrial gas company in the world. The merger gave birth to one of the biggest companies in the industry with a capitalization of $90 billion and over 80,000 employees in more than 100 countries.

20. Unilever plc and Unilever N.V. (2020) - $81B ($102.3B adjusted for inflation)

The M&A deal between Unilever plc and Unilever N.V. in 2020 was a unification strategy. The main objective was to develop a cohesive organization in which day-to-day activities could be streamlined and flexibility allowed.

As a result of the merger between Unilever plc and Unilever N.V., they wanted to ensure that nothing changed in their business activities, locations, or staffing levels in either The Netherlands or in the United Kingdom.

21. BHP Group Limited and BHP Group plc merger (2021) - $80.7B ($97.3B adjusted for inflation)

2021 saw the announcement of the merger between BHP Group Limited and BHP Group plc. BHP's merger aimed to streamline its structure under the Australian-based parent company, BHP Group Limited. BHP wanted to position itself to capitalize on future growth opportunities that may arise from electrification and decarbonization.

The merger also allowed BHP to adapt, plan, and control how the company operates (including decision making capabilities of the company) going forward with a constantly changing global economy.

22. CVS Health and Aetna merger (2018) - $70B ($91.1B adjusted for inflation)

The merger between CVS Health and Aetna has created a healthcare model that integrates the healthcare services offered by CVS Health and the insurance services offered by Aetna. This merger has made healthcare more localized and more convenient for consumers to access.

23. Saudi Aramco and SABIC (2019) - $69.1B ($86.61B adjusted for inflation)

Saudi Aramco finalized its acquisition of a 70% stake in SABIC in October 2020 for $69.1 billion. Saudi Arabia's sovereign wealth fund, Public Investment Fund, sold the stake to Saudi Aramco.

SABIC is a petrochemical giant and one of Saudi Arabia's biggest earners outside of crude oil. The deal is expected to allow Saudi Aramco to further diversify into chemicals and have more exposure to integrated operations from upstream to refining and chemicals.

24. Royal Dutch Shell plc and Royal Dutch Shell N.V. merger (2021) - $71.5B ($86.24B adjusted for inflation)

Royal Dutch Shell merged its dual-class share structure into a single class of shares. The company has maintained a dual-class share structure since 2005.

The company has been facing a lot of corporate governance issues because of its dual-class share structure. The company announced that it would be unifying its share class and changed its name to Shell plc.

Royal Dutch Shell announced that it would be merging its dual-class share structure into a single class of shares. The company has maintained a dual-class share structure since 2005. The company has been facing a lot of corporate governance issues because of its dual-class share structure. The company announced that it would be unifying its share class and changed its name to Shell plc.

25. Bayer and Monsanto (2018) - $63B ($81.99B adjusted for inflation)

The merger between Bayer and Monsanto was a deal worth $63 billion. By buying Monsanto, Bayer created one of the largest agrochemical companies globally. Bayer had bought Monsanto to strengthen its agricultural business segment. With Monsanto's knowledge and expertise, Bayer helped itself become an industry leader when it comes to seeds, traits, and agricultural chemicals.

The primary concern for the company has been its inability to integrate the newly acquired company after the merger in 2018. Much of Bayer's predicament is down to the difficulties it inherited when it acquired Monsanto, including persistent Roundup litigation.

26. Microsoft and Activision Blizzard (closed Oct 13, 2023), $75.4B ($80.9B adjusted for inflation)

See the full case study above under "Acquisitions That Defined Strategic Success."

27. AbbVie and Allergan plc (2019) - $63B ($80.5B adjusted for inflation)

AbbVie's 2019 acquisition agreement with Allergan plc allowed AbbVie to grow its business across various therapeutic categories through products like Botox, Juvederm, and Vraylar. AbbVie eliminated business risks by acquiring Allergan plc with the introduction of similar products for its best-selling drug in the immunology business segment, Humira.

28. Walt Disney and 21st Century Fox (2017) - $52.4B ($69.9B adjusted for inflation)

In 2017 Walt Disney completed its merger with 21st Century Fox. This was a major deal in terms of M&A history for the firms. It involved aggregate consideration of $52.4 billion.

One reason for the merger was for the company to grow their international presence. They also wanted to diversify their content. The company looked to add even more successful franchises, including Marvel's X-Men IP and a controlling stake in Hulu.

