Imagine you’re about to buy your dream home. You’ve done your initial research, the neighborhood seems great, and the price is reasonable. But just before signing the dotted line, you decide to have an inspector check the foundation and he finds cracks that could cost you a fortune down the road. That’s the essence of financial due diligence in M&A transactions: uncovering what lies beneath the surface to make an informed decision.

At DealRoom, we’ve worked with countless investment bankers, law firms, and M&A brokers who’ve shared stories of financial due diligence, making or breaking deals. They agree - understanding a company’s financial performance and what drives its numbers is crucial to success.

Let’s dive into how to conduct financial due diligence with real-life examples, and we’ll provide a handy due diligence checklist to guide you through the process.

What is Financial due diligence?

Think of financial due diligence as a deep investigation into a company’s financial statements—its income statement, balance sheet, and cash flow reports. While an audit verifies the accuracy of these documents, financial due diligence goes beyond. It's about asking questions like, "Are the numbers sustainable?" and "What are the hidden liabilities?"

For example, consider a small tech startup with impressive revenue growth. Everything looks solid at first glance, but financial due diligence reveals that a single large client accounts for 60% of their sales. What happens if that client leaves? This is the kind of insight you gain through financial due diligence—understanding the true quality of earnings.

Buy-side financial due diligence

When we think of financial due diligence in an M&A transaction, we’re typically thinking about due diligence from the buy-side perspective.

Now, picture this: you're on the buy-side of an M&A transaction, preparing to acquire a growing e-commerce business. Everything looks good on paper. The revenue is strong, profits are steady, and they have a loyal customer base. But, during the financial due diligence process, you discover that the company’s growth has been fueled by heavy discounts and promotional pricing. Their EBITDA (earnings before interest, taxes, depreciation, and amortization.) looks inflated because they’ve been sacrificing margins for volume.

In this case, buy-side financial due diligence has saved you from overvaluing the company. You realize that after the acquisition, sustaining that growth without compromising profit margins will be a challenge.

Read more: How to Efficiently Conduct Buy-Side Due Diligence

Sell-side financial due diligence

Despite the tendency to think of financial due diligence as a buy-side practice, there is also a need for the sell-side in a transaction to conduct its own financial due diligence.

On the sell-side, imagine you're the CFO of a manufacturing company about to go up for sale. You’re preparing your financial statements for potential buyers. Through your own financial due diligence, you uncover some underutilized assets - an old warehouse that’s no longer in use and some outdated machinery. Highlighting these assets’ potential value in the sale boosts your company’s valuation, giving you a stronger negotiating position.

This proactive approach to financial due diligence not only attracts more interest from buyers but also ensures you’re not caught off guard during negotiations. This can also serve as a form of internal audit, helping to uncover issues that would otherwise have gone unchecked.

Read more: How to Efficiently Conduct Sell-Side Due Diligence

Understanding the importance of financial due diligence

Financial due diligence should be at the core of the due diligence process, because every other element of the business you’re analyzing will affect financial due diligence in some way.

Need investment in operations? That will affect financials.

The company is facing an upcoming legal dispute? That’s likely to cost you.

The target needs new management? Looks like you’re going to be paying redundancy soon.

Thus, whether the due diligence you’re undertaking is operational, legal or human resources, as in the cases above, or any other area of due diligence, it pays to keep costs in mind.

And while the checklist we provide below is strictly concerned with the explicit financial elements of the target company, every kind of due diligence is in some way financial.

The question, ‘what are the hidden costs here?’ is the essence of what the process is all about.

Difference between audit and due diligence

Audits are like following a recipe exactly. Every number on the balance sheet and every transaction is accounted for, ensuring compliance. Due diligence, on the other hand, is more like taste-testing along the way to see if the dish needs more seasoning. It involves evaluating the company’s future potential and uncovering risks that might not be evident through standard financial reporting.

For example, during an audit, everything might seem fine. But during financial due diligence, you discover the company has been delaying maintenance on critical equipment to improve short-term profits. That’s a red flag you wouldn't catch in a routine audit.

