Revenue-based financing (RBF) is set to soar to unprecedented levels. One such industry report, by Allied Market Research, suggests that the global revenue-based financing market size can expect phenomenal growth of 62.8% between 2020 and 2028, bringing the industry from $901 million in 2019 to $42.3 billion in 2028.

In this article, DealRoom takes a closer look at revenue-based financing.

What is Revenue-Based Financing?

Revenue-based financing, also known as revenue sharing or royalty-based financing, is a method of raising capital, typically used by fast growing businesses. The investors that provide the financing are repaid with a percentage of the company’s revenues.

How does Revenue-Based Financing Work?

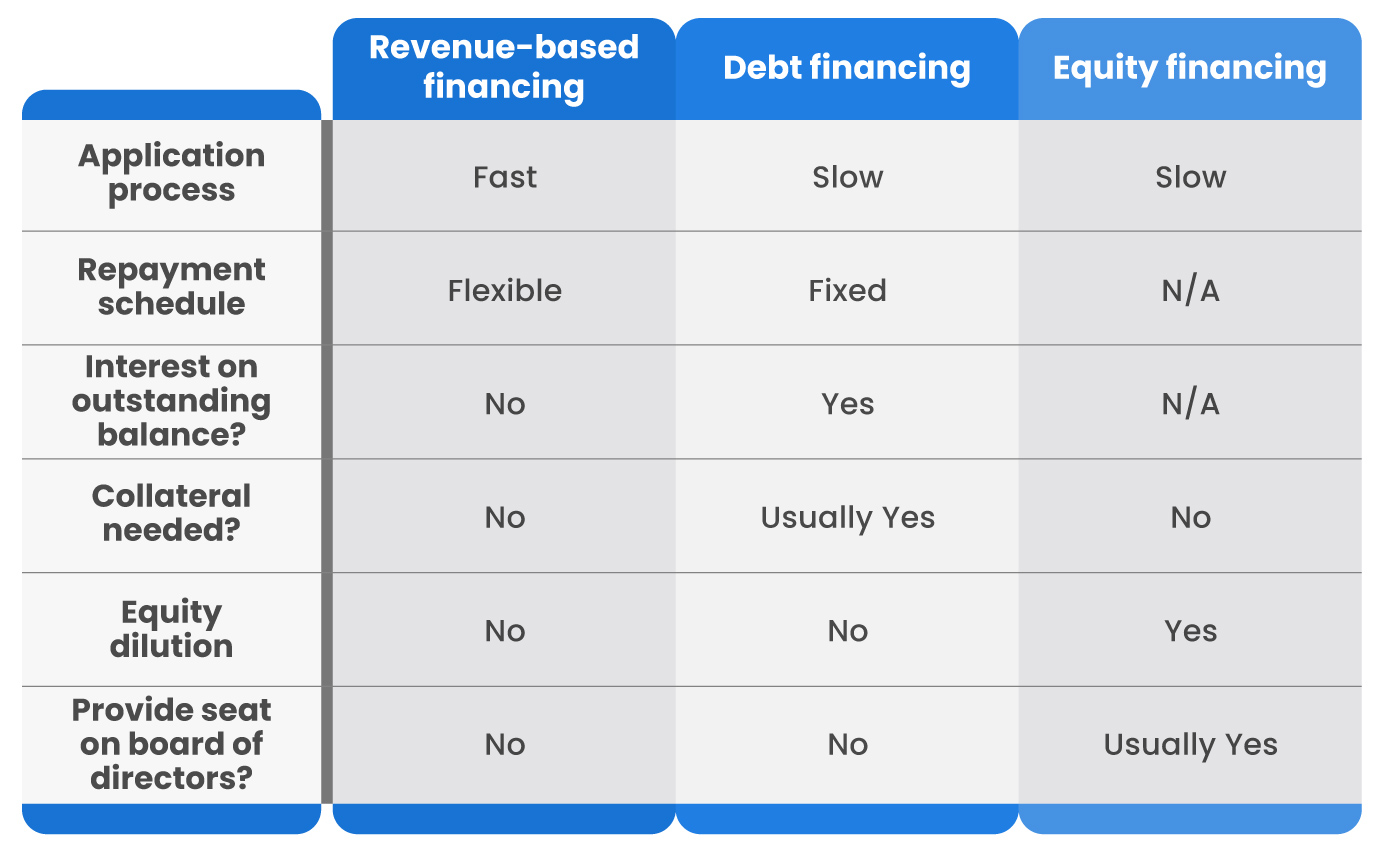

Revenue-based financing works in a similar way to debt financing, with the difference being how the funds provided by the investor are repaid by the company.

Rather than paying fixed monthly amounts on the principal, as is the case with debt financing, revenue financing involves paying a fixed percentage of monthly revenues (a ‘royalty’).

.jpg)

Naturally, this means that the repayments move up and down with the company’s top line revenues.

The repayments are made on an agreed period basis (monthly, quarterly, semesterly, etc.), by the company until the principal is paid, along with a pre-agreed multiple (“cap”) above the principal, which is the investor’s return for providing the initial funding amount. The down payments are a factor of how much revenue the company is earning, how volatile that revenue is, and its growth prospects.

