Guide to Mergers & Acquisitions: M&A Meaning, Types, Examples

Mergers and acquisitions (M&A) is the practice of combining companies through ownership change or strategic partnership. Globally, M&A activity reached $3.5 trillion across roughly 39,000 deals in 2024 (Bain Global M&A Report 2025), making it the largest single category of corporate transaction outside of an IPO.

M&A spans 6 transaction types (mergers, acquisitions, reverse mergers, joint ventures, strategic alliances, partnerships) and 12 distinct strategies (horizontal, vertical, concentric, conglomerate, product extension, market extension, bolt-on, tuck-in, roll-up, hostile takeover, capability acquisition, acquihire), each with different ownership structures, primary purposes, and risk profiles.

Below is a 5-question strategy quiz that matches your goal to one of the 12 standard M&A strategies that we built for those looking to learn more about M&A strategy:

Plus we built this searchable explorer of all 26 M&A concepts (transaction types, strategies, financing methods) with primary use, ownership impact, and named real-deal examples for each:

What are Mergers & Acquisitions (M&A)?

Mergers and acquisitions (M&A) is the process of combining two or more companies through various types of transactions. Despite the name, M&A encompasses more than just buying or selling a company. After all, there are other ways to combine companies together without any party giving up ownership. Let’s look at some of the most common types of M&A.

Different Types of Mergers & Acquisitions

Six transaction types define how M&A deals are structured. Mergers and acquisitions are the most common (combined entity or buyer-takes-ownership). Reverse mergers, joint ventures, strategic alliances, and partnerships are less common but widely used in specific contexts: reverse mergers as IPO alternatives, JVs for risk-sharing on new markets, alliances for technology co-development, and partnerships for long-term operating relationships.

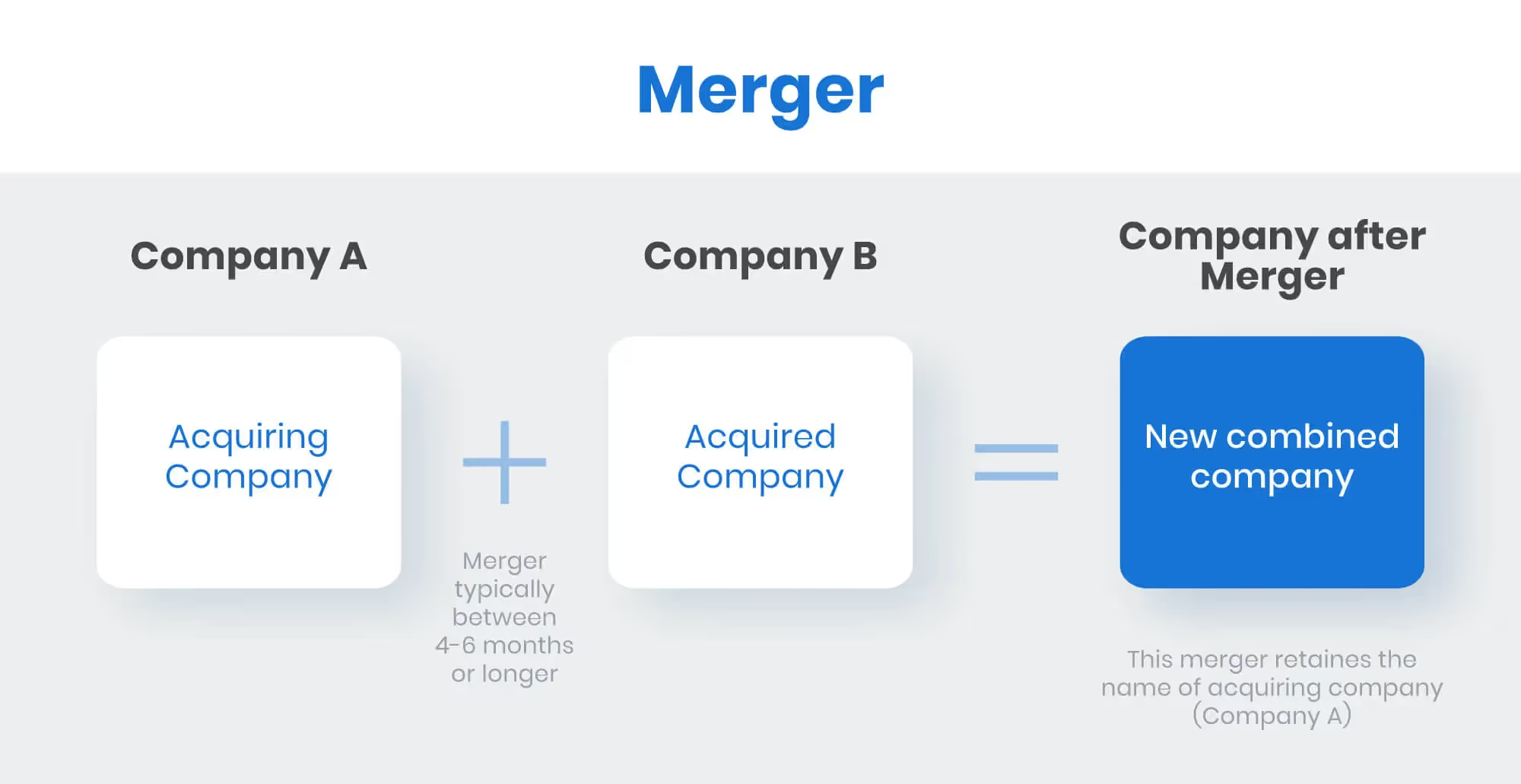

1. Mergers

A merger combines two companies of similar size into a single new entity, with shareholders of both companies receiving shares in the combined company. Mergers are mutual (both parties believe they will benefit) and most payment is via stock exchange rather than cash. The classic example: Exxon and Mobil combined to form ExxonMobil in 1998 in a $73 billion all-stock deal.

Unlike an acquisition, corporate mergers are mutual, and both parties feel they will benefit from the transaction. Typically, in a merger of equals, no massive cash payment is involved. Most of the payment is made through the stock exchange, where shareholders of both companies receive shares in the newly formed company in proportion to their existing shares.

