.avif)

Leveraged buyouts have produced some of thelargest deals in private equity history from the $45 billion TXU buyout in2007 (which ended in bankruptcy) to Blackstone's $26 billion Hilton acquisition (which became one of the most profitable PE deals ever).

We've researched the largest and most recent leveraged buyouts to give you more data on each, and we even created multiple free tools and visualizations around the topic.

This is an interactive table we built that you can filter to dig deeper into LBOs:

Or use our interactive LBO return calculator to determine what the return for an LBO likely was, and how it stacks up:

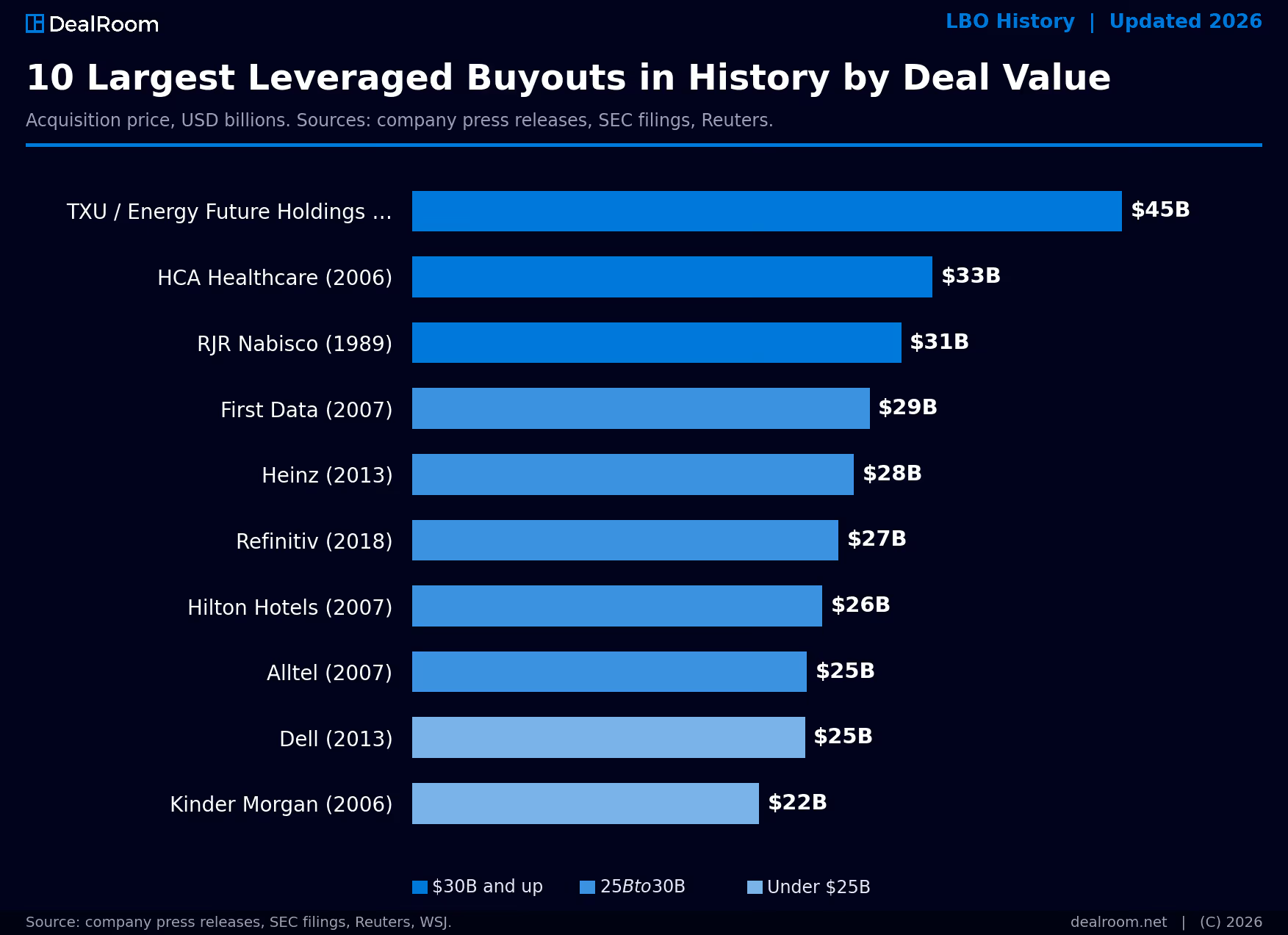

10 Largest Leveraged Buyouts (LBOs) in History

- TXU (now Energy Future Holdings) (2007): $45 billion

- HCA Healthcare (2006): $33 billion

- RJR Nabisco (1989): $31 billion

- First Data (2007): $29 billion

- Heinz (2013): $28 billion

- Refinitiv (2018): $27 billion

- Hilton Hotels (2007): $26 billion

- Alltel (2007): $25 billion

- Dell (2013): $24.9 billion

- Kinder Morgan (2006): $22 billion

1. TXU (now Energy Future Holdings) (2007): $45 billion

In 2007, KKR, TPG, and Goldman Sachs Capital Partners acquired TXU (later renamed Energy Future Holdings) in a $45 billion leveraged buyout - the largest LBO in history. The deal failed, with EFH filing for Chapter 11 bankruptcy in 2014 amid collapsing natural gas prices and an unsustainable debt load that wiped out the entire $8 billion equity check.

This Leveraged Buyout deal was led by KKR, TPG Capital, and Goldman Sachs. This deal involved a Leveraged Buyout of a Texas-based energy company by these private equity giants. It involved a huge amount of debt and relied on high cash flow generated by the target company. However, owing to a financial crisis and a fall in gas prices, the company could not pay its debt and filed for bankruptcy.

Interesting Fact: Despite being one of the biggest LBOs in the world, the TXU LBO ended in bankruptcy because of the unexpected economic downturns.

"The TXU deal underscores the importance of anticipating market shifts and having robust exit strategies in place."

- Financial Analyst

2. HCA Healthcare (2006): $33 billion

In 2006, Bain Capital, KKR, and Merrill Lynch Global Private Equity acquired HCA Healthcare in a $33 billion leveraged buyout. The deal succeeded, with HCA returning to public markets via a 2011 IPO and the sponsors generating an estimated 3-4x return on their equity over the hold period.