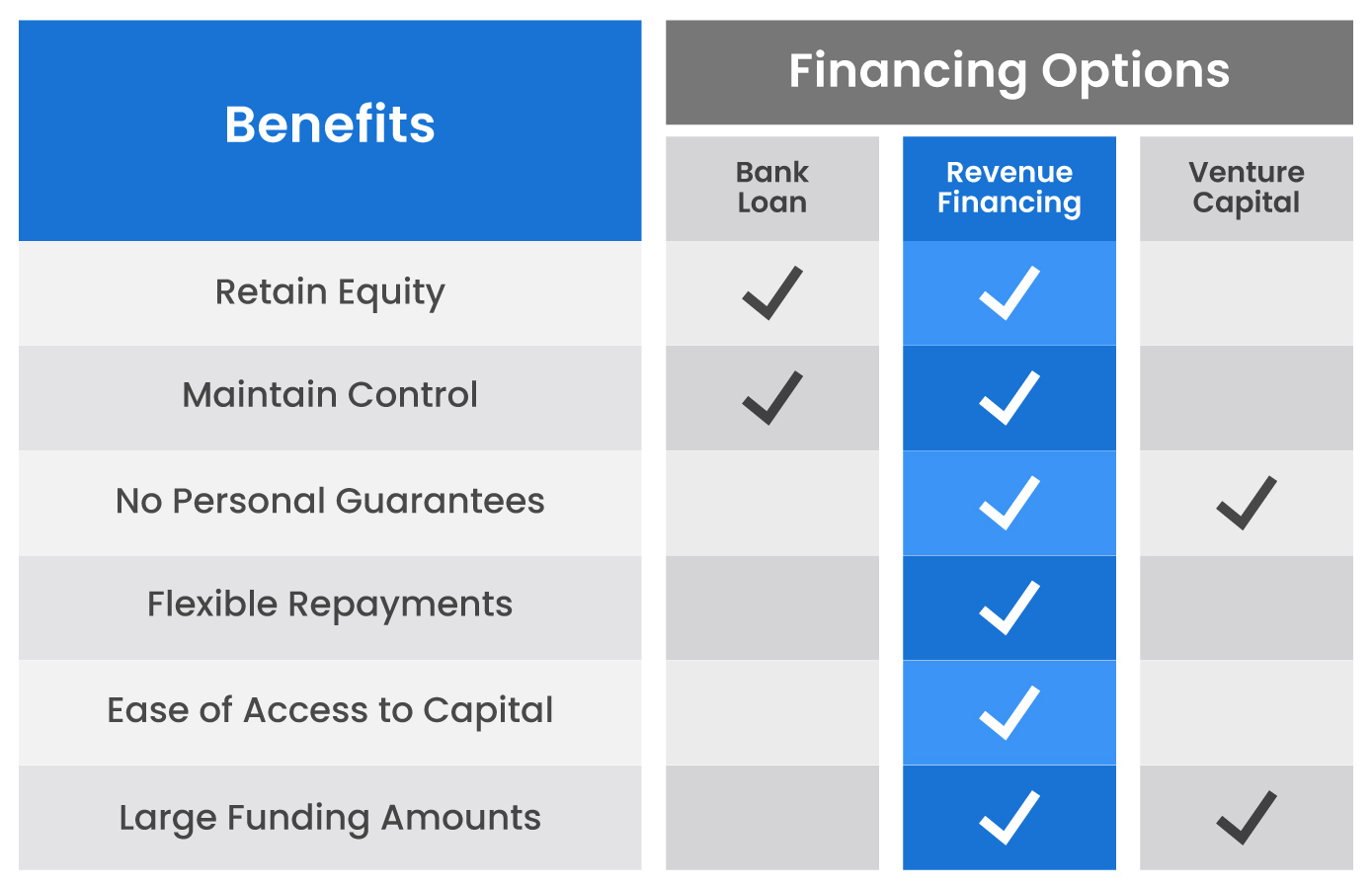

Revenue-Based Financing vs. Traditional Financing

The following chart provides a comparative checklist of the features of revenue-based financing compared to more traditional forms of financing.

Determining if Revenue-Based Financing is Right for Your Business

In short, the main factor to consider with any type of financing, revenue-based financing included, is its cost.

Whichever form of financing is the cheapest to the company is usually the one that is chosen. Of course, accurate valuations are not always easy, particularly when we take non-quantitative issues into account. But this difficulty does not extricate a company from performing a valuation of the different financing methods - a form of due diligence in itself.

When conducting the valuation, non-quantitative factors to consider when comparing revenue-based financing against other forms of financing include:

The duration of the repayment

If the repayments can be made over a longer period of time, that could be advantageous, but remember that new investors may not want to get on board if they see royalty payments taken from your gross profit each month.

The finance provider

Even if you’re a fast growing company, and revenue-based financing seems a straightforward option - and far cheaper than equity - the benefits of bringing on an expert in your industry, through a VC firm, needs to be weighed upon in the equation.