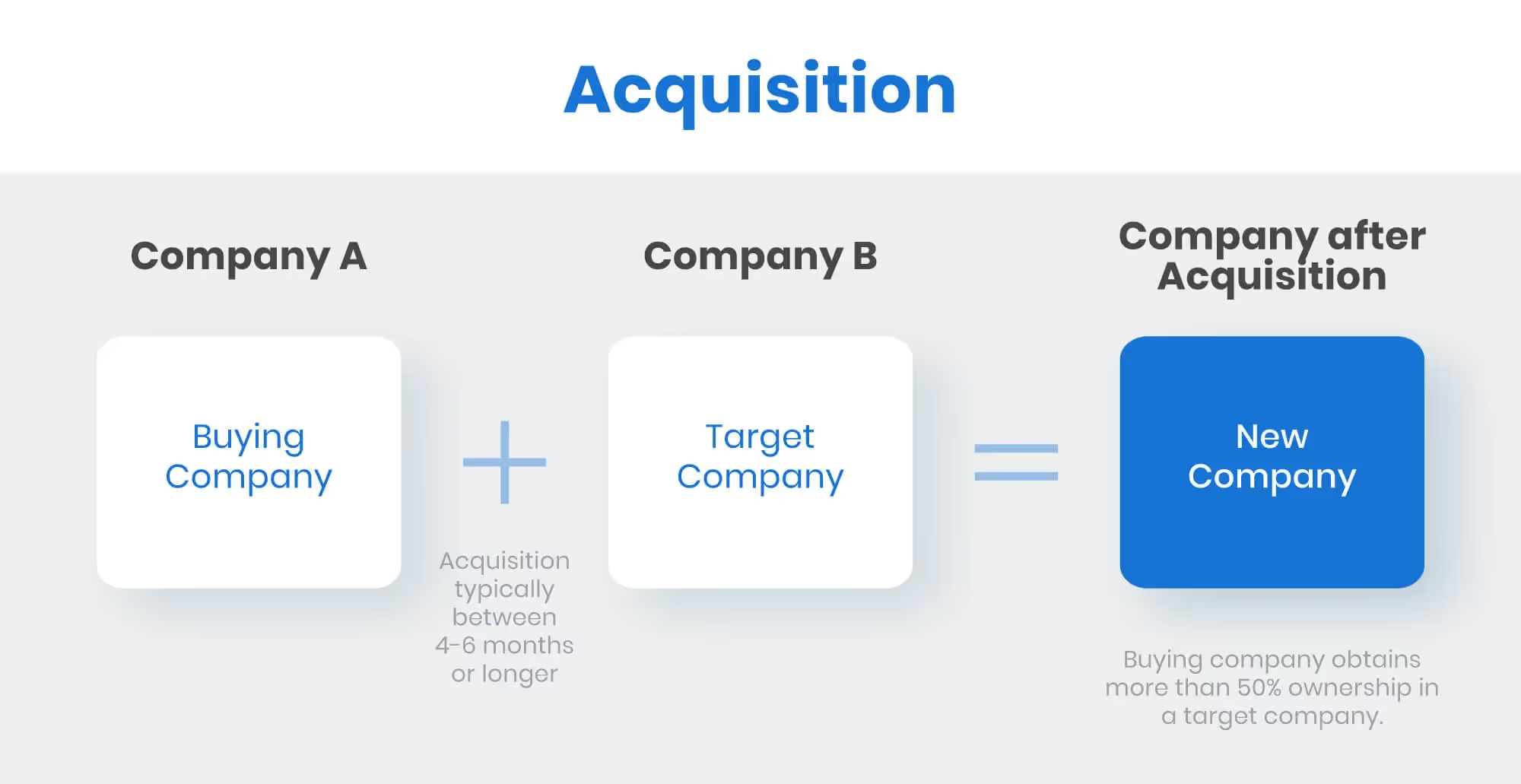

2. Acquisition

An acquisition is the purchase of an entire company or specific assets of a target company. The acquirer pays the seller (cash, stock, debt, or a combination) and takes ownership at close. Acquisitions are the most common form of M&A activity globally, accounting for the majority of the 39,000 deals announced in 2024. The classic example: Amazon's $13.7 billion acquisition of Whole Foods in 2017.

3. Reverse Merger

A reverse merger lets a private company become publicly traded by acquiring the majority of a public shell company's shares and merging with it. This is faster and cheaper than a traditional IPO (typically 3 to 6 months versus 12 to 18 months) but offers less price discovery and less marketing benefit than an IPO. Common examples include SPACs (Special Purpose Acquisition Companies) used during the 2020-2021 SPAC boom.

4. Joint Venture

A joint venture (JV) is a mutual agreement between two or more companies to create a new, separate entity that operates independently of the parent companies. JVs let both partners share investment, risk, and expertise without one acquiring the other. Sony and Ericsson formed Sony Ericsson in 2001 to combine consumer electronics expertise with telecommunications strength.

The perfect example of a joint venture is the agreement between Sony and Ericsson in 2001. They joined forces to create Sony Ericsson with the goal of dominating the mobile industry, leveraging Sony's expertise in consumer electronics and Ericsson’s strength in telecommunications.

5. Strategic Alliances

A strategic alliance is similar to a joint venture but does not form a separate entity. Both companies remain independent and collaborate on a specific project or capability. Toyota and Subaru's strategic alliance produced the Subaru BRZ and Toyota GT86 sports cars by combining Subaru's engine performance expertise with Toyota's manufacturing scale.

A very current and popular example of this is the agreement between Toyota and Subaru for the development of the Subaru BRZ and Toyota GT86. For these particular vehicles, they both leveraged Subaru’s expertise in engine performance and Toyota’s capabilities in manufacturing and design.

6. Partnerships

A partnership is a long-term business relationship sharing profits and liabilities, without forming a new entity and without a fixed end date. Partnerships are most common in professional services (law, accounting, consulting) where the partnership structure has tax and governance advantages over corporate forms.

The table below breaks down the various types of mergers and acquisitions, their primary purposes, the impact on ownership, and provides examples or use cases.

Different Types of M&A Strategies

Beyond the 6 transaction types, M&A is shaped by 12 standard strategies that determine which targets to pursue and what combination logic drives value. The 12 strategies fall into three rough groupings: industry-position strategies (horizontal, vertical, concentric, conglomerate, product extension, market extension) that define the relationship between buyer and target; acquisition tactics (bolt-on, tuck-in, roll-up) that define how a target is integrated; and specific deal patterns (hostile takeover, capability acquisition, acquihire) used in particular contexts.

M&A Deal Benchmarks: Size, Timeline, and Success Rates

The 39,000 M&A deals announced globally in 2024 ranged from sub-$10 million bolt-ons to $107 billion mega-deals, with the median middle-market transaction sized at $240 million. The full deal cycle from sourcing to signing runs 5 to 9 months for a typical middle-market deal; closing adds another 4 to 8 weeks for regulatory approvals.

Sources: Bain Global M&A Report 2025, McKinsey M&A practice research, Harvard Business Review M&A failure rate studies. "Failure" defined as deals that destroy shareholder value or fall short of synergy targets within 24 months.