How long does financial due diligence take?

The time frame for financial due diligence can vary based on the complexity of the target company. A relatively simple acquisition might take 2–6 weeks, while larger M&A transactions could take longer.

For instance, if you’re acquiring a private equity-backed healthcare company, you’ll likely need more time to go through their regulatory filings, tax due diligence report, and legal compliance compared to a smaller tech startup with straightforward financials.

Financial due diligence in M&A transactions

In M&A, financial due diligence helps uncover the true financial health of a company. It starts with reviewing financial statements—the income statement, balance sheet, and cash flow—to assess the accuracy and sustainability of earnings. Next, working capital, debts, and hidden liabilities are evaluated to ensure the company can meet its obligations. Key financial ratios are compared to industry standards, and tax due diligence checks for compliance. Finally, you look for any signs of fraud or non-compliance, giving a full picture of the company’s financial stability before making a decision.

The financial due diligence checklist

When conducting financial due diligence, you and your team should approach the process like an audit committee, thoroughly analyzing every aspect of the company’s financial health. The process generally begins with a review of five years of financial statements, including 10-K filings, 10-Q filings, and proxy filings in the U.S.

1. Income Statement (past five years)

- Look for volatility in earnings over time. If earnings are inconsistent, investigate the underlying causes and assess whether this volatility is likely to continue in the future.

- Scrutinize expenses for any irregularities. For example, are salaries increasing faster than revenue? Or are marketing expenses not reflected in rising revenues?

- Evaluate the quality of earnings. Are revenue figures driven by a single large client, or is the customer base diversified? If a key client leaves, will the company suffer a major revenue loss, or does it have a stable, growing client base?

- Watch for exceptional items. Sellers often highlight one-off events that affect operating income, like a factory shutdown due to a strike. Ask yourself: is this truly an extraordinary event, or something that could happen again within a five-year period?

2. Balance Sheets (past five years)

- Assess the company’s marketable assets—those that could be easily sold. Are these assets likely to fetch more or less than their current value on the balance sheet?

- Review other valuable assets not used in daily operations, such as patents or unused property. These assets could present hidden value in the transaction.

- Pay close attention to the debt-equity ratio. Compare it against your own company’s ratio and the industry standard. Ideally, the target company should carry less debt than your own firm.

3. Balance Sheets (past five years)

- Focus on how much cash the company is generating annually, after accounting for all financing and investing expenses. If cash flow is consistently close to zero, investigate the reason.

- Assess the quality of cash flows. Are positive cash flows driven by operational growth, or is the company selling off assets to maintain liquidity?

- Conduct sensitivity analysis. If the company’s operating cash flow were to drop by 30%—say, due to the loss of a major client—would it still be able to cover its loan interest payments?

4. Financial Ratios and Health Dashboard

- Use the financial statements to calculate key financial ratios over the last five years, creating a comprehensive view of the company’s financial health. At a minimum, this should include:some text

- Operating margin

- Gross margin

- Interest coverage

- Profit margin

- Current ratio

- Debt ratio

- Debt-to-equity ratio

- Asset turnover

- Return on assets

- Return on equity

- Benchmark these ratios against industry standards. For example, if the company’s operating margin is well below the industry average, this could indicate operational inefficiencies.

5. Management Discussion and Analysis (MD&A)

Review these filings to assess the quality of the financial statements. The MD&A can often provide insights into the reasons behind financial trends and may raise new questions for your team to investigate.

6. Tax Due Diligence

Tax due diligence is a critical aspect that warrants its own checklist. Be sure to review tax filings and compliance to uncover any potential liabilities. DealRoom provides a comprehensive checklist for this part of the process.

7. Fraud Detection

Throughout the due diligence process, keep an eye out for signs of fraud. Common types include:some text

- Asset misappropriation: This involves employees enriching themselves through false invoicing, skimming, or similar tactics.

