A letter of intent (LOI) is a succinct summary of an M&A transaction.

Usually written by the buy-side, the LOI clearly outlines what is being acquired, for how much, by whom, in what timeframe, and under what terms and conditions.

Every transaction has an LOI, so it’s important for anyone conducing M&A to know how to maximize their potential.

In this article, we at DealRoom give the run down on Letters of Intent, and how to write them and include some samples in the end.

What is an M&A letter of intent (LOI)?

An M&A letter of intent or LOI is a document that outlines one or more parties to undertake an M&A transaction. The receipt of an LOI is the first time in the M&A process that the buyer’s interest has been formalized, expressing in written form their intentions for the transaction.

Typically, the LOI will include purchase price and terms, the assets and liabilities included in the deal, exclusivity, and the conditions required to close the transaction.

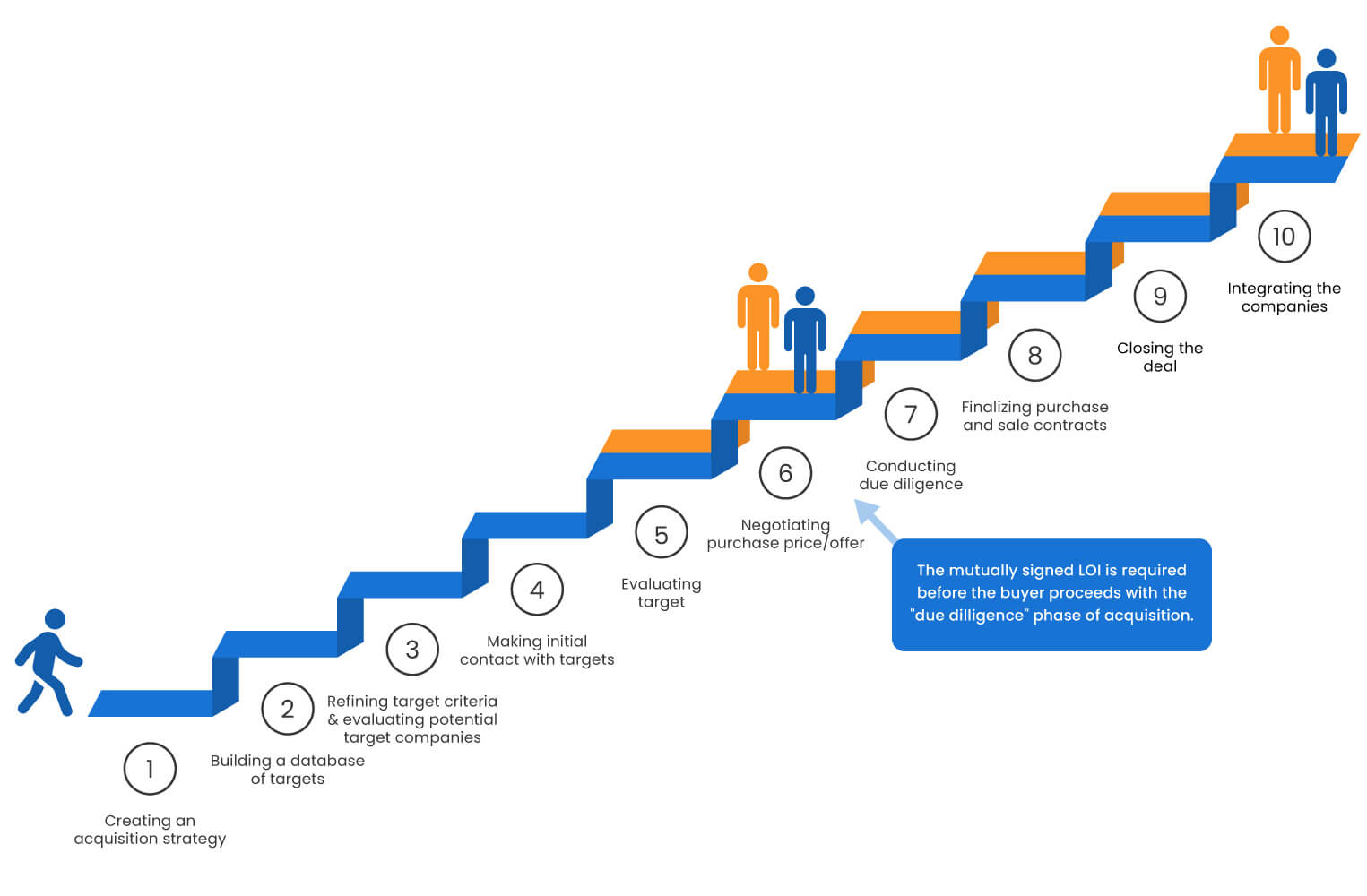

If accepted by the sell-side, the LOI is immediately followed by the due diligence phase of the transaction.

Why to use an LOI

Use of an LOI is considered good practice by everybody in the M&A industry. It also endows the process with clarity and transparency.

Until the LOI, the process will have consisted of conversations, some sharing of documents, and some limited exploration of the company being discussed.

The LOI is the doorway to achieve more. It shows the seller that the buyer is acting in good faith and has spent time putting constructing the terms of a deal.