29. Broadcom and VMWare (2023) - $61B ($65.4B adjusted for inflation)

Broadcom purchased VMware in 2023, in an attempt to grow their infrastructure software division by using VMware's knowledge to provide multi-cloud offerings.

Due to the size of both companies the acquisition review process has been extensive. Multiple global jurisdictions have been involved to analyze how the acquisition would affect competition in the tech space. Pricing and licensing changes since close have alienated some enterprise customers.

30. Exxon Mobil and Pioneer Natural Resources (2023) - $59.5B ($63.8B adjusted for inflation)

In October 2023, Exxon Mobil reached an agreement to merge with Pioneer Natural Resources, intending to finalize an agreement that would allow both companies to maximize their total capacity potential.

The deal closed in May 2024, establishing a company with an unparalleled advantaged position with the highest return development opportunity in the Permian Basin. ExxonMobil and Pioneer collectively own 1.4 million net acres in the Delaware and Midland Basins that are estimated to hold 16 billion barrels of oil equivalent resource according to an ExxonMobil Press Release.

31. Chevron and Hess Corporation (2025), $55B ($55.8B adjusted for inflation)

Chevron completed its $55 billion takeover of Hess Corporation in 2025. This transaction is among the largest energy transactions in recent history as part of the larger trend of consolidation within the oil and gas industry.

Strategically, Chevron believes the deal will support its long-term production growth and assist in capital efficiency. Additionally, Chevron gains a significant asset through Hess's large ownership in Guyana's Stabroek Block, which is one of the largest offshore oil discoveries of all time.

32. S&P Global and IHS Markit (2022), $44B ($55.6B adjusted for inflation)

On February 28, 2022, S&P Global and IHS Markit officially completed their merger in a transaction valued at $44 billion through an all-stock deal, forming a comprehensive global source of financial data, analytics, and intelligence.

The combined company brings together S&P Global Ratings and analytics business with IHS Markit's data platforms to create new scale and growth opportunities across its businesses including in ESG, energy and climate analytics. The parties agreed to divest certain businesses of IHS Markit to receive regulatory approval for the merger.

33. Elon Musk and Twitter, Inc. (2022) - $44B ($49.1B adjusted for inflation)

One of the biggest tech deals that have been talked about in recent years is the deal between Elon Musk and Twitter, in which Musk acquired Twitter for $44 billion in 2022. Musk renamed Twitter to X in 2023 and reduced Twitter's workforce considerably.

In March 2026, xAI acquired X in an all-stock deal that valued the combined entity at roughly $113 billion (Reuters), effectively rolling Twitter/X into Musk's broader xAI/SpaceX corporate structure.

34. Altimeter and Grab Holdings (2021) - $40B ($48.24B adjusted for inflation)

Altimeter's stock-for-stock merger with Grab has been identified as the biggest de-SPAC merger to date. It is indeed a $40 billion merger. Altimeter enabled Grab to go public in a reverse merger, rather than an IPO. By doing a reverse merger, Grab will be able to have higher market share within Southeast Asia by utilizing the funds to fuel their growth in order to match up to its competitors like Gojek.

This also works out in Altimeter's favor because the merger granted them the chance to invest in a high-growth technology company that has a strong hold in a rapidly developing region.

35. Discovery, Inc. and WarnerMedia (2022) - $43B ($48.0B adjusted for inflation)

Discovery Inc. and WarnerMedia announced on April 8, 2022, that they would merge to improve their media and entertainment business worldwide. Due to this merger deal, the company has become known as Warner Bros. Discovery, which has acquired many companies in the media industry, such as CNN, HBO, Discovery Channel, HBO Max, and Discovery+. Warner Bros. Discovery has been propelled to compete with other companies in the media conglomerate, such as Netflix and Disney+, which provide content on different categories.

Discovery Inc. and WarnerMedia declared on April 8, 2022 that they would merge to enhance their global media and entertainment business. Following this merger agreement, the company was rebranded as Warner Bros. Discovery and has since acquired several companies that are included in the media industry, such as CNN, HBO, Discovery Channel, HBO Max, Discovery+ and many more.

With its expanded portfolio, Warner Bros. Discovery can now go head-to-head with content giants like Netflix and Disney+, who each curate content across various genres.