1. Horizontal M&A

Horizontal M&A combines two competitors in the same industry and same stage of the supply chain. Drives consolidation, market share, and pricing power, but draws heavy antitrust scrutiny from the U.S. Department of Justice (DOJ) and Federal Trade Commission (FTC). Examples include Facebook acquiring Instagram (2012, $1B) and T-Mobile acquiring Sprint (2020, $26B).

2.Vertical M&A

Vertical M&A combines companies in different stages of the same supply chain (a buyer of inputs acquiring a supplier, or a manufacturer acquiring a distributor). Cuts costs, secures supply, and protects margin. Examples include a car manufacturer acquiring a seatbelt supplier or AT&T acquiring Time Warner (2018, $85B) to combine distribution with content.

3. Concentric M&A

Concentric M&A combines companies serving the same customer base with different products or services. Expands wallet share without requiring a market transition. A cell phone company merging with a phone case company is the textbook example.

4. Conglomerate M&A

Conglomerate M&A combines companies in unrelated industries. Used for diversification rather than operating synergy. Was a dominant strategy in the 1960s-1980s (GE, ITT, Berkshire Hathaway as exemplars) and has cycled out of favor as investors prefer focused operating companies. The deal stands or falls on the target's standalone performance.

5. Product Extension M&A

Product extension M&A combines companies selling related but different products in the same market. Builds out a category presence and lets the buyer cross-sell. The textbook example: a pencil manufacturer merging with an eraser producer.

6. Market Extension M&A

Market extension M&A combines companies selling the same products in different geographic markets or customer segments. Expands footprint without a product change. Common in cross-border deals: a U.S. company merging with a European distributor to gain access to EU markets.

7. Bolt-On Acquisitions

Bolt-on acquisitions are when a larger company buys a smaller business to extend an existing segment. The target often retains its brand and identity post-close. Common in private equity portfolio strategy where a PE firm runs 2 to 4 bolt-ons during a typical hold period to scale a platform company.

8. Tuck-In Acquisitions

Tuck-in acquisitions are similar to bolt-ons but the buyer fully absorbs the smaller business. The target's brand, leadership, and standalone identity all sunset; the team and technology integrate into the acquirer's existing operations. Common in tech acquisitions where the team and IP matter more than the brand.

9. Roll-Ups Acquisitions

Roll-up acquisitions (also called consolidation) involve acquiring multiple smaller companies in the same fragmented industry and merging them into a single, larger entity. Common in dental, HVAC, IT services, accounting, and other fragmented sectors where scale produces real cost or pricing advantages. Most roll-ups are PE-driven.

10. Hostile Takeover

A hostile takeover is an acquisition where the acquirer forces a public-company target to sell against management's wishes, typically through a tender offer or proxy fight. Only possible for public companies. Rare and expensive; usually driven by a dramatic valuation gap or a strategic threat the existing board refuses to address. Kraft's takeover of Cadbury (2010, $19B) is a recent example.

11. Capability Acquisitions

A capability acquisition is when a company acquires another specifically for its technology, intellectual property, or operational expertise that would take 18+ months to build internally. Common in tech and pharmaceuticals. Amazon acquired Kiva Systems for $775 million in 2012 to gain warehouse robotics technology.

12. Acquihire

An acquihire is an acquisition done mainly to bring the target's employees and leadership in-house, rather than to acquire its product, brand, or revenue. Common in tech, especially for engineering, ML, and product talent that is difficult to hire individually. The target's product is often shut down within 6 to 12 months post-acquisition.

The table below breaks down the various types of M&A strategies, their primary purpose, how they impact ownership, and examples or use cases.

| Strategy | Definition | Ownership / New Entity? | Primary Purpose | Example / Use Case |

|---|---|---|---|---|

| Horizontal M&A | Two competitors in the same industry and stage of the supply chain combine | No new entity necessarily | Increase market share, eliminate competition | Facebook acquiring Instagram |

| Vertical M&A | Companies from different stages of the same supply chain combine | No new entity necessarily | Control supply chain, reduce costs | Car company acquiring seatbelt supplier |

| Concentric M&A | Companies serving the same customers but with different products/services | No | Broaden the offering to the same customer base | Phone maker acquiring phone case maker |

| Conglomerate M&A | Companies from unrelated industries combine | No | Diversification, risk reduction | GE acquiring finance businesses |

| Product Extension M&A | Companies with related products in the same market combine | No | Expand product portfolio. | Pencil company merging with eraser producer |

| Market Extension M&A | Companies selling the same products in different markets combine | No | Geographic expansion | U.S. company merging with European distributor |

| Bolt-On Acquisition | Large company acquires a smaller business to add to an existing segment | A smaller company may keep its brand | Expand product line or market niche | Adobe acquiring SaaS plug-ins |

| Tuck-In Acquisition | A smaller company is fully absorbed into the buyer’s operations | Identity is lost | Integrate teams, tech, and customers | Google absorbing AI startups |

| Roll-Up (Consolidation) | The acquirer buys multiple small firms in a fragmented industry and merges them | Yes, or consolidated into the parent | Build scale and market power quickly | Private equity consolidating dental clinics |

| Hostile Takeover | Acquirer forces the target to sell against management’s wishes | No consent from the target | Gain control despite resistance | Kraft’s takeover of Cadbury |

| Capability Acquisition | The company acquires another primarily for its technology, IP, or skills | Usually absorbed | Gain missing expertise or innovation | Amazon acquiring Kiva Systems |

| Acquihire | Acquisition is mainly to bring in the target’s employees or leadership | Typically absorbed | Acquire talent quickly | Facebook acquiring app teams |

Why Companies Go for Mergers and Acquisitions

Companies pursue M&A for 5 standard reasons: synergies (cost reduction or revenue expansion from combining), market or geographic expansion, defensive plays (acquiring competitors or threats), capability acquisition (gaining technology, IP, or talent), and tax benefits (NOL utilization, basis step-up). Most deals justify themselves on a blend of two or three of these motives; deals that lean entirely on revenue synergies have the worst realization rates.

1. Synergies

Synergies describe the extra value generated when two companies combine, captured as either cost synergies (procurement consolidation, overhead elimination, real estate rationalization, IT consolidation) or revenue synergies (cross-selling, market expansion, pricing power). Cost synergies typically capture 70 to 85 percent of announced value within 18 months; revenue synergies capture only 25 to 35 percent.

a. Cost synergies – These are cost reductions incurred from combining the two entities. The most common example of this is economies of scale. Larger volumes will result in better discounts from suppliers.

b. Revenue synergies—These are additional sales or revenue that the combined entity will generate. The most common example is cross-selling to both companies' customers.

