Executives of a company with a liquidity problem could reasonably view the opportunity to take on debt as exacerbating rather than solving the issues.

In such cases, it may be beneficial to consider a payment-in-kind loan, wherein interest repayments are made in a form other than cash.

DealRoom helps companies raise and structure capital and today, we'll take you through a guide to payment-in-kind (PIK).

What is Payment in Kind?

Payment in Kind (PIK) refers to the payment of dividends or interest to investors or creditors in a form other than cash. Although technically, the payment in kind could be any asset with an equivalent value to the notional interest payments, usually the repayment is made by issuing more equity securities in the PIK debt issuer. The only time that cash is paid by the debtor is at the end of the loan when the principal and accrued interest repayments are made in cash.

How Payment in Kind Works

Understanding the term ‘in kind’ is key to understanding the idea underpinning payment in kind. According to the Oxford dictionary, ‘in kind’ means: “in the same way, with something similar.” In the case of interest payment, the company issuing the debt isn’t going to pay with cash, but they’re going to pay in the same way, with something similar. Hence, payment in kind.

The repayment structures of traditional loans aren’t always convenient for companies with liquidity issues. Many loan structures demand interest repayments one month after the debt has been issued. The company would barely have had time to feel the effects of investing the funds received before payments had to be made.

Enter the payment in kind loan. Companies with liquidity issues turn to these as a means of gaining access to cash, without the immediate need for repayment. Although the notional interest payments are significantly higher - owing to the risk of extending a loan to a company that is not cash-generative in the short term - it can work for both parties.

A health warning here: Not every company that isn’t cash-generative in the short term is in financial trouble. For example, many companies working upstream in the commodity supply chain face long cash cycles. Cotton producers usually wait 9 months to convert their output into cash, potentially creating liquidity issues in the short term.

Other features of a PIK loan include:

- PIK loans are usually issued for periods of five years or longer

- PIK loans usually feature a warrant enabling the lender to obtain some of the company’s equity, giving them the option to partake in the company’s success

- Like Mezzanine finance, PIK loans are unsecured, meaning no collateral is required

- Difficult to refinance

Why Would a Company Prefer a PIK Loan?

PIK loans are usually preferred by companies with low liquidity or who believe their equity to be over-valued. In the first category - companies with low liquidity - the borrower could be a company with a long cash cycle (as with the cotton producers), or a company in financial difficulty. In such cases, the high-risk finance provided by PIK loans can create a toxic situation for the borrower and lender alike.

‘PIKs’ also tend to regularly appear in the following guises:

- Private equity: While PIKs are not common among banks – who cannot justify the risks involved – they are commonly seen used by private equity firms, looking for higher returns on loans to companies.

- Leveraged Buyouts (LBOs): As a rule, LBOs involve the buy-side taking on substantial debt obligations with large interest payments to be made in cash. PIKs enable the buyers to gain more leverage without the short-term requirement to repay in cash.

- Management Buyouts (MBOs): A similar dynamic to that of LBOs, PIK enables those involved in the MBO bid to take on more debt, without bringing in the extra duress of increased cash payments in the short-term.

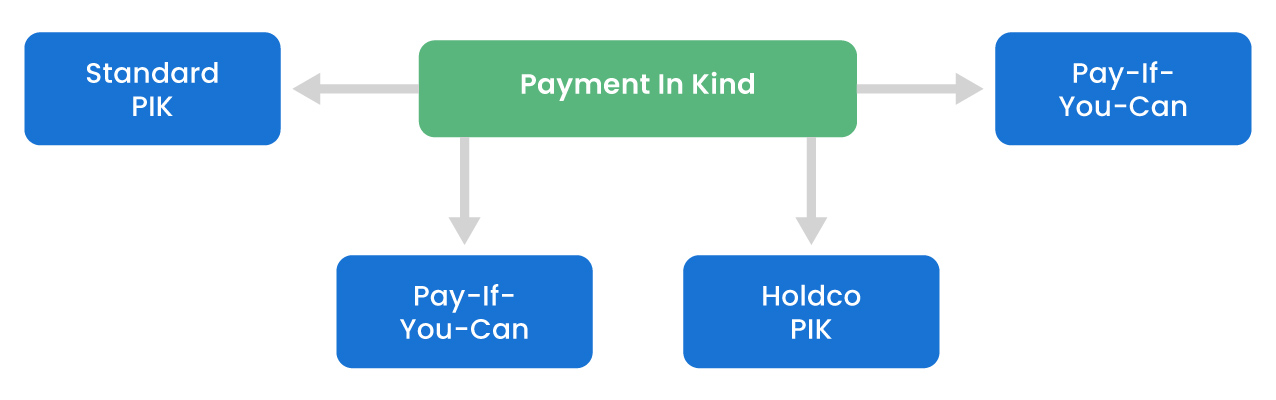

Types of Payment in Kind

As with mezzanine finance, the form of finance most commonly associated with PIK loans, there are several forms. These include:

- Standard PIK: A contract between debtor and creditor that lays out the terms of the loan - similar to a traditional loan format. All expectations, commitments, and dollar amounts are described in detail.

- Pay-If-You-Can: A standard PIK contract with a movement towards cash payments before the end of the contract (as opposed to the right at the end). If the borrower cannot make the cash payment, new stricter terms on the existing payments kick in.

- Pay-If-You-Like: Referred to as ‘toggle notes’, these agreements enable borrowers and lenders to toggle between cash and non-cash interest payments as they wish, with different interest rates applying to each situation.

- Holdco PIK: In this agreement, the borrower stipulates at the outset that their cash flows are dependent on a third party - a parent company - potentially making the repayments far riskier than the regular operating cash flow generated by the borrower.

Example of Payment in Kind

As interest rates begin to rise, and lenders become more careful about which companies they lend to, we can expect a rise in the PIK loan.

In April 2022, Carvana entered a deal with a private equity investor already invested in the company, Apollo Global Management, to what amounted to a $1.6 billion PIK loan.

The loan in question involved a series of investor-friendly provisions (i.e. non-cash benefits), enabling the cash-tight car dealer to enjoy the benefits of a loan without having to make cash payments in the short term, running down its already-stressed cash balance.

Key Takeaways

In summary, payment in kind:

- Refers to a form of payment that is made in a non-cash form.

- Is considered to be a hybrid security, with elements of debt and equity.

- Is a higher risk, owing to the nature of repayments.

- Enables borrowers and lenders to find more creative solutions to liquidity.

.jpeg)

.png)