Venture-backed companies in the U.S. completed 995 acquisition exits in 2025 vs. 62 IPOs, according to PitchBook-NVCA Venture Monitor. These 18 venture capital firms, the largest in this ranking with $621 billion in combined assets under management as of Q1 2026 (add up the AUM in the table below), have realized the largest exits from those portfolios via M&A, such as Google's $32 billion acquisition of Wiz. Here is everything about each firm's AUM, stage focus and M&A exit record, the largest acquisitions from these VC portfolios and what buyers should know before acquiring a VC-backed startup.

I’ve worked on the buy side my entire career. First as an M&A advisor, now developing software for deal teams. The divide between venture and M&A continues to blur. The companies featured on these firms’ fund factsheets are the same companies appearing in our customers’ deal pipelines.

The 18 largest VC firms at a glance

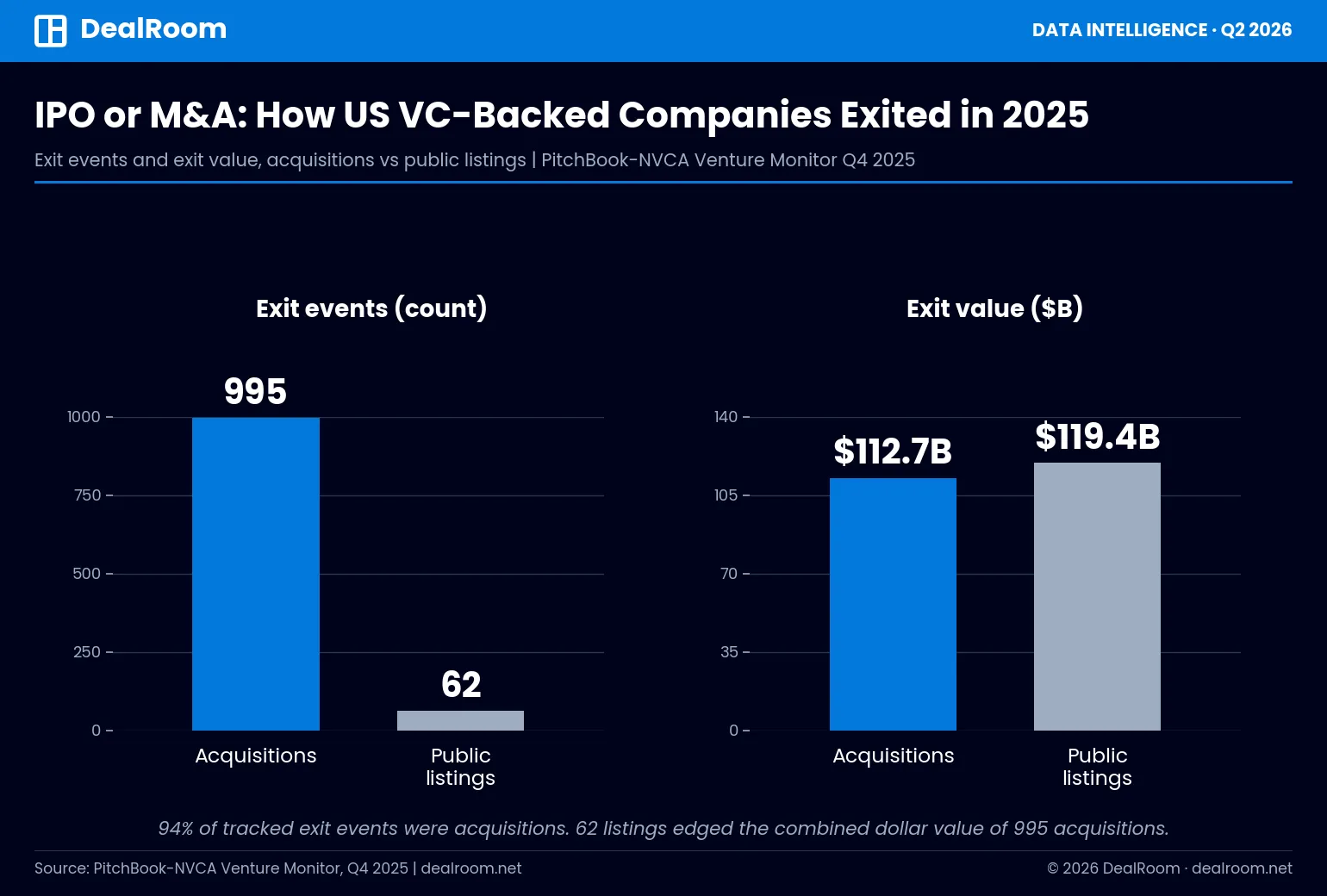

M&A is now the default exit for VC-backed companies

Exit math is skewed. PitchBook and NVCA counted 995 acquisitions of US VC-backed companies valued at $112.7 billion in 2025 compared to 62 public offerings worth $119.4 billion (Venture Monitor Q4 2025). 94% of exit events were sales to acquirers while IPOs, heavily weighted by a few large-cap listings, nudged the dollar amount. Realistically the liquidity option for any given portfolio company is a sale not a listing.