HCA Healthcare was acquired by KKR and Bain Capital through an LBO. It was a management buyout, which means the management of the company played a significant role in the LBO. The large amount of debt was supported by the cash flows of the company. Despite the high interest rates, the constant cash flows helped the company utilize the borrowed funds in the most efficient manner, thus making the LBO a huge success.

Interesting Fact: The success of HCA Healthcare in paying back the debts despite the high interest rates highlights the importance of cash flows in LBOs.

"HCA Healthcare's steady cash flow proved to be the lifeblood that sustained the company through the challenges of heavy debt."

- Industry Expert

3. RJR Nabisco (1989): $31 billion

In 1989, KKR acquired RJR Nabisco in a $31 billion leveraged buyout - the largest LBO in history at the time and the subject of the book "Barbarians at the Gate." The deal had a mixed outcome, with KKR breaking up the company over the following decade and the cigarette / food split ultimately delivering modest returns relative to the headline price.

The LBO of RJR Nabisco by KKR is one of the most famous LBOs in the world, as it’s often cited as an example of the working of an LBO. It was a hostile takeover, where the price paid was also quite high, funded by debts. The assets of the target company were utilized to back the debts. Despite the high interest rates, the LBO model proved to be a success in the initial years, but the performance of the company was not satisfactory because of the large debts.

Interesting Fact: The RJ Nabisco deal is included in the book "Barbarians at the Gate," providing a detailed and interesting account of the deal and its complexities.

"The RJR Nabisco deal remains a cautionary tale of the perils of over-leveraging and underestimating market dynamics."

- Financial Historian

4. First Data (2007): $29 billion

In 2007, KKR acquired First Data in a $29 billion leveraged buyout. The deal had a mixed outcome - First Data spent more than a decade carrying its LBO debt load before re-IPOing in 2015 and was ultimately sold to Fiserv in 2019 for approximately $22 billion in stock.

First Data was bought by KKR, where the company’s stable cash flows from processing transactions were used for the financial transaction. The financial deal included a significant amount of debt, and the company aimed to maintain a high level of returns with consistent revenue generation. The financial crisis, however, posed a threat, and the company still managed to go public again, providing a successful exit for the PE companies involved.