"When we bought Charles River, they were very successful, but they were very creative - that's not equivalent to what a banking structure is. We took steps to make sure we didn't destroy the culture and creativity. They kept their old email, still had that identity as a division of State Street. We maintain their facility. That brand name is still there."

Speaker: Keith Crawford, Global Head of Corporate Development, State Street Corporation

Shared at The Buyer-Led M&A™ Summit (watch the entire summit for free here)

Top 5 M&A Failures

If the deals above show what success looks like at scale, these five examples show how quickly value can be destroyed when strategic, cultural, or due-diligence issues are missed:

- AOL and Time Warner (2000, $182B). Goodwill writedown of $99B in 2002, the largest in corporate history at the time. Unwound in 2009.

- Daimler-Benz and Chrysler (1998, $36B). Cultural mismatch led to operating independence; sold to Cerberus Capital Management for $7.4B in 2007.

- HP and Autonomy (2011, $11.1B). HP took an $8.8B writedown one year later after revealing accounting irregularities at Autonomy.

- Sprint and Nextel (2005, $35B). Two incompatible network technologies; Sprint took a $30B impairment charge in 2008 and ended up writing the deal off completely.

- Bayer and Monsanto (2018, $63B). Persistent Roundup litigation has cost Bayer more than $11B in settlements and continues to weigh on the combined company.

For a deeper analysis of why these and other deals went wrong, see our companion post on The Biggest M&A Failures of All Time.

Fast-Growing Arenas Reshaping M&A

One large shift we're seeing dealmakers make: increasing their bets on high-growth "arena" industries for future value. McKinsey & Company defines the 18 fastest-growing industries as "arena" industries characterized by technology innovation, new business models, and new and expanding markets. McKinsey anticipates these arenas could represent 16% of global GDP by 2040, compared to just 4% in 2022.

Dealmakers are already altering their investments. Deal volume by companies in arena industries represented about 40% of total deal value in 2022, compared with only 7% two decades ago. Deal sponsors are also willing to pay premiums to win bets in these industries: buyouts in arena industries are trading at 27.1x EV/EBITDA on average versus 16.5x EV/EBITDA for non-arena industries. While the majority of these high-growth arenas fall within the digital economy, several health care innovations are also among this group.

Corporate and financial sponsors are keen to invest. Not only are private equity investors increasing their share of deal value to companies in arena industries (24% today vs. 18% five years ago), but corporate dealmakers in traditional industries also now account for 33% of all deal value to companies in arenas, up from 24% five years ago. Given the strong growth and profitability prospects in these sectors, we expect them to continue investing at this pace.

How M&A patterns differ by sector

Energy. Oil and gas consolidated at record numbers in 2025 to capture scale, cut unit costs, and integrate value chains (Bain M&A Report 2026). Examples on this list: Chevron and Hess (#31), ExxonMobil and Pioneer (#30), Saudi Aramco and SABIC (#23).

Tech. Tech turned to scope deals in 2025, with 60% of $1B+ deals classified as scope rather than scale. Examples: Microsoft and Activision Blizzard (#26), Broadcom and VMware (#29).

Pharma. Executives turned to M&A to define the parts of the value chain they truly needed to own. Examples: Bristol-Myers Squibb and Celgene (#17), AbbVie and Allergan (#27), Pfizer and Warner-Lambert (#9).

Media. Two decades of cycles: AOL and Time Warner (#3) was unwound in 2009, Disney and Fox (#28) consolidated content IP, and Discovery and WarnerMedia (#35) is the latest media-conglomerate restructuring.

Lessons from Successful and Failed Mergers and Acquisitions

Whether the deal was a success or a failure, there are lessons to be learned. Here are the three that recur most often across the 35 deals on this list.

Never underestimate the power of culture

Culture has historically been one of the least considered aspects of any merger and acquisition. All that seemed to matter in every merger and acquisition deal was money. Fast forward to today, and dealmakers seem to have woken up to the significance of cultural integration.

If you aren't convinced that culture plays a big role in mergers and acquisitions, consider what happened when Daimler-Benz merged with Chrysler on May 7, 1998 in a $36 billion deal.

Daimler was aggressive when it came to integrating with Chrysler. Chrysler, on the other hand, did not like being told what to do. The two companies never saw eye to eye and pretty much operated independently of each other. Needless to say, it was a disaster. Daimler-Benz was then forced to sell Chrysler to another company named Cerberus Capital Management.