Crucially, the LOI creates a line in the sand:

If the seller accepts the terms outlined in the LOI, the buyer will be given clearance to begin due diligence. If the terms are not accepted, the two sides can begin negotiations on the sticking points.

If these can be ironed out, they return to a ‘final’ version of the LOI, both parties sign-off and due diligence begins in earnest. Thus, the LOI represents an important inflection point in a deal’s evolution.

.jpeg)

How to write an LOI

Letters of intent generally run to 2-3 pages, are concise and direct (summarize text if needed), while maintaining a degree of decorum.

The LOI should strike a balance between formal business writing and writing a polite letter to a counterparty, that doesn’t appear to be overly hostile or aggressive.

Ultimately, the document should convince its reader that they’re receiving a good deal, and show that the bearer is someone that they should be happy to do business with.

The format should run something like the following:

%20structure%20for%20M%26A%20deals.jpeg)

1. Introduction

The beginning of the letter sets out in general terms the aim of the LOI, and usually, the context of how the business being acquired fits strategically with your own. The introduction should also set forth that the LOI is non-binding.

This is a general understanding of LOIs, but there is some gray area among attorneys on this point, so it’s better to underline this at the beginning.

2. Deal Structure

As the most important part of the LOI, the deal structure directly follows the brief introduction. The wording of this part may require assistance from a legal expert if the structure is more complicated than a straight 100% takeover.

Crucially, this section should also include how payment is made and when (for example, in installments, based on revenue, etc.)

An important component of this is the terms around accounts receivable. You’re buying the business partly on the basis of its current assets.

In the case of receivables, you’re not sure if they’ll be paid, so you have to make a provision for this in the LOI.

The nature of such provisions will depend on the size of the receivables in monetary terms, and to the successful operation of the business in the short-term.

Where the owner(s) of the acquired business will remain in the business, the terms of their employment may also be outlined in this section.

This should be clear but non-confrontational. The seller should feel that they stand to benefit from the acquisition and not that they’re being coerced into the new set of arrangements.

As with any other employment contract, this should include some incentives for the management team and outline the difference their contribution will make.

This would typically include some equity benefits in the new company and perhaps improved working conditions such as reduced working hours.

3. Indemnification Obligations

The courteous tone of the previous section is especially important, as it’s followed by the seller’s indemnity obligations.

This section, arguably the second most important after the deal structure, sets out your recourse in the event of the circumstances of the business suffering a significant deterioration in the aftermath of the deal.

The scope of indemnities are covered well elsewhere, but suffice to say that these are thought of in terms of ‘caps’ and ‘baskets.’

Caps set the limit in dollar terms of what the seller owes the buyer in the event of such a deterioration. Baskets provide the seller with some cover on how much losses are allowed before compensation to the buyer kicks in.

4. Transaction Closing Conditions

The closing conditions are usually composed of regulatory and financial conditions that must be met before the transaction can close.

For example, a takeover could be subject to some form of regulatory approval (this would be typical in the case of a foreign buyer looking to acquire a US telecoms company) or the buyer obtaining sufficient financing from their 3rd party lender.

You should now have a document (in letter form) which will serve as a roadmap for the deal.

Although it’s technically non-binding, the idea is that it’s written in good faith. To dramatically change anything within it jeopardizes the chances of the deal closing.

Once sent over to the seller’s side, it will also serve as the basis for your negotiations.

"In our preliminary non-binding bid, we have a long list of assumptions. One of the assumptions is that all third party contracts are at or near their historical costs and fee levels. That's gonna impact your underlying valuation if you come in and you're paying 25% more on a large third party contract."

Speaker: Keith Crawford, Global Head of Corporate Development, State Street Corporation

Shared at The Buyer-Led M&A™ Summit (watch the entire summit for free here)

Download free letter of intent (LOI) samples

Form of LOI - Equity Acquisition

Form of LOI - Asset Acquisition

How to Negotiate a LOI

Some negotiation is expected in the LOI.

Even after the buy-side and sell-side have discussed a deal in detail, it’s common that the LOI includes at least some issues which won’t have been detailed before.

While the major numbers will generally be known in advance, the smaller clauses and conditions are unlikely to have been covered.

Issues which the seller is likely to contest include:

- The time periods mentioned (e.g., payment times, length of gardening leave, consultation periods, etc).

- Conditions of payment (e.g., a certain percentage of the transaction being paid based on a future metric being achieved).

- Issues around working capital, and how much is considered ‘normal’ as part of the transaction.

- Issues around basket indemnity and cap indemnity.

- Length and scope of the due diligence being proposed.

- Size of the deposit (In some cases, particularly in smaller transactions, the buyer may pay a percentage of the final deal upfront as a sign of goodwill. This is not refundable if the deal is not concluded).

Conclusion

The writing of the letter of intent represents the moment at which a buyer moves from being a ‘tyre kicker’ to a serious buyer.

A well-written LOI should crystallize the transaction in under three pages. That makes its drafting important for both sides of the transaction.

By creating a clear, concise, and transparent letter of intent, the buyer not only fully outlines their intentions to the seller, but also brings clarity to their own perspective on the deal.

This is why an LOI is an important component of any deal, and demands your attention.

.jpeg)

.jpeg)