Interesting Fact: First Data’s ability to withstand the financial crisis and again go public is a clear indicator of the adaptability of companies in the face of adversity.

"First Data's journey from private to public again exemplifies the cyclical nature of financial markets and the resilience of well-managed firms."

- Market Analyst

5. Heinz (2013): $28 billion

In 2013, Berkshire Hathaway and 3G Capital acquired H.J. Heinz in a $28 billion leveraged buyout. The deal succeeded - Heinz was merged with Kraft Foods Group in 2015 to form Kraft Heinz (KHC), one of the largest food companies in the world, with Berkshire and 3G retaining major stakes through the public-market combination.

Berkshire Hathaway and 3G Capital bought Heinz, a public company, and the deal included borrowed funds and equity finance. The strong company brand and stable cash flows were key factors in raising funds for the deal. The investment expertise of the acquiring company in managing high interest rates and a significant amount of debt led to a successful public issue of the combined company.

Interesting Fact: Warren Buffett's involvement in the Heinz acquisition gave an additional layer of prestige and attention to the deal.

"The Heinz deal, with Warren Buffett at the helm, solidified the merger as a beacon of stability and profitability in the eyes of investors."

- Business Journalist

6. Refinitiv (2018): $27 billion

In 2018, Blackstone (in consortium with Canada Pension Plan Investment Board and GIC) acquired a 55% stake in Refinitiv from Thomson Reuters in a $27 billion leveraged buyout, taking the financial-data and analytics business out of its parent. The deal succeeded - Refinitiv was sold to the London Stock Exchange Group in 2021 for $27 billion in stock, generating a multi-billion-dollar gain for Blackstone in roughly three years.

Blackstone completed the acquisition of Refinitiv using its consistent cash flow and essential financial data service. The acquisition financing included a mix of debt and equity. High interest costs were managed through Refinitiv's robust revenue streams. In this LBO deal, Blackstone took advantage of the valuation of the target company in the financial sector.

Interesting Fact: The acquisition of Refinitiv was one of the biggest deals in the financial sector.

"Refinitiv's acquisition highlighted the increasing importance of financial data and analytics in shaping investment decisions and market strategies."