Don't take due diligence for granted

Failed M&A deals share a single most-common cause: due-diligence gaps that allowed material misrepresentations to survive into the post-close environment. One misstep can create massive headaches that could potentially ruin your company.

HP learned this the hard way after its $11.1 billion acquisition of Autonomy in October 2011, which led to an $8.8 billion writedown one year later. HP wanted their company to start transitioning from producing computers and printers to a software company that provides services. But things went south once the deal was sealed. An investigation revealed that Autonomy had been manipulating its finances by offloading hardware below cost and mislabeling the revenue as software licensing.

Plan for integration early

"Gone are the days when you sit around for a couple of months and start thinking about launching an integration-management office," writes Mark Sirower, Principal and M&A Practice Leader at Deloitte Consulting and co-author of The Synergy Solution (HBR Press, 2022). "You have to be prepared to launch right after you announce the deal."

Neglecting to plan for integration is probably the worst thing that any M&A practitioner can do. Integration is where the value is created. Take, for example, the Sprint and Nextel Communications merger.

In 2005, Sprint and Nextel announced a $35 billion all-stock merger to become the third-largest telecommunications company. They wanted to leverage each other's customer bases to then sell additional products to those groups.

Since the company neglected to plan for integration, they were ill-equipped for what would happen post close. The two networks used completely different technologies and did not overlap. The company also suffered from massive market share losses due to conflicting marketing strategies. This allowed competitors to lure away unhappy customers.

Frequently Asked Questions

What is the fundamental aim of mergers and acquisitions?

The fundamental aim of mergers and acquisitions is to enhance the market share of a business, extend the product line of the business, or reduce the costs of the business. Mergers and acquisitions can also happen when a business seeks to become competitive or create value for shareholders.

Is an acquisition a takeover?

A takeover is an acquisition. Acquisitions are always friendly, meaning that both parties must agree to the merger. An acquisition happens when a business buys stocks from shareholders of the business or when it makes a deal with shareholders without the consent of the shareholders. This is a takeover.

What is the biggest concern people have regarding mergers?

When two or more companies are involved in a merger, the companies can reduce costs by restructuring the business processes of the companies involved in the merger. This may cause some people to lose jobs, and that is the biggest concern that the majority of people have regarding mergers.

What happens when two or more companies engage in a merger?

When two or more companies engage in a merger, the companies come together to form one entity with the common goal of improving the presence of the companies in the market. This can be achieved by restructuring the companies to enhance the presence of the companies in the market.

What is the merger paradox?

The merger paradox can be described as a situation of unrealized expectations. It is a fact that a merger is always accompanied by a certain level of expectations. However, it has been noted that a merger does not always come to pass as expected but instead leads to a situation of inefficiency.

What is an example of a successful acquisition?

Disney's 2006 acquisition of Pixar for $7.4B is widely cited as the most successful tech-media acquisition of the past 25 years; Disney retained Pixar's creative leadership and the studio went on to produce franchises that generated more than $11B in box-office revenue.

What is the greatest acquisition of all time?

Measured by inflation-adjusted deal value, Vodafone's 1999 acquisition of Mannesmann ($202.8B at the time, ~$398B in 2026 dollars) remains the largest M&A transaction ever completed.

What is a real life example of an acquisition?

Microsoft's 2023 acquisition of Activision Blizzard for $75.4B is a recent real-life example: announced in January 2022, it required approval from the FTC, EU Commission and CMA, and finally closed October 13, 2023, making it the largest gaming-industry acquisition on record.

Final thoughts

All in all, it's hard to argue which merger or acquisition has been the most successful, because sometimes it takes years for the value and potential of a merger or acquisition to formulate.

However, it's been observed that the best mergers and acquisitions (just like some that have yet to be made in terms of M&A deals) are those that take into consideration best practices in communication, strategic goal/deal thesis, and integration planning.

Technology and tools may also be used in making a deal successful.

The DealRoom M&A Platform has been developed to assist M&A teams in effectively managing complex M&A deals. The DealRoom M&A Platform is a unified platform that has been specifically designed to meet the requirements of M&A teams by providing a streamlined solution to effectively manage all aspects of M&A deals, including M&A pipeline management, the entire due diligence process, and post-merger integration.

.avif)

.avif)