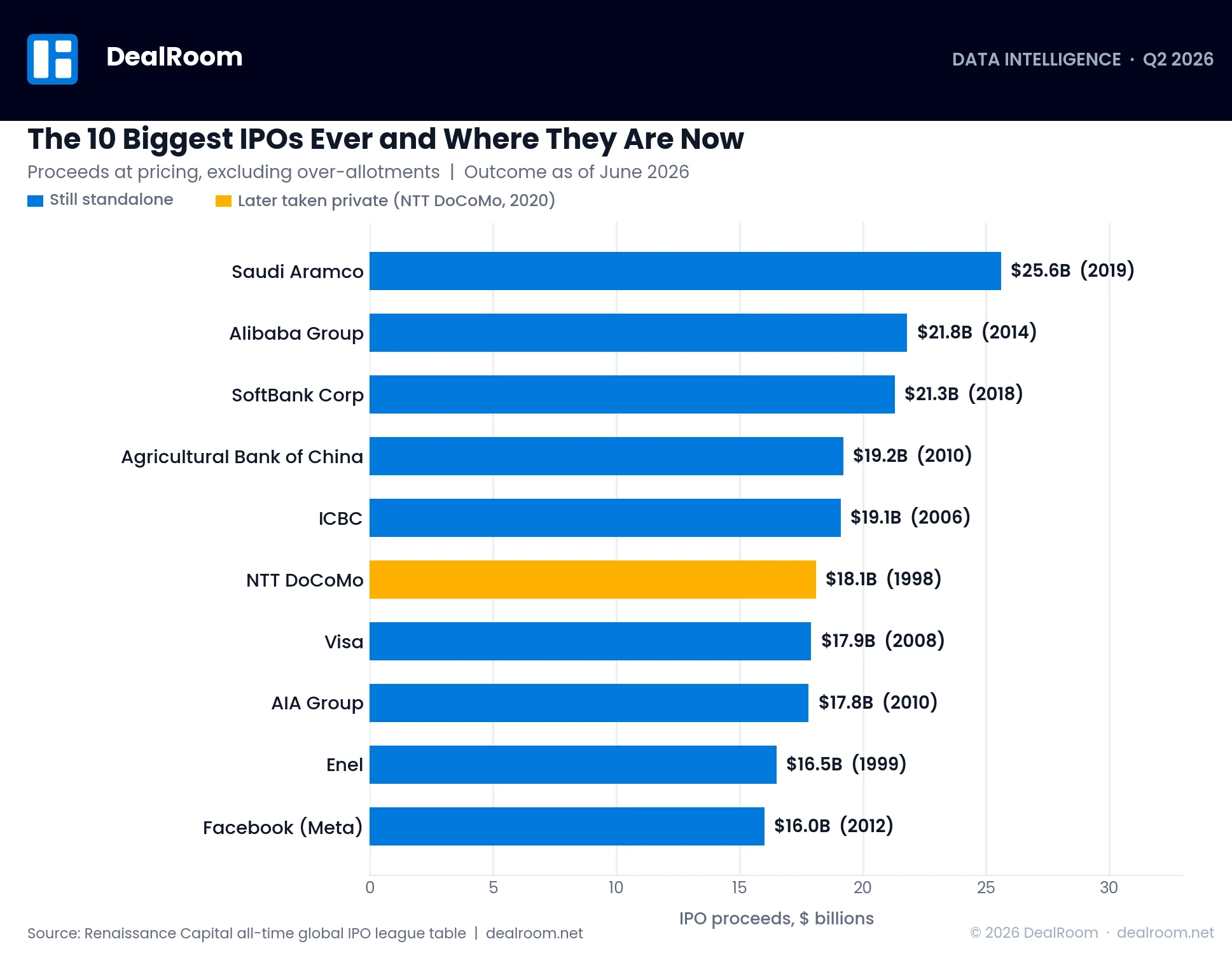

Medline raised $6.27 billion on the Nasdaq in December 2025, making it the largest IPO in the world for that year. It only qualified because it had exited first: bought by Blackstone, Carlyle and Hellman & Friedman in 2021 in a roughly $34 billion takeover including debt, only to return four years later as a public company. The IPO was effectively an M&A exit disguised as an IPO ticker.

