Understanding Series A, B, C, D, and E Funding Stages

.avif)

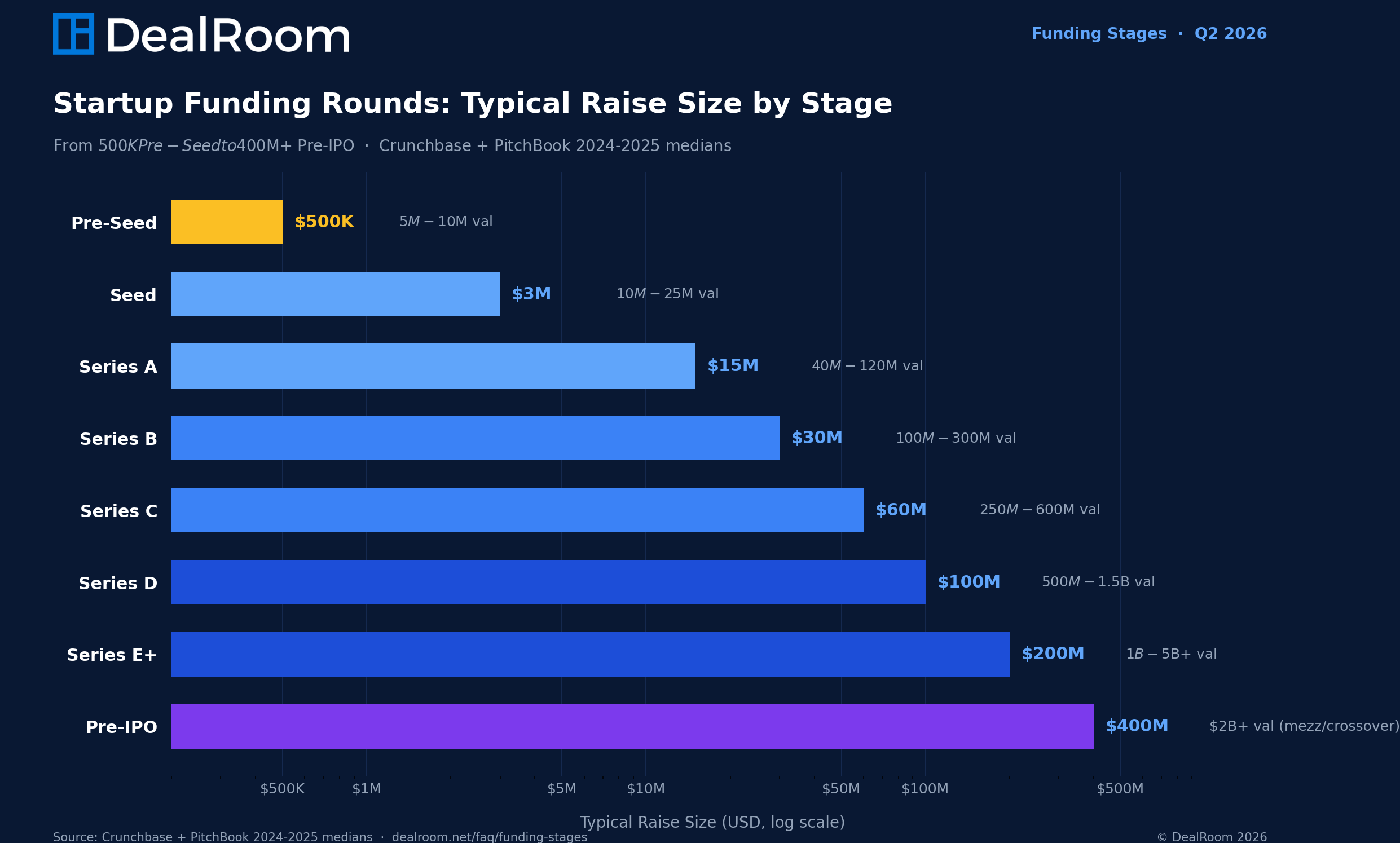

Startup funding rounds typically scale through 8 stages with concrete 2026 medians: Pre-Seed (~$500K at $5M-$10M valuation), Seed (~$3M at $10M-$25M), Series A (~$15M at $40M-$120M), Series B (~$30M at $100M-$300M), Series C (~$60M at $250M-$600M), Series D (~$100M at $500M-$1.5B), Series E+ (~$200M at $1B-$5B+), and Pre-IPO (~$400M+ at $2B+).

