.avif)

As someone with over a decade in M&A, I get asked how to calculate the acquisition price of a company frequently. Price is often where deals are won or lost. The number I trust starts from the target's standalone enterprise value, adds a control premium and counts only the synergies you can realistically capture.

In DealRoom's State of M&A report, we found that programmatic acquirers who priced with discipline beat their peers on median annual shareholder returns by 2.3 percentage points. Here is how I build a number you can actually defend.

You can use the tool above (built by our engineering team based on years of M&A deal flow) to calculate an estimated acquisition price. Before discussing how to calculate the acquisition price of a company, however, it’s important to underline that the price is just one component of the acquisition.

Even when a company is acquired for a knockdown price - or at least, what is perceived to be a knockdown price - it could transpire that the company paid too much.

That’s because the price you pay is only one component of the value you gain.

As most ‘how to’ guides on M&A are keen to emphasize, a significant percentage of the value in a deal is unlocked in the integration phase (hence, the need for a change manager).

All that said, you give your deal a much better chance of generating value if the acquisition price is right.

We at DealRoom work with many companies organizing their M&A process and below, we have put together some strategies you should employ when calculating the acquisition price of a company.

These rules are general enough to hold true for a small company making its first foray into mergers and acquisitions, or a much larger firm with a long track record of closing deals.

What is an acquisition price?

The acquisition price is the total consideration paid for a company on an agreed date.

For accounting it also includes directly attributable transaction costs (legal, advisory, due-diligence and brokerage fees), so it usually exceeds the headline price agreed between the two parties.

If the market reacts well to news of the deal, the value for shareholders would rise thanks to an increase in the stock price, with the opposite happening if the market reacted badly.

Furthermore, for the sake of accounting, the acquisition is considered an acquisition of an asset.

As such, the acquisition price which will appear on the company’s financial statements is not just the price agreed between the two companies, but also the cost of making the transaction a reality, including legal fees, outside consultants’ fees, brokerage fees, and more.

How to determine acquisition price

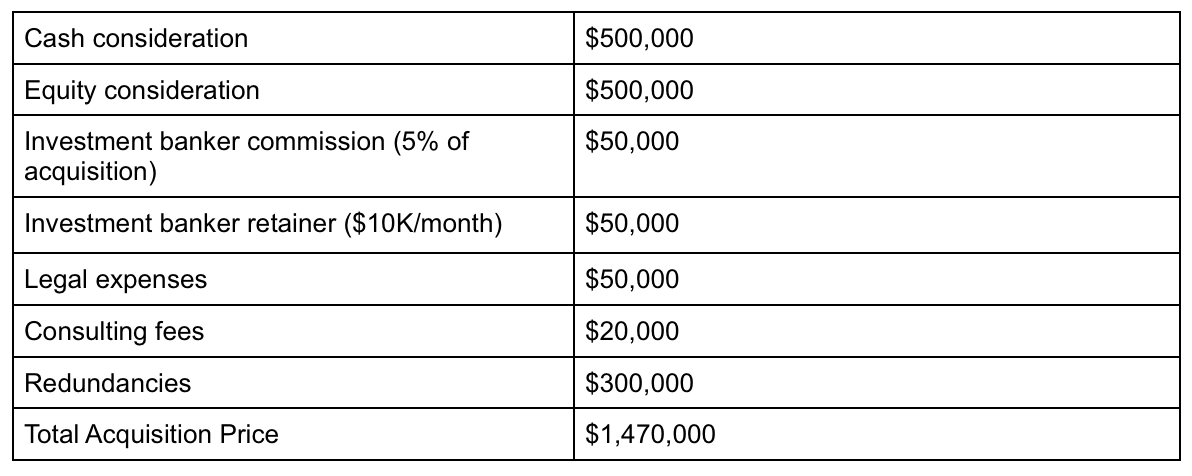

Let’s suppose that your company acquires a company for $1 million for an even breakdown of cash and stock.

Let’s also assume that there were some other costs involved in making the deal a reality (including the integration costs).

There is some flexibility on these costs, as companies can contract investment bankers and ultimately not make any acquisitions, in which case, these would be pure operational costs.

If the acquisition closes, the expenses can be capitalized, however.

The acquisition price might look something like the following:

With the costs adding up so quickly, it’s easy to see why it’s so important to make sure, i) that there’s a strong motive for the acquisition in the first place, and ii) that the consideration being paid for the acquisition is fair relative to the target company’s intrinsic value.

Get a second opinion

One of the most common mistakes of buyers is to let the grand vision cloud their perspective. A business should only be bought when the numbers make sense.