2. Expansion

Expansion is the second-most-common M&A motive: entering a new geographic market, customer segment, or product category faster than building it from scratch. The most common pattern is a U.S. company acquiring a European or Asian competitor to gain immediate market access rather than spending 3+ years building presence organically.

Consider a U.S. company seeking to enter the Asian market. Starting a business from scratch in a foreign country can be a more challenging process than acquiring an existing Asian company with an established presence in the target market.

3. Defensive Play

A defensive M&A play is when a company buys a competitor or potential threat to eliminate it from the market. Most famously, Google's $1.65 billion acquisition of YouTube in 2006 protected Google's digital advertising market by absorbing the fastest-growing online video platform before it could become a serious competitive threat.

One of the most famous M&A examples is Google's acquisition of YouTube in November 2006. YouTube was a fast-growing video-sharing platform starting to draw significant online traffic. Google saw this as a threat to its digital advertising market and decided to buy it for $1.65 billion.

This strategic move allowed Google to protect its advertising revenue and expand its presence in the online video market.

4. Capability

Capability-driven M&A is when an acquirer buys a target specifically for technology, IP, or operational know-how. Amazon's 2012 acquisition of Kiva Systems for $775 million is a textbook example: Amazon needed warehouse automation technology that would have taken years to develop internally, so it bought the leader in the space.

Amazon acquired them for $775 million to streamline its warehouse operations, reduce shipping times, and decrease costs through advanced robotics and automation technology.

5. Tax Benefits

Tax benefits can motivate M&A when the target offers tax-loss carryforwards (NOLs), asset-basis step-up opportunities, or favorable tax structuring. Section 382 of the Internal Revenue Code limits how much of an acquired company's NOLs can be used post-acquisition, but well-structured deals can capture meaningful tax value (typically 2 to 8 percent of deal value).

How Do Companies Finance Mergers and Acquisitions?

M&A deals are funded through 8 standard financing methods, often blended within a single transaction. Cash deals offer immediate certainty for sellers but reduce the buyer's liquidity; debt deals preserve cash but add leverage; stock deals dilute ownership but conserve cash; earnouts bridge valuation gaps. Most large deals use a mix of cash, debt, and either stock or earnout to balance these tradeoffs.

1. Cash

Cash is the most straightforward method for financing M&A deals. Using the company's cash reserves, the buyer pays the seller a specific amount in exchange for the company's ownership. This method is most appealing to the sellers because it offers immediate payment.

On the other hand, the acquiring company would want to hold on to their cash for as long as possible, unless interest rates are too high.

2. Debt Financing

Debt financing involves companies borrowing funds through bank loans, bonds, and other forms of debt to cover the costs of the transaction. They have several options for sources, including commercial and investment banking, private equity firms, and other financial institutions.

If interest rates are low, debt financing would be the company’s first option for utilizing its cash reserves in other investments and maximizing opportunities.

3. Seller Financing

There are also instances where the seller agrees to finance the transaction on behalf of the buyer. In short, the seller agrees to deferred payment in exchange for a slightly higher purchase price. This type of transaction requires a lot of trust between the buyer and seller.

4. Stock Payments

In this scenario, the buyer pays the seller using their company’s shares. This allows the buyer to acquire the target company without using cash or leveraging their balance sheet. This method can also be attractive to the seller if the acquirer’s stock has a high value and is expected to perform even better after the acquisition.

5. Earnouts

Whether it's used as a financing strategy or to bridge valuation gaps, earnouts simply mean the buyer agrees to pay a certain amount upfront and then additional payments based on the future performance of the business sold.

For instance, the seller is asking for $150 million for their company, and would not negotiate for anything less. The buyer can now employ an earn-out and agree to pay $120 million upfront, with the remaining $30 million subject to future performance.

6. Leveraged Buyouts (LBOs)

A leveraged buyout (LBO) is when an acquirer (typically a PE firm) buys a target using primarily borrowed money, secured by the target's assets and future cash flows. Buyer puts down a small amount of equity (typically 20 to 50 percent of purchase price) and finances the rest with debt. KKR's 1989 buyout of RJR Nabisco ($25 billion, classic LBO) anchors the playbook.

The investor uses the target company’s assets to secure the loans, and thus the target’s future cash flows to service the debt. In exchange, the buyer only puts down a small amount of equity. This enables firms to acquire control of other companies without incurring significant capital.

The high debt can also result in outsized returns on the small amount of capital at risk if the company performs well after the acquisition. KKR's buyout of RJR Nabisco is a classic example of an LBO: high leverage, high risk, and high potential returns.

7. Mezzanine Financing

Mezzanine financing is a source of capital between senior debt (the first layer of financing used to finance an acquisition) and equity in the deal. It's used to bridge the gap when a traditional loan isn't enough for the purchase price, enabling buyers to close the acquisition without additional equity. It’s treated like debt but may give the lender an equity interest if the borrower can't repay.

Due to its riskier position compared to senior debt, mezzanine financing has higher interest rates. However, it is popular in M&A transactions due to its ability to bridge funding gaps without immediate ownership dilution.

8. Asset-Based Financing

In asset-based financing, the buyer borrows money secured by the target company’s assets. The assets used as collateral can include equipment, inventory, receivables, or real estate. The maximum amount that can be borrowed depends on the quality and value of the assets in question.

Asset-based financing can be especially helpful in the acquisition of an asset-heavy company, such as a manufacturer, logistics company, or retailer, where the quality of assets provides a safety net and low risk for lenders.

The table below breaks down the types of M&A financing methods, how they work, and the advantages and disadvantages of each.

| Financing Type | How It Works | Advantages | Disadvantages |

|---|---|---|---|

| Cash | The buyer uses cash reserves to pay the seller directly | Immediate payment to seller; simple structure | Reduces buyer’s liquidity; less attractive if interest rates are low |

| Debt Financing | Borrowing funds via loans, bonds, or other debt instruments | Preserves cash reserves for other investments; favorable when interest rates are low | Increases debt load and interest obligations |

| Seller Financing | Seller finances the deal by allowing deferred payments | Reduces upfront cost for buyer; can ease negotiations | Requires strong trust between parties; seller bears financing risk |

| Stock Payments | Buyer pays using their company’s shares instead of cash | Preserves cash; appealing if the buyer’s stock is strong and expected to rise | Dilutes ownership; risky if stock value drops |

| Earnouts | Buyer pays part upfront and additional payments based on future performance | Bridges valuation gaps; reduces buyer’s risk | Can lead to disputes over performance metrics, delayed payment to the seller |

| Leveraged Buyouts (LBOs) | Buyer acquires the company mostly using borrowed funds secured by the target’s assets | High returns on small equity if the company performs well | High financial risk due to large debt; dependent on the company’s cash flow |

| Mezzanine Financing | A hybrid of debt and equity is used to bridge funding gaps | Bridges financing gaps without immediate equity dilution | Higher interest rates due to higher risk for lenders |

| Asset-Based Financing | Loans secured by the target company's physical assets | Useful for asset-heavy companies; low risk to lenders | Limited to the value and quality of available assets |

Tax Treatment of M&A Deals: Asset vs Stock vs Section 338

The tax structure of an M&A deal often matters more to the economics than the headline price. Three structural choices dominate U.S. M&A tax planning: asset purchases, stock purchases, and Section 338(h)(10) elections.