Founders typically give up 15-25% per round at Pre-Seed through Series A, narrowing to 5-12% at later stages as the cap table thickens. Investor profiles shift from angels and accelerators (Pre-Seed) through tier-1 VCs (Series A) to crossover funds and sovereign wealth (Series D+). Below: a comparison table, an interactive funding calculator that estimates raise size and dilution for your stage and sector, plus alternatives to equity (venture debt, revenue-based financing).

2026 Funding Round Benchmarks

Median raise size, valuation, investor type, and dilution for every stage from Pre-Seed to Pre-IPO. At-a-glance reference table.

| Stage | Typical Raise | Typical Valuation | Investor Type | Dilution |

|---|---|---|---|---|

| Pre-Seed | $250K–$1.5M~$500K typical | $5M–$10M | Angels, F&F, accelerators | 10–20% |

| Seed | $1.5M–$6M~$3M typical | $10M–$25M | Seed VCs, multi-stage seed programs | 15–25% |

| Series A | $10M–$25M~$15M typical | $40M–$120M | Tier-1 VCs (a16z, Sequoia, Accel) | 18–25% |

| Series B | $20M–$60M~$30M typical | $100M–$300M | Growth-stage VCs (Insight, Tiger, IVP) | 15–22% |

| Series C | $30M–$100M~$60M typical | $250M–$600M | Late-stage VCs, crossover funds | 12–20% |

| Series D | $50M–$200M~$100M typical | $500M–$1.5B | Mega-funds, hedge funds, sovereigns | 8–15% |

| Series E+ | $100M–$500M+~$200M typical | $1B–$5B+ | Pre-IPO crossover, mutual funds | 5–12% |

| Pre-IPO | $200M–$1B+~$400M typical | $2B+ | Mezzanine, public-mutual-fund crossover | 3–8% |

We built this simple tool to see how different groups of stages compare on key metrics:

Startup Funding Stages: Side-by-Side Comparison

Typical raise size, valuation, investor types, dilution, and timeline for every funding stage from Pre-Seed to Pre-IPO. Sortable by any column. 2026 benchmarks.

| Stage↕ | Typical Raise↕ | Typical Valuation↕ | Typical Investors | Dilution | Time to Close |

|---|

As well as this funding calculator to give you a rough sense of what to expect based on a variety of factors:

Funding Round Calculator

Pick your stage, sector, revenue, and growth rate. We’ll estimate your typical raise size, valuation, dilution, and the right investor types for your round.

The Funding Process

The startup funding journey consists of phases with distinct goals and challenges. It often begins with pre-seed or seed-stage funding, when companies usually have little more than a concept or a minimum viable product (MVP) and yield little to no revenue. As startups move into the venture capital phase—starting with Series A funding—the focus shifts to scaling the business and generating a predictable revenue stream.

The goal of startup funding is to ensure that an early-stage startup has the financial resources it needs to scale the business and enable investors to see a return on their investment (ROI). While there are no strict rules for the amount of money or equity exchanged at each stage, the stakes generally tend to be higher in the early stages than later when the company is more established.

Types of Companies Investors Look For

Types of Companies Investors Look For Each investor has specific criteria when deciding whether to invest in a startup. While many say they invest in people rather than just ideas, at the end of the day, investors are looking for companies with clear growth potential and a competitive advantage.

Here are some common traits that attract investors:

Strong Elevator Pitch: Present a concise company overview to emphasize your primary value proposition and establish an initial connection with a potential investor.

High Margins or High Volume: The company should have the potential to sustain high margins or volume, which are critical to generating long-term value.

Monopolistic Characteristics: Potential investors want companies with unique advantages, such as a patent or distinctive market fit.

Clear Exit Plan: Investors want to see a clear path to exit, whether through an acquisition or IPO.

Pre-Seed Funding

Pre-Seed is the first institutional funding round, typically raising $250K-$1.5M (median ~$500K) at a $5M-$10M post-money valuation. Investors: angel investors and friends-and-family, accelerators (Y Combinator, Techstars, 500 Global, Antler), and pre-seed micro-funds (Hustle Fund, Forum Ventures, Hawthorne). Used to: validate the idea, build a working MVP, and form the founding team. Typical dilution: 10-20%. Time to close: 1-3 months.

Seed Funding

Seed is the second funding round, typically raising $1.5M-$6M (median ~$3M) at a $10M-$25M post-money valuation. Investors: dedicated seed VCs (Floodgate, First Round, Initialized, Felicis), multi-stage VC seed programs (Sequoia Arc, a16z Seed, Lightspeed Seed), and strategic angels and AngelList syndicates. Used to: prove product-market fit and build the initial go-to-market motion. Typical dilution: 15-25%. Time to close: 2-4 months.