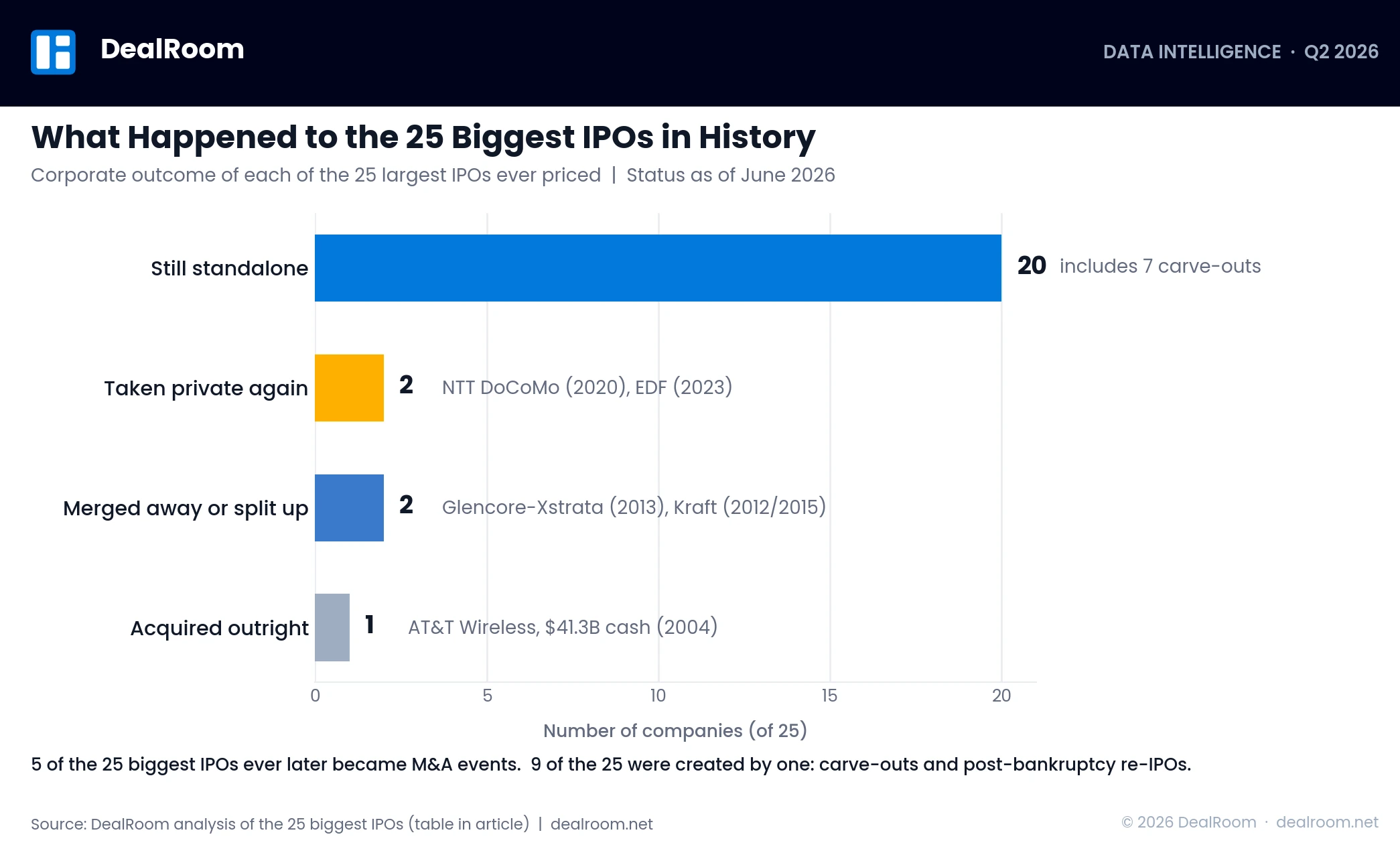

It's that revolving door we're now tracking on this page. We re-ranked the 25 largest IPOs of all time by price, verified those figures against Renaissance Capital's historical league table and original filings, then researched what happened to each company after its IPO day. Five out of the 25 would later become M&A deals themselves: two went private again, two were involved in megamergers or breakups and one was acquired outright for cash (numbers pulled from the table we verified below). Another nine existed as public companies only because of another transaction: a carve-out from a corporate parent, or a re-IPO following bankruptcy. You can find the full table with the deal stories behind it, below. We also explain what it all means for anyone screening the newest public companies.