The same is true at the top of the market. Cisco closed its $3.7 billion deal for AppDynamics two days before the company was scheduled to price its IPO. SAP followed suit with Qualtrics, shelling out $8 billion in cash days before its target’s anticipated IPO. Wiz rejected a $23 billion offer from Google in 2024 only to accept $32 billion a year later. Bottom line for buyers: Don't let a credible IPO path scare you away from a VC-backed target. It's often the catalyst for a decision.

The biggest M&A exits from these portfolios

The largest exits of VC-backed companies are almost exclusively from these portfolios. Google’s $32 billion acquisition of Wiz is the largest ever for a venture-backed company. All deals below were VC-backed at time of exit and had at least one investor from this list on the cap table.

Firm profiles: AUM, focus and exit behavior

1. Andreessen Horowitz (a16z)

$90.0B AUM | Menlo Park | Founded 2009

a16z runs dedicated funds across consumer, enterprise, fintech, bio and health, crypto, games, American Dynamism and infrastructure. Its holdings include two of the most analyzed technology deals of the past decade: Microsoft's $7.5 billion acquisition of GitHub and Facebook's $1 billion acquisition of Instagram, each sourced from among the earliest vintages of a16z. Managing $90 billion and dozens of late-stage positions, board members at a16z sit across the table in a significant percentage of large tech mergers and acquisitions.

2. Insight Partners

$90.0B AUM | New York | Founded 1995

Insight leads all firms on this list by volume as both a software focused growth investor and M&A seller. Insight has disclosed over 200 M&A exits and 70+ IPOs. Companies in which Insight had positions at sale include Wiz, Qualtrics and Cylance. For buyers of B2B software, targeting a company backed by Insight likely means audited metrics, professionalized GTM efforts and a board experienced with what a clean process looks like.

3. Tiger Global Management

$58.5B AUM | New York | Founded 2001

Tiger invested over $35 billion in investments in 2021. It retreated significantly in 2022 and today focuses on AI infrastructure, vertical SaaS, and fintech. Tiger has a very hands-off operating style, so Tiger investors seldom block a deal. Credit Karma's $7.1B exit to Intuit and Moveworks' $2.85B exit to ServiceNow were both from Tiger-occupied cap tables.

4. Sequoia Capital

$56.0B AUM | Menlo Park | Founded 1972

The oldest franchise also has the deepest M&A exit history: WhatsApp, GitHub, Qualtrics and Wiz all had Sequoia on the cap table at exit. Since the 2023 breakup into Sequoia (US/Europe), Peak XV (India/ Southeast Asia) and HongShan (China), acquirers should consider each entity its own counterparty with its own portfolio.

5. Legend Capital

$48.1B AUM | Beijing | Founded 2001

Legend Holdings (parent of Lenovo) has funds investing in USD and RMB denominated deals throughout greater China through its venture and growth arm. Exits have tended to be via Asian exchange listings rather than trade sales. Cross-border M&A by Legend backed companies also involve CFIUS and Chinese regulatory review as part of any deal process.

6. Thrive Capital

$37.0B AUM | New York | Founded 2009

Joshua Kushner's firm typically only invests in 8 to 12 companies annually with full conviction. Thrive closed Thrive X at $10 billion in early 2026. Thrive co-led the last private funding round for Wiz and held GitHub before it was sold to Microsoft. Shares are tightly held, so a position at Thrive is usually large enough to anchor or veto an exit. This limits negotiations to key decision makers.

7. General Catalyst

$30.0B AUM | Cambridge | Founded 2000

GC operates multi-stage practices in Health Assurance, enterprise defense, AI infrastructure and consumer. Perhaps most notably, GC is the best example we’ve seen of a venture firm transitioning to become a strategic acquirer itself: its Health Assurance Transformation group outright acquired Ohio-based health system Summa Health. Corporate development teams in healthcare will increasingly see GC as a competitor to make bids, not just as a company to sell to.

8. New Enterprise Associates (NEA)

$25.9B AUM | Chevy Chase | Founded 1977

NEA closed its 18th flagship fund in 2023. NEA's healthcare team has invested in over 250 companies and generated 90+ IPOs. The exit profile is public market heavy. But because NEA holds such large positions in mid-stage healthcare and enterprise businesses, NEA is one of the most common counterparties in growth-stage carve-out and roll-up discussions.