The seed round is the first official funding stage. Here, early-stage startups exchange equity for capital to finance growth initiatives such as product development or hiring new team members. By this point, some revenue generation is expected, and according to Carta, funding amounts can range from $500k to 5 million. Alternatives to raising funds through Angel investors are also common. Because the timeline for a return on investment can be as long as ten years, this stage may require a significant leap of faith from investors.

Series A Funding

Series A is the third funding round, typically raising $10M-$25M (median ~$15M) at a $40M-$120M post-money valuation. Investors: tier-1 venture capital firms (Andreessen Horowitz, Sequoia, Accel, Lightspeed, Bessemer, Index, Greylock, Benchmark) and sector-specialist VCs. Used to: scale a validated PMF into a repeatable go-to-market motion (typically requires $1M-$3M ARR for SaaS, comparable traction proof for other models). Typical dilution: 18-25%. Time to close: 3-5 months.

Series A funding is a critical milestone in a startup's journey, marking the transition from initial seed funding to more substantial investments. Friends and family will likely take a back seat as Venture Capital (VC) firms come into play. These potential investors bring capital, strategic guidance, and industry connections, conducting rigorous due diligence to evaluate the startup's growth potential, market opportunity, revenue generation, and scalability.

When a company reaches Series A, it must clearly indicate a precise product-market fit, though it may not be profitable. The primary goal of this funding round is to accelerate growth, which often involves expanding operations, increasing market presence, and growing the team. According to insights from Kruze Consulting, typical valuations for startups raising Series A funding come in at $40 million.

How much money can the Series A Funding Round raise?

Funding at this stage varies based on the startup and its needs. Investors evaluate everything from the business concept to early market traction, founding team members, and the financial model. Growth List is a helpful resource for insight into the latest funded Series A startups.

What type of investors offer Series A funding?

This level of funding typically comes from professional investors like VC firms, PE firms, and hedge funds. These investors seek startups with a strong market need and a strategic plan that indicates a high potential for success. To secure funding, startups need to present a clear business plan and showcase early market traction, proving there is demand for their product or service and that they are on a path to scale.

What should you use Series A funding for?

This stage of funding is all about growing the business. This could involve leveraging the investment to expand operations, increase market presence, or develop the team.

How companies get Series A funding

Finding the right investor is the biggest challenge. The dream is landing big names like Sequoia Capital or Andreessen Horowitz. However, it’s often more practical to seek out lesser-known VC firms that are still highly reputable. Remember that even if initial pitches don’t result in funding, the feedback received can be invaluable for refining your business plan and improving your chances in future rounds.

Here is a helpful resource to set you up for success: 7 Crucial Steps to Take Before a VC Fundraising Round

Series B Funding

Series B is the fourth funding round, typically raising $20M-$60M (median ~$30M) at a $100M-$300M post-money valuation. Investors: growth-stage VCs (Insight Partners, Tiger Global, Iconiq, IVP, Meritech, General Atlantic), Series A leads taking pro-rata, and strategic corporate VCs writing $10M-$30M. Used to: scale into new markets, geographies, or product lines after PMF and unit economics are proven (typically requires $5M-$15M ARR). Typical dilution: 15-22%. Time to close: 4-6 months.

When a startup reaches Series B funding, it should be seen as a company with significant growth potential within the VC ecosystem. This round focuses on further scaling, increasing revenue, and improving the product offering. According to the Growth List, Series B funding often starts as low as 500k and can grow to over 300 million.

Take AI startup Skild AI, for example. Once the funding happens, existing investors may continue with their investments. At the same time, new specialized investors in later-stage funding rounds may also join, drawn by the reduced risk compared to earlier stages.

How much money can the Series B round raise?

This stage of funding is all about scaling the business. Securing Series B funding will catalyze the next level of growth and tee a company up for later financing rounds. According to the Growth List, this level of investment can start at 500k and grow to 300 million and beyond.

What type of investors offer Series B funding?

This level of funding is primarily from established VC firms. To learn about the top VC players, read our blog, 15 Top Venture Capital Firms in the World.

What should you use Series B funding for?

Companies typically use Series B funding to continue growing their businesses. This includes expanding into new markets, refining their product offering, and expanding their team.

How companies get Series B funding

If a company is securing Series B funding, it likely has established itself in the market, proving its growth and scalable business model. To get to the next round of funding, it will likely need to continue refining its elevator pitch, highlighting how future investments will contribute to its product development, market expansion, and future maturation.