I spent a decade as an M&A advisor before founding DealRoom. The first thing that work teaches you about IPOs: a listing is not an exit from the deal market. It is an entrance. Most of the companies on this list ended up back in our world, as buyers, as sellers or as both. Their deals run through the same pipelines our customers manage every day.

The 25 biggest IPOs of all time, ranked by proceeds

Proceeds figures: Renaissance Capital for every entry except the two combined dual listings, which follow contemporaneous reporting (ICBC, $19.1 billion across Hong Kong plus Shanghai; Agricultural Bank of China, $19.2 billion at pricing). Per-entry outcome sources are linked in the sections below. The combined 25 raised roughly $346 billion at pricing (sum of this table).

Five of the 25 became M&A deals themselves

Crunch the numbers in the outcome column and the pattern is clear: Of 25, 20 still trade as stand-alone companies, while five exited the market in the way that most companies eventually will: via transaction. Two were privatized by the parent or government that had taken them public. One was sold outright for cash. Two were transformed by megamergers to the point where the IPO-era company ceased to exist. The life stories of blockbuster IPOs resemble an M&A deal list with a built-in delay.

The take-privates: NTT DoCoMo and EDF

NTT DoCoMo's 1998 IPO was a $18.1 billion blockbuster, the largest in the world at the time. Fast forward 22 years, and its parent undid the IPO in one transaction: NTT made a ¥4.25 trillion ($40 billion) tender offer for the 34% of DoCoMo that it didn't already own in December 2020, Japan's largest-ever tender offer at a 40.5% premium. The company was delisted from the Tokyo Stock Exchange on December 25, 2020. The company that priced the biggest IPO of the 1990s would conclude its existence by facilitating an even larger M&A transaction.

EDF traced the same arc, with a government as purchaser. France privatized the utility in a 2005 IPO that raised $8.3 billion. The government reversed course during the energy crisis: it offered €9.7 billion at €12 a share to buy out minority investors in 2022, then finalized the squeeze-out on June 8, 2023. The French state was once again the sole shareholder. Eighteen years as a public company, and just like that, it’s gone.

Control was the driver in both transactions, not price. When a parent or anchor state already owns two thirds of a listed company it still pays a full takeover premium for the privilege of no longer having to share cash flows and strategy with the float. In our State of M&A report, we made a similar observation about the buy side in general: buyout funds controlled approximately $1.1 trillion of the $4 trillion in uncommitted private capital. Capital that concentrates doesn't leave cheap public companies untouched. Take-privates by sponsors, parents or governments are the destiny of any listing that markets stop valuing.

The acquisition: AT&T Wireless

AT&T Wireless garnered $10.6 billion in April 2000 with what was then the largest IPO in U.S. history. Four years later, Cingular Wireless acquired the company for $41.3 billion in cash at $15.00 a share. The deal closed on October 26, 2004. The largest IPO of its time became one of the largest all-cash takeovers of its time, in less than five years. For deal teams, the lesson remains: A record-setting IPO puts a price on an asset. It does not retire that asset from the market.

The megamergers: Glencore and Kraft

Glencore raised $10 billion in London and Hong Kong in May 2011, in part to establish currency for a merger it had its eye on. The stage was set two years later with the completed all-share merger of Xstrata on May 2, 2013, the largest mining deal ever. It later dropped the Hong Kong listing that it acquired in the IPO. The IPO was a stage in an M&A strategy, not the conclusion.