9. Lightspeed Venture Partners

$25.0B AUM | Menlo Park | Founded 2000

Lightspeed has managed independent funds in the U.S., India, Israel and Europe. It led AppDynamics' A round and stayed on through Cisco's $3.7 billion pre-IPO acquisition. It backed Moveworks through its $2.85 billion sale to ServiceNow and held Wiz at IPO. Few firms have successfully exited via strategic transactions more than Lightspeed.

10. Dragoneer Investment Group

$21.7B AUM | San Francisco | Founded 2012

Dragoneer is a public/private hybrid investor that often comes in two to four years pre-IPO and holds through the listing. If they're on the cap table, it's generally safe to assume an IPO-first strategy, so an acquirer must offer a premium to win that is more attractive than the public markets.

11. Bessemer Venture Partners

$20.0B AUM | San Francisco | Founded 1981

Bessemer has led the most deals in vertical SaaS, cloud infrastructure, fintech and healthcare through Series A-C and publishes research behind its investment theses. Auth0's sale to Okta for $6.5 billion is Bessemer's largest strategic exit of the cloud era. Bessemer backed companies come with clean, benchmarked SaaS metrics, allowing for shorter financial diligence.

12. Accel

$20.0B AUM | Palo Alto | Founded 1983

Accel’s thesis-driven, ‘prepared mind’ approach to research has fueled enterprise software Series A deals in software infrastructure and dev tools. Accel held Qualtrics at SAP's $8 billion cash deal and was the largest venture holder in Slack, which sold to Salesforce for $27.7 billion following its direct listing. Accel is on the buy and sell side of enterprise software consolidation.

13. Technology Crossover Ventures (TCV)

$19.9B AUM | Menlo Park | Founded 1995

TCV invests $50 million to $300 million checks into late-stage internet and software businesses generating $30 million or more in revenue. Its crossover strategy biases towards IPO results (Netflix, Spotify, Toast), so TCV-backed targets often go to market only after public windows have closed.

14. OrbiMed

$18.3B AUM | New York | Founded 1989

The largest single purpose healthcare investor has interests in venture, public equities and royalty financing. Large pharma buyers are common for its therapeutics and device positions. Due to OrbiMed's MD and PhD bench, diligence on its portfolio companies is typically already at banker quality.

15. Battery Ventures

$16.8B AUM | Boston | Founded 1983

Battery writes checks ranging from $5 million Series As to $200 million growth rounds. Battery has also done PE-style buyouts of bootstrapped software companies. Battery is both a buyer and seller. Glassdoor's $1.2B sale to Recruit Holdings was originated from a Battery Series A investment.

16. Deerfield Management

$15.1B AUM | New York | Founded 1994

Deerfield is healthcare-only and spans venture and public equities, structured credit and royalties. Exit of therapeutics positions is predominantly via pharma acquisition or licensing, not IPO. Clinical and regulatory expertise is evident in its well-curated data rooms.

17. Khosla Ventures

$15.0B AUM | Menlo Park | Founded 2004

Vinod Khosla's firm invests in early stage deep tech, climate tech and AI infrastructure companies that have long hold periods. Khosla Ventures' biggest exit in cybersecurity is Cylance's $1.4 billion acquisition by BlackBerry. As Khosla focuses on seed deals with more science risk, technical diligence outweighs financial diligence.

18. Index Ventures

$13.0B AUM | San Francisco + London | Founded 1996

The leading trans-Atlantic firm took Wiz from its initial rounds and through the $32 billion Google exit and sold Duo Security to Cisco for $2.35 billion. Index's presence in both markets means its portfolio companies are regularly approached by both US and European strategic buyers, sometimes within the same process.

Why corp dev teams watch VC portfolios

VC portfolios are the most qualified target pool in the market: vetted by pros, benchmarked quarterly and optimized to scale. 2025 numbers prove buyers have taken notice. Deals for pre-seed, seed and Series A companies accounted for roughly 75% of all VC-backed acquisitions in 2024. VC-backed companies were the buyer on 23% of those deals, according to Venture Monitor. The types of targets being acquired are young teams bought for capabilities, not revenue.

We described this as'transact to transform' in our State of M&A report: firms acquiring to fill adjacent capabilities instead of developing them organically. We also pointed to signals emerging from within the venture market itself: one VC client shared that over one-third of the pitch decks they saw in 2023 were AI-focused. That focus is now evident across these 18 portfolios. It is precisely where buyers motivated by capability are looking.

Three key signals when screening a VC portfolio:

- Fund age. A company sitting in a 2014 vintage fund will soon feel distribution pressure. GPs with a year or two left on their fund are motivated sellers, even if the company's blog posts are all about how independent they are.

- Follow-on behavior. When insiders don't lead a round and a bridge emerges, the board has likely already started strategic options discussions.

- Investor exit profile. A Dragoneer or TCV investor means you’re about to see an IPO. An Insight or Lightspeed investor means management has sold to M&A multiple times previously.