Series C Funding

Series C is the fifth funding round, typically raising $30M-$100M (median ~$60M) at a $250M-$600M post-money valuation. Investors: late-stage VCs (Dragoneer, TCV, Coatue, D1 Capital), crossover funds (T. Rowe Price, Fidelity, Wellington), and sovereign wealth + family offices (Mubadala, Temasek). Used to: capture market share aggressively, fund acquisitions, or build the platform infrastructure to support a 10x scale-up (typically $20M+ ARR). Typical dilution: 12-20%. Time to close: 4-7 months.

By Series C, a company is well-established, with substantial and predictable revenue and market presence. Investors at this stage see less risk, and competition among them can increase the company’s valuation. Entrepreneurs often use Series C funds to fuel further growth, which could translate into acquisitions or regional expansion. Investors outside the traditional VC ecosystem—such as private equity (PE) firms, hedge funds, or even sovereign wealth funds—often participate in this round, attracted by the prospect of a future IPO.

How much money can the Series C funding round raise?

According to Growth List, recent Series C funding can range from 1 million, like Lucid Green, to over 1 billion like Core Weave’s 2024 Series C funding.

What type of investors offer Series C funding?

By now, a company has already gone through several funding rounds, and initial investors are likely still in the mix. Nonetheless, the main players will remain the same, ranging from VC firms, PE firms, hedge funds, and investment banks to corporate investors.

What should you use Series C funding for?

With the company already established, it’ will use the funding to expand into new markets or regions, develop new product offerings, acquire other companies, or prepare for an IPO.

How companies get Series C funding

To get this level of funding, a company should be able to show investors it’s ready to scale, enter new markets or regions, or prepare for an IPO. This demonstrates that the business is robust and capable of significant growth.

Series D Funding

Series D is the sixth funding round, typically raising $50M-$200M (median ~$100M) at a $500M-$1.5B post-money valuation. Investors: mega-funds (SoftBank Vision Fund, Tiger Global, Coatue), hedge funds with growth portfolios, and mutual-fund crossover positioning for IPO. Used to: extend runway, fund step-change M&A, or buy time before a delayed IPO window. Typical dilution: 8-15%. Time to close: 5-8 months.

At Series D, the company is typically a household name, and the funding round is often less about necessity and more about taking advantage of favorable market conditions. For instance, Facebook’s Series D round in 2009 raised $200 million, earning it a near $10 billion valuation. By this stage, Facebook didn’t need additional funds but raised them to strengthen its market position.

How much money can the Series D funding round raise?

According to Arc, Series D funding rounds average around $50 million, though some can exceed $300 million, especially for companies preparing for an IPO or major expansion.

What type of investors offer Series D funding?

The leading players, including VC, PE, hedge funds, investment banks, and corporate investors, will remain the same.

What should you use Series D funding for?

Companies often use Series D funds to prepare their operations and finances for an initial public offering(IPO). This would include refining their business model, strengthening the balance sheet, and ensuring compliance with regulatory requirements.

How do companies get Series D Funding?

To get Series D funding, companies need to show predictable growth and a clear plan for an exit, like an IPO or acquisition. This typically involves showcasing strong financials, a solid exit strategy, and being prepared for thorough due diligence.

Series E, F, and G Funding Rounds and Beyond!

Series E and beyond is for companies that have stayed private longer than the standard A-D path, typically raising $100M-$500M+ (median ~$200M+) at a $1B-$5B+ post-money valuation. Investors: late-stage crossover funds, sovereign wealth (PIF, Mubadala, GIC, Temasek), and mezzanine capital (Apollo, Ares, Blackstone Tactical Opportunities). Used to: bridge to an IPO that has been postponed, fund large-scale international expansion, or refinance earlier rounds with friendlier secondary terms. Typical dilution: 5-12%. Time to close: 6-10 months.

While Series A through D are the most common stages, there isn’t a limit to the number of funding rounds a company can pursue. Series E, F, and beyond are becoming increasingly common, but they come with diminishing returns as the company’s growth potential is gradually realized. Early-stage investments carry the highest risk and the biggest reward potential, while later-stage investments tend to be safer but offer smaller returns.