- Financial statement fraud: Inflating assets or hiding liabilities is a common form of this. Even audited financial statements may not catch these issues, so thorough review is key.

- Corruption: This could range from vague transaction descriptions to misaligned payment records. Be on alert for red flags in these areas.

It’s crucial to ask the right questions. For example, inquire about:

- Complex business arrangements or unusual transactions.

- End-of-quarter transactions that seem out of the ordinary.

- Changes in auditors and the reasons behind those changes.

- Significant growth over a short period and the factors driving it.

- Non-intuitive changes, such as receivables growing faster than revenue.

- Adjustments in accounting practices.

- Insider sales of stock.

Thorough and detailed financial due diligence will reveal the true financial health of the target company, enabling better decision-making and reducing the risk of future surprises. Always ask questions and don't hesitate to dig deeper if something doesn’t seem right.

“Time pressure drives data quality problems. You can’t fix one without the other.”

- Matt Melsen

Shared at The Buyer-Led M&A™ Summit (watch the entire summit for free here)

Frequently Asked Questions

What is financial due diligence?

Financial due diligence is a detailed review of a company’s financial records before an investment, merger, or acquisition. It helps buyers confirm that the target’s financial performance, assets, and liabilities are accurate and reliable.

What is the main purpose of financial due diligence?

The purpose is to verify the financial health of a business. It helps investors assess whether the reported earnings, cash flow, and balance sheet figures reflect the company’s true value and risk profile.

How do you conduct financial due diligence?

Start by gathering financial statements for the past three to five years, review revenue streams, margins, and expenses, and check for consistency between financial reports and tax filings. Also analyze debt, working capital, and future cash flow projections.

What documents are needed for financial due diligence?

You’ll need audited financial statements, management accounts, tax returns, debt agreements, customer contracts, and forecasts. These records allow buyers to test accuracy and spot potential red flags.

Who conducts financial due diligence?

Due diligence is typically carried out by financial analysts, accountants, or advisory firms on behalf of investors, private equity funds, or corporate acquirers.

How long does financial due diligence take?

The process usually takes between two and six weeks, depending on company size, data availability, and deal complexity.

What is the difference between financial and legal due diligence?

Financial due diligence focuses on financial performance, accounting accuracy, and future projections. Legal due diligence examines ownership, contracts, and compliance issues.