- Financial Analyst

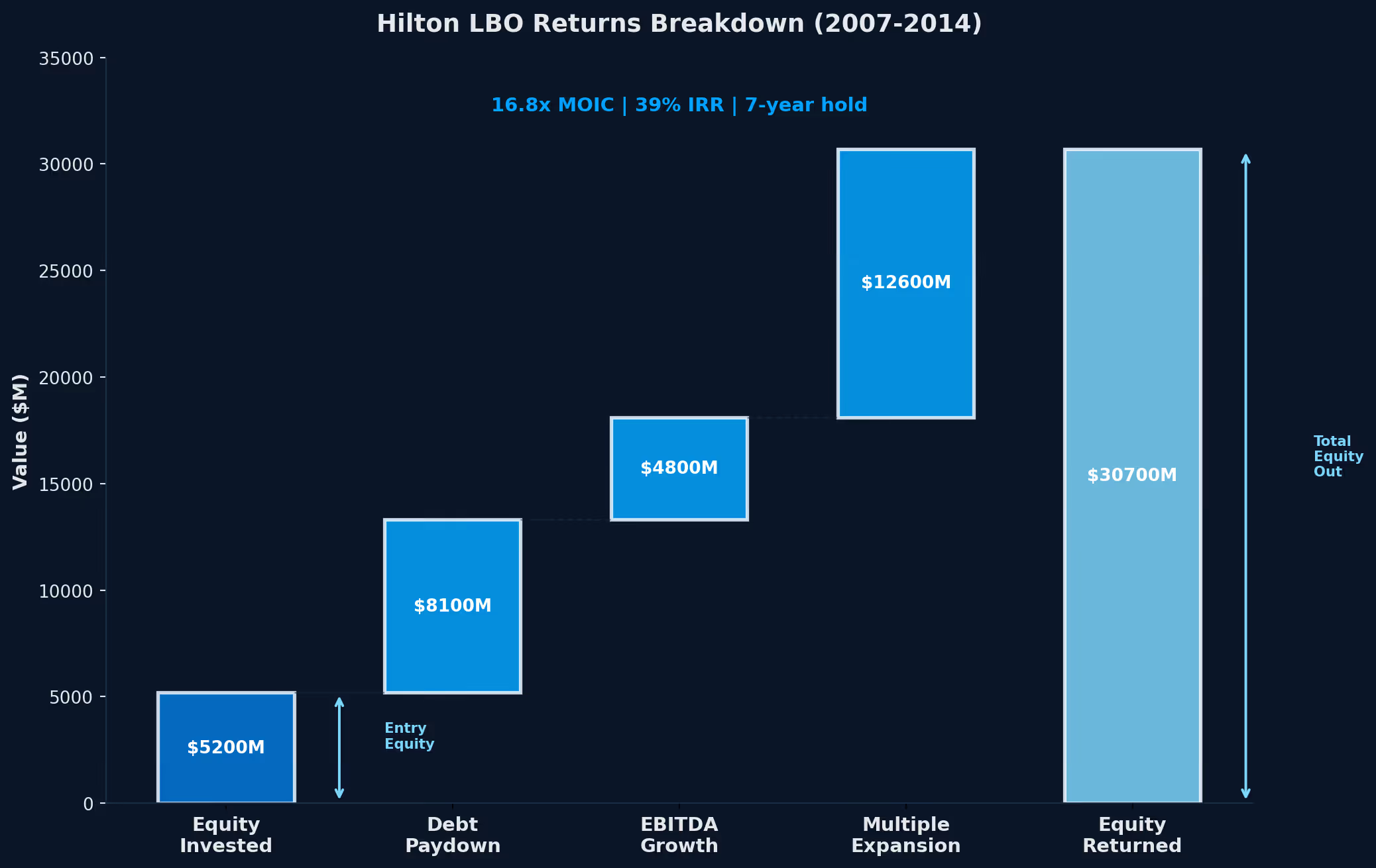

7. Hilton Hotels (2007): $26 billion

In 2007, Blackstone acquired Hilton Hotels in a $26 billion leveraged buyout. The deal succeeded spectacularly - Hilton returned to public markets via a 2013 IPO and Blackstone's exits over the following years generated approximately $14 billion in profit, making it one of the most profitable PE deals in history.

Blackstone acquired Hilton Hotels just before the financial crisis. Despite the economic crisis, Hilton's consistent cash flow and brand value helped service its debt obligations. In this acquisition deal, Blackstone borrowed a large amount of money. Operational improvements were implemented to increase the rate of return on investment. Finally, Hilton was taken public again, showing a successful exit strategy.

Interesting Fact: Hilton Hotels, which was acquired just before the financial crisis, has managed to come out of the turbulent times, thus proving the viability of the business model.

"Hilton's ability to weather the storm and emerge stronger underscores the enduring value of brand reputation and operational excellence."

- Hospitality Expert

8. Alltel (2007): $25 billion

In 2007, TPG Capital and Goldman Sachs Capital Partners acquired Alltel in a $25 billion leveraged buyout. The deal succeeded - the sponsors flipped Alltel to Verizon for approximately $28.1 billion just one year later, in mid-2008, generating one of the fastest LBO exits in industry history.

TPG Capital and Goldman Sachs acquired Alltel, a telecommunication company, when mobile technology was in transition. The acquisition was financed using Alltel's cash flows and projected growth. Within a year, Alltel was sold to Verizon, providing a lucrative exit for the private equity firms.

Interesting Fact: Alltel's acquisition by Verizon was a quick process, showing how dynamic the telecommunication sector is.

"The Alltel deal epitomizes the speed and agility demanded in an industry characterized by rapid technological advancements and fierce competition."

- Telecom Analyst

9. Dell (2013): $24.9 billion

In 2013, Silver Lake Partners and founder Michael Dell acquired Dell Inc. in a $24.9 billion leveraged buyout, structured as a management-led take-private. The deal succeeded - Dell completed a transformational acquisition of EMC for $67 billion in 2016, returned to public markets in 2018, and the sponsors generated multi-billion-dollar returns on the take-private bet.