Pre-IPO / Mezzanine

Pre-IPO (also called mezzanine or crossover) financing is the last priced round before going public, typically raising $200M-$1B+ (median ~$400M+) at a $2B+ valuation. Investors: mezzanine lenders, public mutual fund crossover (T. Rowe Price, Fidelity, Capital Group), and structured-equity providers. Used to: lock in the pre-IPO price, build buyer awareness, and provide secondary liquidity to early employees and investors. Typical dilution: 3-8%. Time to close: 8-12 months, often run concurrently with the S-1 filing.

Alternatives to Series Funding Rounds

While traditional series funding may be the popular route for startups, several alternatives could be a better fit depending on your business needs. Options like bootstrapping, where you grow your company using personal savings or revenue, or crowdfunding, where you raise small amounts of money from a large number of people, are also viable options. Venture debt and angel investing can also raise capital without giving up significant equity. Each of these alternatives offers different benefits and risks, depending on your stage of growth and financial goals.

For a deeper understanding, take a look at the alternatives in these articles:

Venture Debt

Venture debt is a loan provided by specialized lenders (Silicon Valley Bank, Hercules Capital, Trinity Capital, Atel) to venture-backed startups, typically alongside or after a priced equity round. It is non-dilutive: you keep your ownership but take on a payment obligation. Common structures:

- Term loan: $1M-$25M+, 3-4 year term, 8-13% interest, interest-only period 6-18 months, then amortizing. Typically secured by all assets.

- Warrants attached: lender takes warrant coverage equal to ~5-10% of loan principal at the most recent equity-round price.

- Best for: companies that just closed equity (proves quality), have 12+ months of runway, and want to extend runway without diluting again.

Avoid venture debt if you have less than 12 months of cash, unclear path to next round, or covenants you can't reliably hit.

Revenue-Based Financing (RBF)

Revenue-based financing advances capital against future revenue, repaid as a fixed percentage of monthly sales. Major providers: Stripe Capital, Pipe, Capchase, Clearco, Lighter Capital. Common structures:

- Repayment: 1-12% of monthly revenue until a fixed multiple (typically 1.3x-1.6x of advanced amount) is repaid.

- Term: 6-36 months depending on revenue volatility.

- Best for: SaaS / e-commerce companies with predictable monthly revenue, $200K+ MRR, 18+ months of operating history.

Avoid RBF if you have lumpy or seasonal revenue, gross margins below 50% (the take rate eats your profitability), or near-term plans to raise priced equity (RBF claims complicate the cap table).

Convertible Notes and SAFEs

For pre-priced rounds (Pre-Seed and Seed), convertible notes and SAFEs (Simple Agreements for Future Equity) are simpler instruments than priced equity rounds. They convert to stock at the next priced round (typically Series A) at a discount or cap. Best for sub-$2M rounds where the cost and complexity of a full priced round isn't justified.

Key Takeaways: How to Raise Venture Capital

Before approaching any investor, make sure your business is ready: you need a Minimum Viable Product (MVP), a commercially viable concept, and a scalable model. VCs are buying into a long-term partnership — arriving without these puts you at a serious disadvantage.

Once you're ready, the process typically moves through these stages:

- Prepare your pitch deck — Expect it to evolve with every investor conversation. Use a virtual data room to track versions and which investors have seen what.

- Early meetings — These run like job interviews. You'll be asked about your team's background, why you founded the company, and your five-year vision.

- Partner meetings — Expect deeper scrutiny of your business model, market, and competitive landscape. This is also when you should assess cultural fit and clarify what you need beyond capital (operational support, technical expertise, introductions).

- Term sheet — A successful partner process leads to a term sheet outlining proposed investment terms.

- Due diligence & close — The firm conducts formal due diligence before both parties sign to close the round.

How DealRoom can help with startup funding rounds

Navigating the world of startup funding is intimidating, but for most, it is essential. From pre-seed financing to the later stages like Series E, understanding what each stage is all about and how it can impact your company is crucial. These funding rounds do more than provide the money you need to grow—they validate your business, attract the right investors, and set you up for long-term success.

Whether you're just getting started with a big idea or gearing up for an IPO, knowing the details of each funding stage helps you make the right decisions for your company. And remember, while many startups follow the traditional funding route, options like bootstrapping and crowdfunding can be great alternatives depending on your business needs.,

At DealRoom, we're here to help you through this process. Our tools are designed to make raising funds more accessible and more efficient. Staying informed and organized is vital as you build and scale your business. Using tools like our virtual data room, FirmRoom can help you keep everything in order—managing documents, collaborating with investors, or ensuring due diligence goes smoothly. We're here to support you every step of the way. Click here to start a free trial or talk to our team.

Get your M&A process in order. Use DealRoom as a single source of truth and align your team.