Don’t do this on an ad hoc basis. Our customers automate this exact filtering within DealRoom Pipeline, along with their entire corporate development workflow.

Acquiring a VC-backed company: what buyers need to know

Buying into a venture-backed company is different than buying a founder-owned business in four ways. These differences become apparent during diligence and negotiation.

The preference stack determines who says yes

Proceeds are not distributed pro rata. Liquidation preferences entitle the holders of preferred stock (aka the VC funds) to a contractual minimum before any proceeds go to common stockholders. At certain prices the preferred investors may be made whole while the founders and employees receive little if anything. This kills deals that may have looked attractive based on headline price.

Run the waterfall before you let a price anchor your thinking. The interactive calculator below demonstrates how preference multiples and participation determine who gets what at any given exit value.

Approvals run through the board and the preferred

Financing docs usually need board approval and consent from one or more preferred classes. Many charters have drag-along provisions forcing common holders after thresholds are reached. Map the approval tree during week 1 diligence: don't assume a deal-supportive CEO is worthwhile if two funds have blocking positions.

Diligence is faster, but different

VC backed targets generally come in with clean financials and diligence products created at each financing. Additional focus should be on the cap table itself (option pools, SAFEs, warrants and convertible notes that convert on close), 280G golden parachute exposure, and treatment of unvested equity. See our due diligence guide for the complete request list. The venture capital due diligence checklist is the checklist we provide our customers who are pursuing these exact targets.

The sell side knows the playbook

A board that includes Insight, Sequoia or Lightspeed has seen dozens of exits. These processes are banker-driven, fast-paced and designed to produce competing bids on deadline. Companies who succeed in winning these processes run their own disciplined buy-side M&A process. They don't let the seller's timeline control them.

How these firms run due diligence (and what it means for your timeline)

Venture diligence takes less time than corporate diligence, and the difference matters when you're competing against a follow-on round instead of another bidder. Typical VC diligence timelines: 1 to 2 weeks for seed, 3 to 6 weeks for Series A and 4 to 8 weeks for growth rounds. If a strategic acquirer runs a 12 week process against a 4 week term sheet they will lose by default. There is a reason rigorously compressed diligence is the core value proposition of purpose-built tooling versus email + spreadsheets.

Frequently Asked Questions

What venture capital firm has had the largest M&A exit?

Index Ventures, Sequoia Capital, Insight Partners, Lightspeed and Thrive Capital all invested in cybersecurity startup Wiz, which Google bought for $32 billion in stock and cash. That’s the largest ever exit by way of acquisition for a venture-backed company, eclipsing the previous record holder: Sequoia-backed Facebook’s acquisition of WhatsApp in 2014, which closed at $21.8 billion.

Who has the most money in venture capital?

Andreessen Horowitz and Insight Partners currently stand at about $90 billion each in assets under management as of Q1 2026. Tiger Global Management is third with $58.5 billion, with Sequoia Capital at $56 billion.

Do VC-backed startups exit through IPO or acquisition?

Venture capital exits were overwhelmingly via acquisition by count. PitchBook and NVCA counted 995 acquisitions of US VC backed companies in 2025 versus 62 IPOs. When measured by dollar value, however, the two were close because there were several large IPOs.

How much time do you have to conduct due diligence on a VC backed target?

Venture rounds send this signal: about 1-2 weeks at seed, 3-6 weeks at Series A and 4-8 weeks at growth stage. Strategic buyers will generally take longer than that for confirmatory diligence. Hence due diligence prep before LOI is especially important in these deals.

What is liquidation preference and why does it matter in M&A?

Liquidation preference is the contractual right of preferred stockholders to receive a certain multiple (typically 1x) of its investment before common shareholders receive any proceeds in a sale. The preference dictates who actually makes money at a given price and thus who is for/against the deal. Ask yourself: who fills the pockets at closing? Acquirers should model the preference waterfall prior to making an offer.

How is venture capital different from private equity in M&A?

Venture capital and private equity are often talked about in the same sentence when discussing mergers and acquisitions. This is because they are different forms of private equity. VC firms take minority positions in start-ups and usually exit via trade sale of a single position. PE firms acquire controlling interests, hold for 4-7 years, then exit entire companies. This means the VC seller negotiates with many voices on a board, while PE seller controls the process from beginning to end.

Methodology

Rankings are based on public information, primarily SEC Form ADV filings, as well as annual firm reports and corroborated data from Bloomberg, Forbes and the Financial Times. Asset sizes reflect total assets under management, only including firms with $10 billion or more in committed venture or growth capital. M&A exit data is compiled from SEC filings as well as announcements from acquirers and other news published via links in the exits table. Exit market data is from PitchBook- NVCA Venture Monitor, Q4 2025. Remember this is a ranking by size of AUM, not necessarily firm quality or returns.

.avif)

.webp)