Asset purchase. The buyer purchases specific assets (and assumes specific liabilities) of the target. The buyer gets a stepped-up basis in the acquired assets, which lets the buyer depreciate or amortize them at the new (higher) tax basis. The seller typically pays both corporate-level and shareholder-level tax (double taxation) on the gain. Asset purchases are buyer-friendly and seller-unfriendly, but they let the buyer cherry-pick assets and exclude unwanted liabilities. Most common in middle-market deals where the seller is a passthrough entity (LLC or S-corp) with no entity-level tax.

Stock purchase. The buyer purchases shares of the target. The target's tax basis in its assets stays the same (no step-up). The seller typically pays only one level of tax (capital gains at the shareholder level). Stock purchases are seller-friendly and buyer-unfriendly. Most common in deals where the seller is a C-corporation with significant entity-level tax exposure.

Section 338(h)(10) election. A hybrid: the deal is legally structured as a stock purchase (clean for the seller) but is treated as an asset purchase for tax purposes (stepped-up basis for the buyer). Requires both buyer and seller agreement. Common in PE deals where the target is a corporate subsidiary; the seller (the parent corporation) is indifferent to tax treatment because consolidated returns wash out the difference.

NOL utilization. When the target has net operating losses (NOLs), Section 382 of the Internal Revenue Code limits how much can be used post-acquisition. The annual limit equals the equity value of the target multiplied by the long-term tax-exempt rate (currently around 4 percent), which can dramatically reduce the value of an NOL-heavy target.

Tax-free reorganizations. Certain stock-for-stock mergers can qualify as tax-free reorganizations under Sections 368(a)(1)(A) through 368(a)(1)(C). The target shareholders defer capital gains until they sell the buyer stock they received. Common in mergers of equals where both parties want a tax-deferred outcome.

Tax treatment is typically negotiated alongside price; a buyer offering an asset deal at $100 million may be matched by a competing buyer offering a stock deal at $112 million if the after-tax economics for the seller are equivalent.

Legal & Regulatory Considerations

Every M&A deal is subject to legal and regulatory scrutiny. In the United States, larger transactions require a Hart-Scott-Rodino (HSR) filing with the FTC and DOJ for antitrust review (typical threshold for 2025: deals over $119.5 million). Foreign-investment deals may also require CFIUS review for national-security concerns. The EU requires merger clearance for transactions above defined turnover thresholds. Cross-border deals often require approvals in multiple jurisdictions, adding 3 to 12 months to the timeline.

National and international regulators also scrutinize mergers and acquisitions. In the United States, for instance, larger transactions typically require a Hart-Scott-Rodino (HSR) filing with the Federal Trade Commission (FTC) and the Department of Justice (DOJ) for antitrust review. Foreign investment transactions may also be subject to a review by the Committee on Foreign Investment in the United States (CFIUS) on national security grounds.

In the European Union, transactions must be cleared with the EU Commission if they are expected to impact competition and may need to be GDPR compliant if personal data is transferred. Similar procedures are followed by antitrust and competition authorities in the UK, Canada, India, China, and other major jurisdictions.

Lawyers involved in an M&A transaction are typically responsible for its legal structure, drafting and negotiating purchase agreements, preparing and filing regulatory paperwork, and ensuring compliance with securities laws.

If the transaction spans multiple jurisdictions and/or involves sensitive industries such as healthcare, defense, and financial services, or public companies, the role of legal advisors becomes even more crucial. Thorough legal due diligence can help avoid post-closing lawsuits, integration issues, and regulatory fines or penalties, making it one of the most important phases of an acquisition.

M&A Antitrust Thresholds: When Regulatory Review Kicks In

Most M&A deals do not require antitrust filing. Filing thresholds protect small transactions from regulatory burden but capture every deal large enough to potentially affect market competition. Knowing the thresholds upfront determines whether you need 30 to 90 days of additional pre-close review.

U.S. Hart-Scott-Rodino (HSR) thresholds for 2025:

- Size of transaction test: Deals over $119.5 million require an HSR filing

- Size of person test: For deals between $119.5M and $478M, both parties must meet specific size thresholds (one party with at least $239M in assets or sales, and the other with at least $23.9M)

- Filing fee: $30,000 for deals between $119.5M and $173M; rises to $2.39 million for deals over $5.508 billion

- Waiting period: 30 days standard (15 days for cash tender offers); FTC or DOJ can issue a Second Request that extends review by 4 to 6 months

CFIUS (Committee on Foreign Investment in the United States):

- Voluntary in most cases but mandatory for certain critical-technology, critical-infrastructure, and sensitive personal data transactions involving foreign acquirers

- Review timeline: 45-day initial review plus 45-day investigation if needed, plus a possible 15-day extension

- Outcome options: clearance, mitigation agreement, blocked deal, or forced divestiture

EU Merger Regulation:

- Required if combined worldwide turnover exceeds EUR 5 billion AND each of at least two parties has EU turnover above EUR 250 million

- Review timeline: Phase I (25 working days) plus optional Phase II (90 working days)

- Increasingly the binding constraint for cross-Atlantic deals; EU has blocked or forced changes on multiple deals approved in the U.S.

UK Competition and Markets Authority (CMA):

- Voluntary system but mandatory in practice for deals affecting UK competition

- The UK CMA has become unusually aggressive post-Brexit, blocking or unwinding deals other regulators clear (notably Microsoft-Activision review)

Cross-border M&A typically triggers filings in 5 to 15 jurisdictions for large deals. Adding 6 to 12 months to the deal timeline for multi-jurisdiction reviews is now the norm for any deal over $5 billion.