Michael Dell took his company private in partnership with Silver Lake Partners. He wanted to restructure his company without interference from external factors. It was a management buyout involving a lot of debt using the company's assets and projected growth. He wanted to restructure and increase the company's valuation before seeking a public listing again.

Interesting Fact: Michael Dell's decision to take his company private is a move in the right direction for restructuring and repositioning his company for long-term growth.

"Michael Dell's bold move to take the company private was driven by a vision to reinvent Dell for the digital age, free from the constraints of quarterly earnings expectations."

- Tech Industry Insider

10. Kinder Morgan (2006): $22 billion

In 2006, Goldman Sachs and Kinder Morgan's senior management led a $22 billion leveraged buyout of Kinder Morgan, taking the energy-infrastructure company private. The deal succeeded - Kinder Morgan returned to public markets via a 2011 IPO and is now one of the largest midstream-energy operators in North America.

This LBO transaction was led by the company's management and Goldman Sachs, where Kinder Morgan went private. The company raised a huge amount of debt, which was secured by the company's consistent cash flows from its energy infrastructure business. The company faced some problems, but its consistent cash flows helped it to manage its debt and interest repayment obligations.

Interesting Fact: The successful management of debt obligations by Kinder Morgan is a significant fact in the context of LBOs in the energy infrastructure industry.

"Kinder Morgan's ability to thrive amidst the challenges of the energy market reaffirms the resilience of infrastructure investments in the long term."

- Energy Analyst

.png)

Frequently Asked Questions

What is a Leveraged Buyout?

A Leveraged Buyout is a situation wherein an investor buys a company with borrowed money. The assets and cash flow of the target company are used as collateral for these debts. This is done to increase the returns on equity.

Why do Private Equity Firms perform Leveraged Buyouts?

Private equity firms perform Leveraged Buyouts because they enable these firms to acquire a company with a smaller amount of capital. This is because they can finance a larger percentage of the deal by debt, thus increasing the potential return on investment. Once they acquire a company, they work on improving it and increasing its profits before selling it or going public.

What are some of the most famous Leveraged Buyouts?

Some of the Leveraged Buyouts that can be considered the most famous include:

- RJR Nabisco by KKR

- TXU Energy by KKR, TPG Capital, and Goldman Sachs

- HCA Healthcare by KKR and Bain Capital

- Hilton Hotels by Blackstone

- TXU Energy by KKR, TPG Capital, and Goldman Sachs

- Heinz by Berkshire Hathaway and 3G Capital

What are some of the key determinants of a successful Leveraged Buyout?

The key to a successful Leveraged Buyout is good cash flow, proper debt usage, and effective operations. A clear exit strategy through sale or IPO is important too. For instance, Hilton and HCA were successful due to proper cash flow and constant improvements in operations.

What are some reasons why leveraged buyouts fail?

An LBO may fail if the acquired business fails to meet its debt obligations. Economic or business environment issues may cause businesses to fail in meeting their debt obligations. For instance, TXU’s failure was caused by low energy prices and the 2008 financial crisis.

How do investors make money in leveraged buyouts?

Investors in LBOs make money through increasing the value of the business. Investors may improve business operations to increase its value. As the business value increases, investors may sell or take it public to make money.

What is the role of management in leveraged buyout?

The management plays a key role in Management Buyouts (MBOs), in which management buys out the business with other investors. Management has knowledge about the business and ensures that goals are achieved in line with other investors.

What are some recent examples of leveraged buyouts?

Recent LBO transactions include:

- Acme Corporation by XYZ Capital – specializing in tech growth.

- Global Logistics Solutions by Alpha Partners – enhancing supply chain effectiveness.

- BioPharm Innovations by Beta Capital – increasing biotech potential.

- Retail Dynamics Inc. by Gamma Investments – increasing retail performance.

- Tech Solutions Group by Delta Ventures – increasing software and IT capabilities.

What lessons can be learned from past Leveraged Buyouts?

The history of LBO transactions has demonstrated that companies need to have consistent cash flow, financial discipline, and planning to achieve success in LBO transactions. Overleveraging a company, even a successful one, can be fatal.

How do Leveraged Buyouts impact employees and operations?

An LBO transaction can result in operational changes for a company. The company might reduce its workforce and change its leadership. However, the LBO should be conducted in a way that improves operational efficiencies.

.avif)