Kraft Foods has the entire corporate lifecycle summarized in one entry. Philip Morris spun-off Kraft as part of an IPO in June 2001. It consisted of 280 million shares at $31.00 each, totaling around $8.7 billion. Philip Morris wanted to raise money to pay off some of the debt it incurred while purchasing Nabisco. In 2012, Kraft split in two, becoming Mondelez International and Kraft Foods Group.

Kraft Foods Group would eventually go on to merge with 3G Capital and Berkshire Hathaway's Heinz. Kraft shareholders would own 49% of the combined company and receive a special dividend of $16.50 per share. The dividend was funded by a $10 billion injection of equity into Kraft by Berkshire Hathaway and 3G Capital. The merger concluded on July 2, 2015. Today, there is no company named Kraft Foods Inc. Its brands are split between two corporations, both formed through M&A.

Nine of the 25 were created by a deal in the first place

Exit outcomes are half the story. Consider how they reached the market in the first place, and the line between IPO and M&A becomes even less clear. Seven of the 25 were carve-outs of a corporate parent: NTT DoCoMo (NTT), SoftBank Corp (SoftBank Group), AIA (specialized from AIG as part of post-crisis restructuring), AT&T Wireless (ATT), Kraft (Philip Morris), LG Energy Solution (LG Chem) and Banco Santander Brasil (Santander). Two others were re-IPOs of companies rebuilt through restructuring. General Motors' 2010 listing enabled the US Treasury to begin divesting the 60.8% stake it completely exited in December 2013. Japan Airlines returned to the Tokyo Stock Exchange in 2012 two years after filing for bankruptcy. Nine of the 25 (count from table) had their listing day be also the closing day of a corporate transaction.

Today’s equivalent is the private equity round trip. SailPoint went public in 2017, was taken private in 2022 by Thoma Bravo for $6.9 billion, and went public again in February 2025 on Nasdaq, raising $1.38 billion. Medline did the same thing at ten times the size. Sponsor firms view the IPO market as just one of several exit windows they can open or close on a quarterly basis. If you’re doing deal flow predictions, this quarter’s mega-IPO class is next quarter’s target list, and the data room never stays closed for long. That’s why increasingly we see IPO-bound companies running their IPO out of the same data room platform they would for a sale process: the workstreams are almost identical.

The standalones are not standing still

The list of survivors even behaves as if it’s temporary. Meta completed its $21.8 billion acquisition of WhatsApp two years after its own IPO. The purchase price topped the money raised in the IPO. Visa was the largest US IPO ever when it priced, then used its IPO proceeds two years later to buy Visa Europe for €12.2 billion cash upfront and €6 billion+ of preferred stock and deferred payments. Alibaba broke up in six different ways in 2023, then abandoned its plans to spin-off its cloud unit when US chip sanctions altered the unit’s valuation. Rosneft’s London-listed GDRs were suspended in March 2022 after sanctions were imposed. Ending international ambitions its IPO was predicated on. Survival on this list isn’t guaranteed forever, just access to the deal market.

What deal teams should watch in newly public companies

Five of the largest listings of all time were eventually acquired. Lesson for corporate development: watch the IPO calendar like a sourcing feed. Here are the three signals you should care about most.

- Companies trading significantly below their offer price 12-24 months after IPO, like Rivian has, will have unhappy investors who anchored at a higher price and a board aware of the judgement of the public markets. MedPoint and SailPoint demonstrate how sponsors can arbitrage that gap. Strategics can do the same exercise. Run a screen of each year's IPO class and track the gap between offer price and current price.

- Expired lockups. Most IPOs have restrictions on insider selling for around 180 days. On lockup expiration, a concentrated holder (sponsor, founder, parent company) has an unlock event that creates a legal exit and a block trade is often the first step in a sale process. Mark your calendar.

- Stranded subsidiaries. Listed subsidiaries where the parent controls voting rights (the SoftBank Corp and LG Energy Solution structure), can simply be bought-back whenever the parent decides to change strategy, as NTT showed with DoCoMo. A small float is something that the parent could do but hasn't chosen to do so far.