Market conditions

A company’s financing options will be determined to a large extent by the prevailing market conditions. Any company’s leadership should objectively estimate their own growth prospects and other issues like interest rate hikes and ongoing inflation before opting for revenue-based financing.

Advantages and Disadvantages of Revenue-Based Financing

In addition to the qualitative points outlined above, the advantages of RBF should be considered.

Advantages include:

Retain equity: With revenue-based financing, there is no need for an owner to reduce their share of control in their company.

Flexibility: Unlike debt repayments, which reoccur every month at the same rate regardless of the company performance, with revenue-based financing, the repayments are at least commensurate with company performance. Furthermore, the terms of the repayments can be set in advance to provide an even higher level of flexibility.

Faster access to capital: While debt and equity financing can take several months, and multiple rounds of due diligence, revenue-based financing tends to be significantly faster.

The advantages naturally have to be considered alongside the disadvantages.

Disadvantages Include:

Revenue is required: Unlike debt and equity financing, pre-revenue companies cannot access revenue-based financing (for obvious reasons).

Lower levels of financing: The levels of financing provided by revenue-based financing tend to be much lower than that of debt and equity financing.

Limited availability: The market for revenue-based financing, as the $900 million figure outlined at the beginning of this article suggests, is not even a fraction as liquid as that of traditional markets, severely limiting the ability of many companies to take advantage (for now, at least).

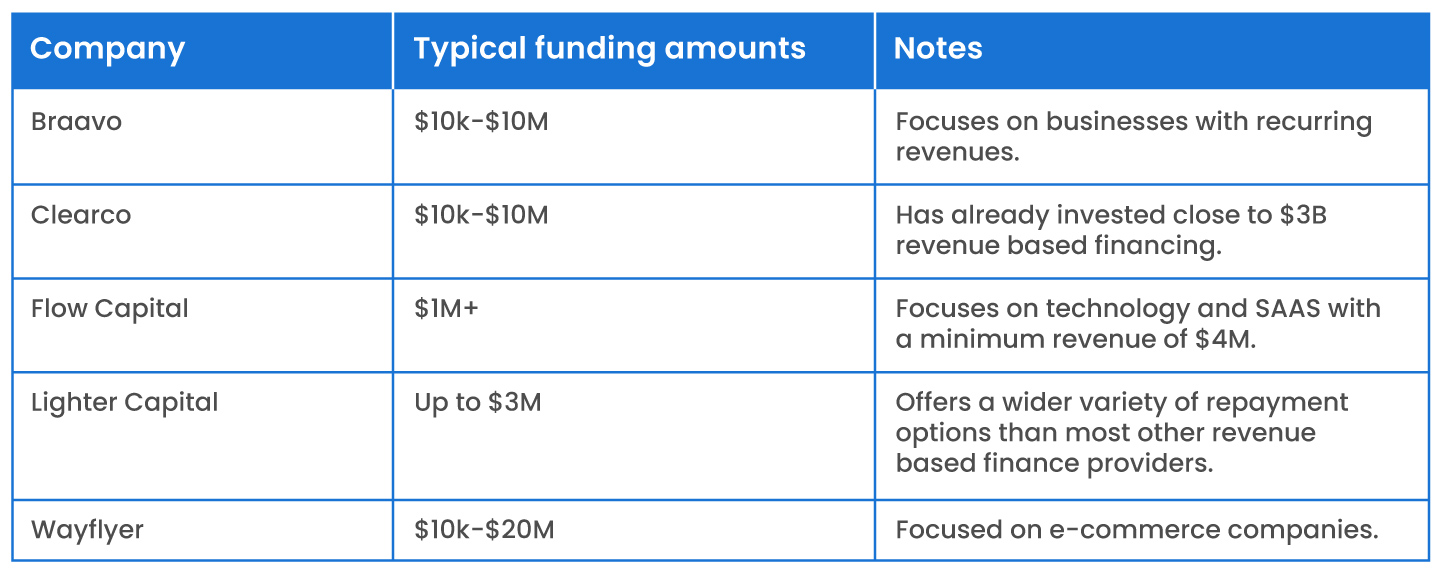

Who Provides Revenue-Based Financing?

The following is a sample of some revenue-based financing providers in North America.

Bear in mind, that for this industry to grow at the rate projected by industry analysts, new players - including those more established in other forms of finance - are likely to come online all the time.

How to Choose a Revenue-Based Financing provider?

This article should provide you with some ideas on how to choose a revenue-based financing provider.

Conduct a thorough valuation of each source of financing on its own merits, and this should better inform your decision on which provider to choose.

Related Resources:

Venture Debt: A Guide to Venture Debt Financing

Mezzanine Financing 101: Definition, How it Works

Summary

The growth of revenue-based financing should be welcomed by startup and high-growth company owners. Its arrival on the funding scene provides another valuable option for companies looking for financing.

Any company considering revenue-based financing should weigh its pros and cons against those of other types of financing, maximizing the company’s opportunities for accessing value-generating capital.

%2520(1)-p-800.jpeg)

.avif)

.png)