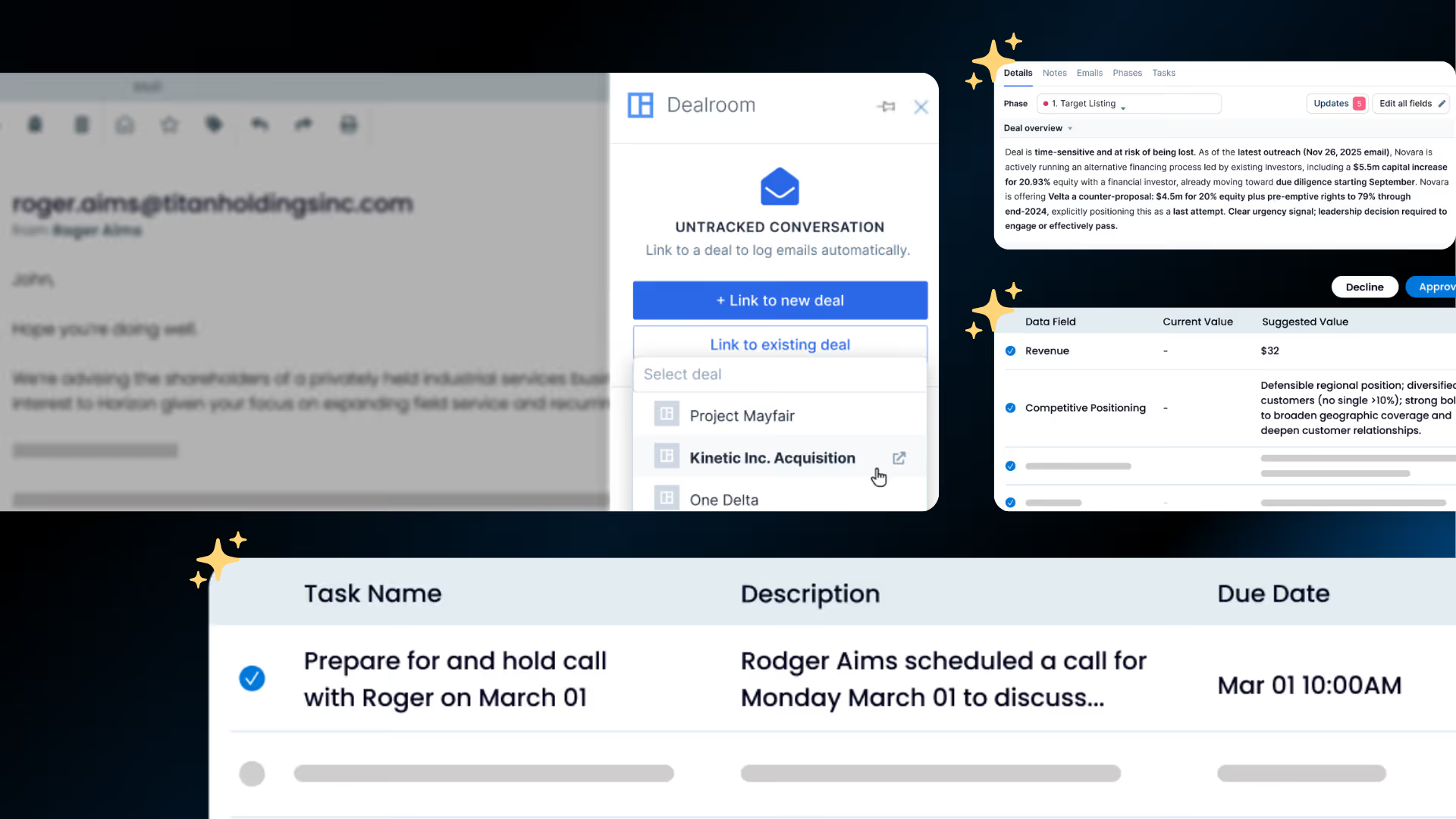

Conducting financial due diligence with DealRoom

The DealRoom M&A platform is designed to simplify and streamline the financial due diligence process, offering built-in playbooks to help you get started quickly. These playbooks act as a step-by-step guide, ensuring that you cover all necessary aspects of due diligence efficiently.

With DealRoom, you have a centralized location to conduct all your due diligence and manage requests. You can invite all stakeholders—whether they are from your team, the target company, or external advisors—and assign granular permissions to control who sees what information. This ensures secure collaboration while giving you complete control over document access.

Each request within DealRoom allows for in-platform conversations, so you can handle all communications directly in the request thread. This eliminates the need for email back-and-forth, reducing time spent tracking conversations and ensuring nothing gets lost in translation.

Additionally, the platform has a virtual data room (VDR) where you can easily drag and drop relevant documents. Each document is indexed and stored in the VDR, ensuring everything is organized and accessible right when you need it. This integration between requests and document management is key to keeping your due diligence process smooth and efficient.

.png)

DealRoom offers DealRoom AI, a powerful feature that can analyze uploaded documents, answer specific questions, extract key information, and even generate summary reports. This feature helps reduce document review time by up to 80%, making the entire process faster and more accurate. Check out the interactive demo - Here!

Key Takeaways

Conducting financial due diligence is like peeling back the layers of an onion. Every new layer reveals something important, and sometimes what you find can completely change the deal. Whether you’re on the buy-side or sell-side, financial due diligence helps you make informed decisions, uncover hidden risks, and ultimately secure a better outcome.

Use DealRoom M&A Platform to streamline your financial due diligence process. Execute the process more efficiently and realize synergies faster.

.png)

.avif)

.avif)

.avif)

.avif)