Blog

M&A Blog by Dealroom – exclusive insights and expertise on the Mergers & Acquisitions market, along with practical ideas for successful M&A

Featured

.png)

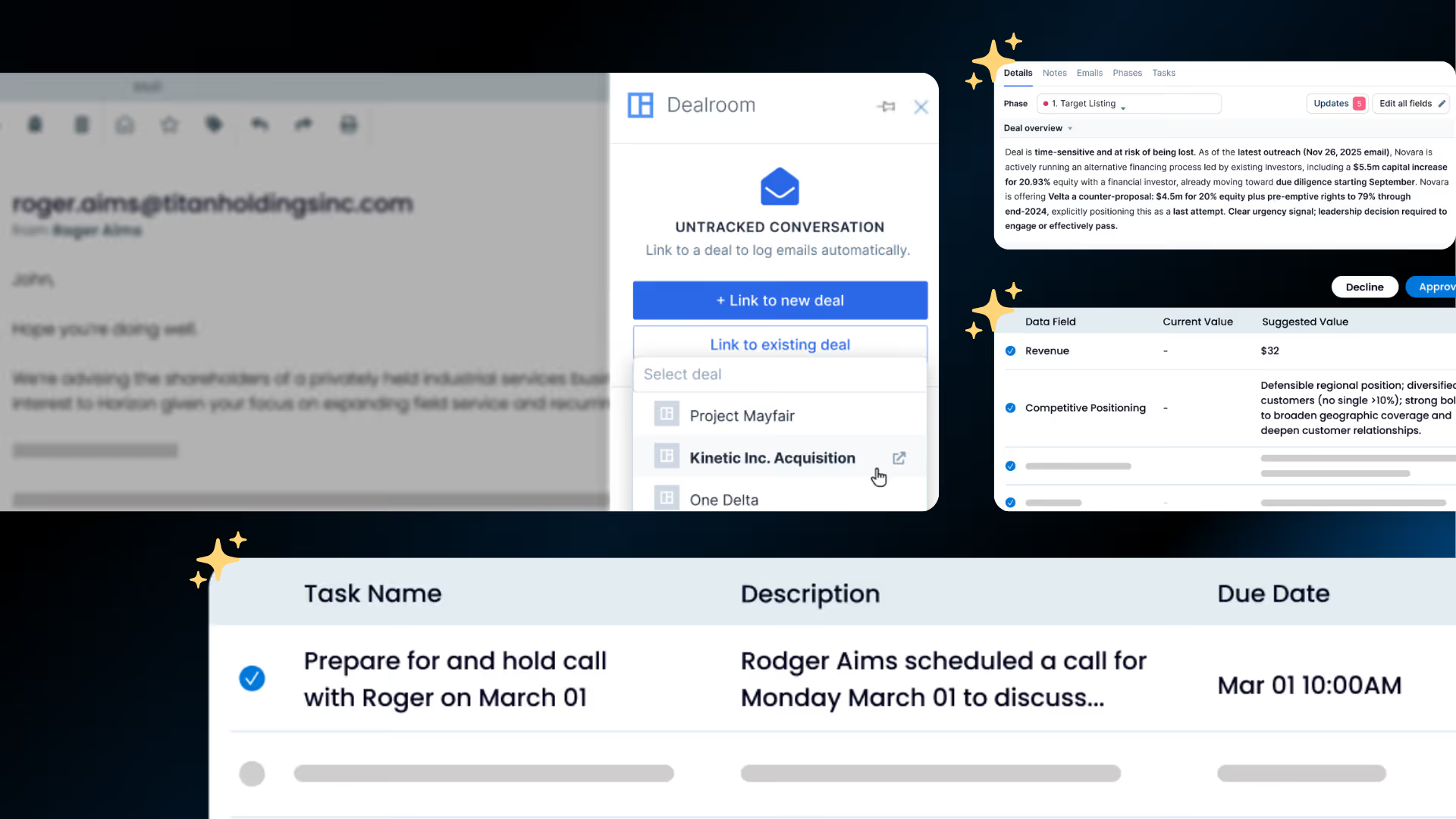

DealRoom Powers Secure Collaboration Across the M&A Deal Lifecycle with New Permissions Features

Permission enhancements give deal teams precise control over who sees what, so sensitive work stays protected and deals move faster

.webp)

.png)

.avif)

The Buyer-Led M&A™ Newsletter by DealRoom

A no-nonsense take on what drives real value in modern M&A

.png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.webp)

.png)

.avif)

.avif)

.avif)

.webp)

.avif)

.avif)

%2520(1).webp)

See DealRoom in Action

Discover why DealRoom is the best merges and acqusitions software for Corporate Development teams managing multiple deals. Simplify your M&A lifecycle, boost efficiency, and reduce friction — all in one platform.