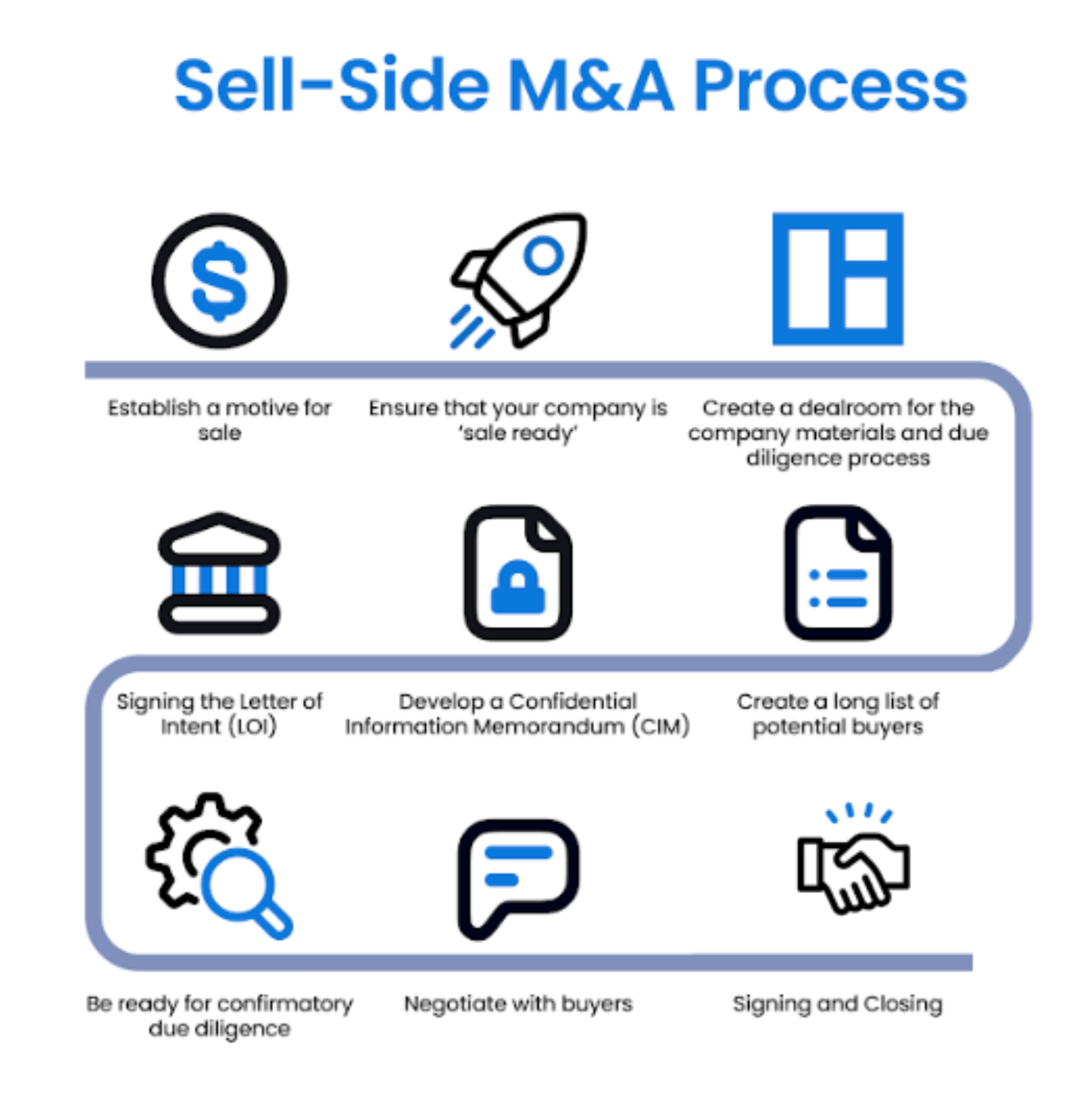

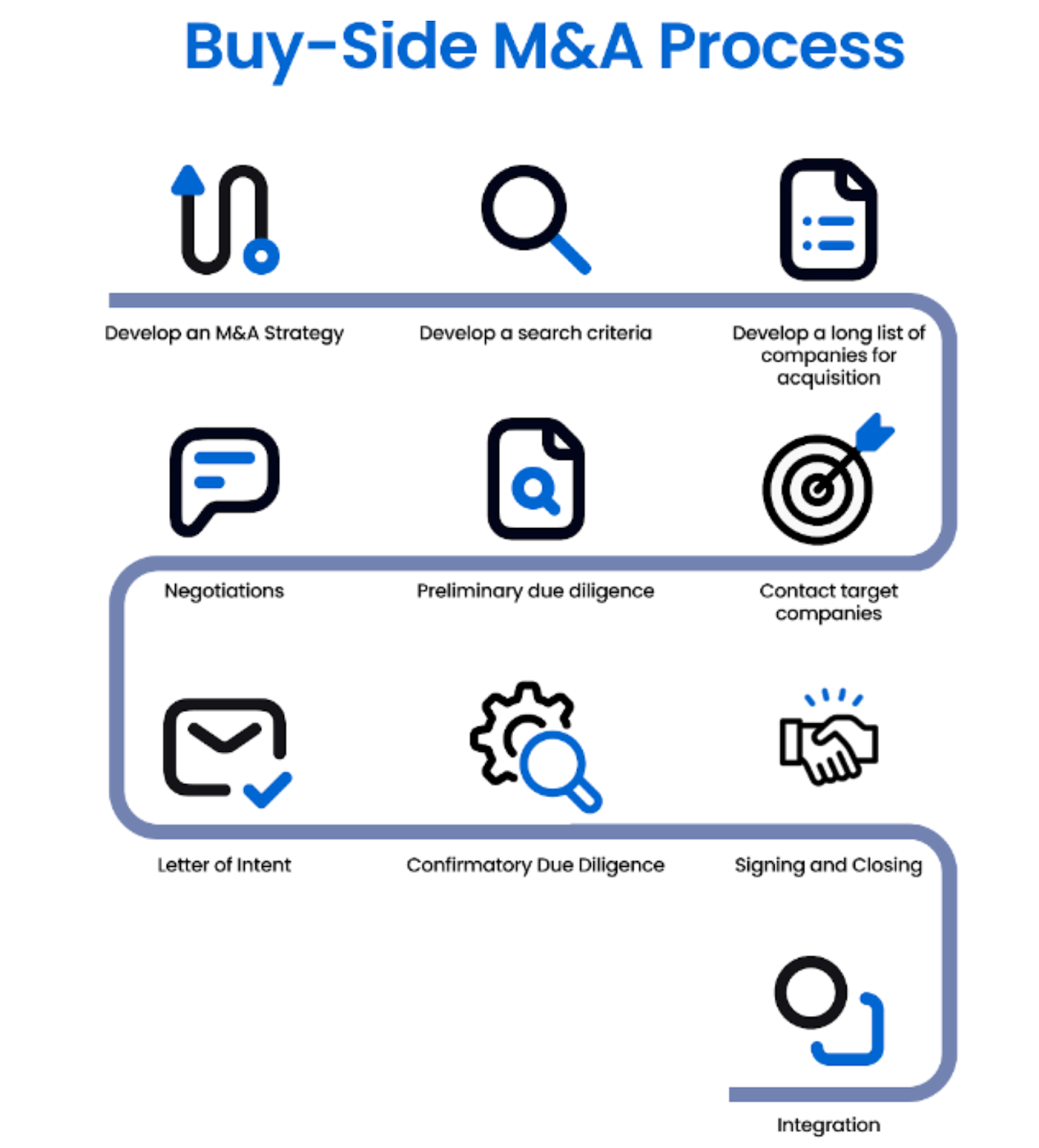

M&A Process Explained

The M&A process runs differently depending on which side of the deal you sit on. Sell-side processes focus on preparation, marketing, and negotiation to maximize price and certainty. Buy-side processes focus on strategy, sourcing, diligence, and integration. Both sides converge through Letter of Intent (LOI), confirmatory diligence, signing, and closing, but the work and incentives are distinct.

Sell-Side M&A Process Steps

- Establish a motive for sale

- Ensure that your company is ‘sale ready’

- Create DealRoom for the company materials and due diligence process

- Create a long list of potential buyers

- Develop a Confidential Information Memorandum (CIM)

- Signing the Letter of Intent (LOI)

- Be ready for confirmatory due diligence

- Negotiate with buyers

- Signing and Closing

Buy-Side M&A Process

- Develop an M&A Strategy

- Develop a search criteria

- Develop a long list of companies for acquisition

- Contact target companies

- Preliminary due diligence

- Negotiations

- Letter of Intent

- Confirmatory Due Diligence

- Signing and Closing

- Integration

M&A Advisor Roles: Who Does What in a Deal

A typical mid-to-large M&A deal involves 8 to 12 distinct advisor roles working in parallel for both buyer and seller. Understanding what each does (and what they do not do) helps companies scope advisor budgets and avoid coverage gaps.

Investment banker (M&A advisor). Runs the sell-side or buy-side process. On sell-side, banks identify potential buyers, draft the Confidential Information Memorandum (CIM), manage the auction process, and negotiate price. On buy-side, banks help source deals, prepare valuation materials, and provide a fairness opinion. Typical fees: 1 to 2 percent of deal value for sell-side, often with a fixed retainer plus success fee.

M&A lawyer. Drafts and negotiates the purchase agreement (SPA or APA), handles regulatory filings (HSR, CFIUS, foreign-investment), conducts legal due diligence on the target, and coordinates closing logistics. Typical fees: $1 million to $5 million on a middle-market deal, $5 million to $25+ million on a large deal.

Quality of Earnings (QoE) accountant. Conducts buy-side financial due diligence: normalizes EBITDA, identifies one-time items, and produces the QoE report that drives valuation refinement. Typically a Big 4 firm (Deloitte, PwC, EY, KPMG) or a boutique (Alvarez & Marsal, FTI). Typical fees: $300K to $1.5 million on a middle-market deal.

Tax advisor. Structures the deal for optimal tax treatment, models tax leakage, and advises on Section 338 elections, NOL utilization, and cross-border tax structuring. Often the same firm as the QoE accountant, or a separate boutique.

Sector consultant (commercial DD). Validates the target's market thesis: customer concentration, competitive positioning, market growth, win/loss patterns. Typical providers: McKinsey, BCG, Bain, L.E.K., or specialist boutiques. Typical fees: $250K to $2 million.

IT and cybersecurity advisor. Assesses the target's technology stack, system integration risks, and cybersecurity posture. Particularly important for tech acquisitions or any deal where IT integration is the synergy thesis.