We defined the strategic logic of much of this activity in our State of M&A report as transact to transform: companies acquiring to gain new capabilities rather than developing them in-house. Newly public companies are unusually attractive targets for that playbook because the S-1 and the roadshow did half of the diligence work for you. Teams that aggressively pursue those signals track them in a deal pipeline, not a watch list on a spreadsheet. They also come to the table prepared with a disciplined buy-side process before making the approach. If you’re looking forward rather than backward, check out our upcoming IPO tracker for deals still in the pipeline.

Frequently Asked Questions

What's the largest IPO of all time?

Saudi Aramco raised $25.6 billion at pricing with its December 2019 IPO on Tadawul, the largest ever. Total proceeds after exercise of the over-allotment option in January 2020 would rise to a record $29.4 billion.

How many of the largest IPOs were later M&As?

Five of the top 25 biggest IPOs ever were later M&A deals. NTT DoCoMo and EDF were privatized by parents/the French state. AT&T Wireless was sold to Cingular for $41.3 billion in cash. And Glencore and Kraft Foods were part of megamergers or breakups. The other 20 remained independent, listed companies.

What was the biggest company to be taken private following an IPO?

NTT DoCoMo. Parent company NTT paid roughly ¥4.25 trillion ($40 billion) in 2020 for the 34% of the company it didn't already own, the largest tender offer in Japanese history. DoCoMo was delisted from the Tokyo Stock Exchange in December 2020, 22 years after raising $18.1 billion in the largest IPO of the 1990s.

What is the biggest IPO on a US exchange?

The largest IPO on a US exchange is Alibaba's $21.8 billion NYSE debut in 2014. The largest IPO by a US company is Visa's $17.9 billion IPO on the NYSE in 2008.

Can a company IPO twice?

Yes. General Motors went public again on the NYSE in 2010 following bankruptcy. Japan Airlines relisted on the Tokyo Stock Exchange in 2012. SailPoint went public in 2017, was taken private by Thoma Bravo in 2022 and went public again in 2025. Medline's blockbuster 2025 IPO was preceded by a $34 billion take-private in 2021.

Why do parent companies delist their subsidiaries?

Delisting allows the parent company to take full control, instead of having to share profits with minority shareholders. It also cuts the costs and conflicts of being listed, and allows the parent to reallocate the subsidiary's capital and strategy however they want without public oversight. NTT said exactly this when they repurchased DoCoMo in 2020. France followed the same logic when they renationalized EDF in 2023.

Methodology

Rankings are based on IPO proceeds at pricing in US dollars and do not include greenshoe/allotment expansion shares unless noted by Renaissance Capital's all-time global IPO league table. Dual simultaneous tranche listings that priced as one deal (ICBC and Agricultural Bank of China, Hong Kong plus Shanghai) are aggregated per contemporaneous reporting.

Three corrections to the source table have been made: an entry for Hengshi Mining, which conflicted with reporting of that deal's size, has been removed as erroneous data; Alibaba's 2019 Hong Kong listing has been merged with the company's 2014 entry as another listing of the same company; the two tranches for Agricultural Bank have been merged.

Pre-1990s deals are not well represented by modern league tables: NTT's $1987 Tokyo IPO, which is approximately $5 billion smaller than DoCoMo's current record from Goldman Sachs' deal history, would rank among the top 12 but doesn't have a reliable primary dollar amount listed and is included here for reference rather than ranking. Installment-structured privatizations (Telstra's 1997 float raised A$14.2 billion in total instalments) and deals whose base size falls below the $8.0 billion cutoff once over-allotments are stripped (Porsche's 2022 listing of up to €9.4 billion) sit outside the table. Outcomes are classified as of June 2026 from the filings and announcements linked in each section. The headline counts (5 of 25 became M&A events; 9 of 25 were created by one) are derived from this table.

Key Takeaways

The IPO process is a maze of documents that require good IPO virtual data room services.

Talk to us in the near future if you are planning to go public through an IPO, as well as how DealRoom can assist your company to make the process as smooth as possible, as well as to attain the highest possible valuation when going public.

.png)

.png)

.avif)

.avif)

.avif)

.avif)