HR consultant. Evaluates the target's organization, compensation, benefits, and culture; identifies key-talent retention risks. Often handled by the buyer's internal HR team plus an external comp specialist.

Insurance broker (R&W insurance). Brokers Representation and Warranty (R&W) insurance, which transfers the risk of seller breaches to a third-party insurer. Standard on most middle-market and larger deals; typical premium 2 to 4 percent of coverage limit.

Lender (debt financing). Provides senior or subordinated debt financing for leveraged transactions. Lender diligence runs in parallel to the buyer's, often using the same QoE report.

Environmental consultant. Conducts Phase I (and Phase II if needed) environmental site assessments. Mandatory for any acquisition involving real estate, manufacturing facilities, or known contamination history.

Real-World M&A Examples (with Lessons Learned)

The fastest way to learn what makes M&A succeed or fail is to study named historical deals. The successes share three traits: clear strategic fit, realistic synergy assumptions, and respect for the acquired company's culture. The failures share a different three: overpayment driven by competitive bidding, cultural misalignment, and inadequate integration planning. The four examples below cover both ends of that spectrum.

Successful Deals: Synergy & Strategic Fit

- Disney-Pixar (2006): Disney's $7.4 billion acquisition of Pixar in 2006 is one of the most-cited successful M&A deals in modern business. Disney granted Pixar creative independence in exchange for distribution and merchandising scale; animation revenue doubled within 3 years. New franchise opportunities (Toy Story sequels, Finding Dory, Inside Out) drove Disney's growth for the following 15 years.

- Facebook-Instagram (2012): Facebook's $1 billion acquisition of Instagram in 2012 is the highest-return acquisition in modern history. Instagram had only 13 employees at acquisition. Facebook let it run autonomously and added advertising infrastructure. Instagram now generates roughly $67 billion in annual revenue, accounting for nearly 40 percent of Meta's total revenue.

The key takeaway from these and other successful M&A deals is that strategic fit, synergy, and respect for the acquired company’s culture are what create value.

Deal Failures: Culture & Execution Breakdowns

- AOL-Time Warner (2000): AOL's $165 billion acquisition of Time Warner in 2000 is one of the largest value-destruction events in M&A history. AOL leadership believed traditional media and internet distribution would combine seamlessly. Cultures clashed, expectations were misaligned, and the dot-com bubble burst. The combined company destroyed over $200 billion in shareholder value within two years.

- Daimler-Chrysler (1998): Daimler's 1998 acquisition of Chrysler in a $36 billion "merger of equals" failed because Daimler treated Chrysler as a subsidiary rather than a partner. Misaligned values, conflicting leadership, and geographic distance led to poor collaboration and declining sales. Daimler sold Chrysler to Cerberus Capital Management for $7.4 billion in 2007, less than a decade after the merger.

The key takeaway from these failed M&A deals is that culture, leadership alignment, and integration planning are as important as financial logic.

These examples also highlight why tools like DealRoom’s M&A Platform exist: to prevent failures due to poor due diligence or integration.

M&A by Industry: Where Activity Is Concentrated

Global M&A activity is concentrated in a handful of industries that produce most of the deal value year after year. Understanding the industry distribution helps companies and advisors anchor expectations on what counts as a "normal" deal in their sector.

Technology and software consistently ranks #1 by deal volume, accounting for roughly 22 to 28 percent of global M&A in recent years. Tech M&A is dominated by capability acquisitions (companies buying AI, cybersecurity, or developer-tools startups), platform consolidation (PE firms rolling up vertical SaaS players), and acquihires (large platforms buying small teams for specialized talent).

Healthcare and life sciences runs second at 15 to 20 percent of global M&A. Pharma giants drive most of the dollar value through patent-extension acquisitions of biotech innovators. Healthcare services M&A (hospital consolidation, dental and vet roll-ups, ASC platforms) drives most of the deal count even though individual deal sizes are smaller.

Financial services is the third-largest sector at 10 to 15 percent of global M&A. Bank-bank deals have slowed since the 2008 crisis but specialty finance, fintech, insurance, and asset management continue to consolidate. Private equity is itself a large M&A consumer (the secondary buyout market alone runs $400 billion+ annually).

Industrial and manufacturing runs 8 to 12 percent, dominated by aerospace and defense, specialty chemicals, and capital equipment consolidation.

Energy and utilities runs 5 to 10 percent, cyclical with oil prices and transition policy changes.

Consumer and retail runs 8 to 12 percent, with food and beverage M&A particularly active as legacy CPG companies acquire emerging brands. Consumer tech M&A (streaming, gaming, e-commerce) overlaps with the technology sector.

The remaining roughly 25 percent splits across real estate, telecommunications, media, transportation, and other sectors. Cross-industry deals (a tech company acquiring a healthcare services platform, for example) are rare but increasingly common as digital transformation makes industry boundaries more porous.

M&A Risks & Challenges

M&A failures rarely come from a single mistake. They come from a series of compounding miscalculations across 6 risk categories: overvaluation and bad assumptions, cultural misalignment, integration complexity, regulatory and legal roadblocks, debt burden, and employee or customer disruption. Identifying these risks early gives M&A teams a chance to plan around them rather than discover them in year two.

Overvaluation and Bad Assumptions

Buyers often pay too much based on overly aggressive revenue forecasts or unrealistic synergy expectations that fail to materialize. Overconfidence, bidding wars, and the pressure to deploy capital may drive valuations above what a company can deliver post-acquisition.

Cultural Misalignment

Perfectly sound deals can fall apart due to differing work cultures. A clash in leadership style, communication practices, decision-making speed, or employee values can cause internal strife and talent loss (e.g., Daimler-Chrysler).

Integration Complexity

Integration of IT systems, processes, legal entities, and teams is more challenging than most projections anticipate. Without a well-defined and effectively executed post-merger integration (PMI) plan that encompasses HR, finance, IT, sales, and operations, anticipated synergies are often delayed or lost. This is where using a tool like DealRoom’s M&A Platform can help to keep workstreams aligned and on time.

Regulatory and Legal Roadblocks

Antitrust issues, national security reviews (e.g., CFIUS in the U.S.), industry-specific regulations, or international legal discrepancies can delay or derail a transaction. Lengthy regulatory processes increase transaction costs and uncertainty, and mandatory divestitures can alter the deal’s structure.

Debt Burden and Financial Risk

In leveraged transactions, excessive debt levels put pressure on cash flows. If the business experiences a downturn in revenue or if synergies do not materialize as quickly as expected, the company might face difficulties in servicing its debt, potentially leading to restructuring or bankruptcy.

Employee Uncertainty and Customer Disruption

Unclear communication during a deal can lead to employee churn, lower morale, and customer attrition, while competitors are poised to capitalize on the disruption to poach clients or talent.

Most risks don’t materialize after the deal; they’re built in from the beginning, when strategy, valuation, and integration planning are still being developed. Teams that plan for these challenges upfront and treat integration as part of the deal, rather than an afterthought, are the ones that win and capture value time and time again.

Frequently Asked Questions

What is the difference between a merger and an acquisition?

A merger combines two companies of similar size into a single new entity, with shareholders of both companies receiving shares in the combined company. An acquisition is the purchase of a target company or its assets by an acquirer; the buyer takes ownership and the seller is paid. Mergers are mutual; acquisitions can be friendly or hostile. The terms are often used interchangeably (M&A) but the structures differ.

What are the 4 main types of M&A?

The four most common M&A types are: horizontal (combining direct competitors), vertical (combining different stages of the same supply chain), conglomerate (combining unrelated businesses), and concentric (combining companies serving the same customers with different products). Beyond these, M&A includes joint ventures, strategic alliances, partnerships, bolt-ons, tuck-ins, roll-ups, hostile takeovers, capability acquisitions, and acquihires.

How long does an M&A deal take?

A typical middle-market M&A deal runs 5 to 9 months from sourcing to signing, plus another 4 to 8 weeks for regulatory approvals before closing. Sourcing and screening take 2 to 3 months, due diligence runs 2 to 3 months, negotiation and SPA drafting take 1 to 2 months. Mega-deals over $5 billion typically run 12 to 18 months due to multi-jurisdiction antitrust reviews.

What percentage of M&A deals fail?

Roughly 50 to 70 percent of M&A deals destroy shareholder value or fail to meet announced synergy targets within 24 months, according to McKinsey, BCG, and Harvard Business Review research. The most common causes are overpayment, cultural misalignment, and inadequate post-close integration planning.

What is the largest M&A deal in history?

Vodafone's 1999 acquisition of Mannesmann for approximately $202 billion remains the largest M&A deal in nominal terms. Adjusted for inflation, AOL's 2000 acquisition of Time Warner ($165 billion at the time, equivalent to roughly $300 billion today) is often cited as the largest. Both are also among the worst-performing deals in history.

What does M&A stand for?

M&A stands for mergers and acquisitions. The abbreviation refers collectively to the corporate finance practice of combining companies through ownership change (mergers, acquisitions) or strategic partnership (joint ventures, alliances, partnerships).

What is the typical M&A deal size?

The median middle-market M&A deal is approximately $240 million in 2024. Deal sizes range from sub-$10 million (small bolt-ons) to over $100 billion (mega-deals). The largest single deal in 2024 was approximately $107 billion. Roughly 60 percent of all global M&A deals fall under $250 million in enterprise value.

DealRoom’s M&A Platform offers due diligence and project management capabilities designed to address the many challenges in M&A. It should be considered a critical element of the process by any company undertaking agile M&A.

.avif)

Get your M&A process in order. Use DealRoom as a single source of truth and align your team.