When you believe that they do, you should ask a second opinion. And this is important - the second opinion should be from a trusted third party, not the investment banker who stands to gain from the transaction.

As we mentioned before, you don’t always need an investment banker in any case.

A few expert opinions are better than one. This gives a range of different perspectives - say, on the technical, marketing, finance and legal aspects of the transaction.

When calculating the value of the deal, don’t just look at your own expertise, draft in intelligence from other areas. Gain any edge when calculating the acquisition price that you possibly can.

"At one point, I had a banker call me at dinner and say we have a problem - we just lost $25 million in EBITDA. I said why? He said the asset manager repriced the fees. $25 million of EBITDA at maybe 8 to 12 times - that kills a deal."

Speaker: Keith Crawford, Global Head of Corporate Development, State Street Corporation

Shared at The Buyer-Led M&A™ Summit (watch the entire summit for free here)

The value of synergies when calculating the acquisition price

Spend some time reading the financial accounts of public companies and something will quickly become apparent: The notes sections that accompany financial statements are a graveyard for targets for which the buyer vastly overrated the synergies and ended up writing down the value of the acquisitions.

This happens to even the most experienced companies.

Microsoft is a culprit that springs to mind. It has written down investments in Nokia ($7.6 billion, 2015) and aQuantive ($6.2 billion, 2012) and may yet end up doing so with LinkedIn.

SMEs, however, don’t have the same cash reserves that Microsoft can fall back on, so write downs tend to be more damaging.

Thus, a good way to think about M&A synergies when calculating the price of an acquisition is not to think about them at all.

That is - there should be synergies behind the motive for the deal, but not in arriving at the calculation price. Synergies do exist. But in the majority of cases, trying to calculate them will only lead to you overpaying.

Paradoxically, the thing which you believe will generate value can end up destroying it instead.

Use more than one valuation tool

As mentioned in a previous post, there are a number of different valuation methods, so there’s no sense in limiting yourself to just one.

At a minimum, acquirers should look to use two methods for valuation - with one industry multiple (EBITDA or revenue, usually) being used to complement another, usually the discounted cash flow or book value.

The industry EBITDA multiplier is relatively straightforward, but remember which end of the industry you’re operating in: Databases like CapitalIQ will provide useful figures on multipliers but you shouldn’t compare NASDAQ companies with SMEs.

For the record, a database like Platt’s is usually a better barometer for multipliers for smaller companies.

Aligned to this, it can be useful to gain a second opinion on value as well. We’re not suggesting you confuse the issue by having too many valuations - merely that you take a few valuations and think of them as a range for the price.

Clearly, the closer you can get to the bottom of that range in your transaction, the better a chance the deal has of generating value.

Frequently Asked Questions

Acquisition price vs purchase price vs enterprise value: what's the difference?

The purchase price is what a buyer pays the target’s shareholders for their equity. The acquisition price is the total consideration recorded for the deal, including transaction costs. Enterprise value sits above both: it values the whole business (equity plus net debt) before financing.

Enterprise value is the value of the whole business (equity plus net debt), independent of how the deal is financed.

A clean deal model starts at enterprise value, bridges to equity value by subtracting net debt, then adds the control premium and deal costs to arrive at the acquisition price.

What is a control premium (and how big is it)?

A control premium is the amount an acquirer pays above a target’s standalone market value to secure control of the business. It exists because control carries rights a minority holder does not have: setting strategy, redeploying cash and capturing synergies. Premiums vary widely by sector and deal type, but public-company acquisitions commonly clear at a meaningful premium to the undisturbed share price. The practical rule is to size the premium against the synergies you can actually capture. If the premium exceeds net realizable synergies, you are pre-paying value you have not yet created.

What counts as an acquisition cost?

Beyond the headline consideration, the acquisition price on the financial statements absorbs the costs of making the deal real: legal fees, financial and commercial due diligence, outside consultants and advisers, brokerage or banker fees and financing costs. When a deal closes, many of these expenses are capitalized as part of the acquisition. If the deal collapses, they revert to operating expense. This is why deal costs belong in the price calculation from the outset, not as an afterthought.

How do you calculate the acquisition price of a private company?

For a private company, build the value from at least two methods (an industry EBITDA or revenue multiple cross-checked against a DCF or book value) using comparables sized to the business, then add a control premium and deal costs and aim for the lower end of the range.

Private companies have no live share price, so you build the value rather than read it off a screen. Start with at least two methods, typically an industry EBITDA or revenue multiple cross-checked against a discounted cash flow or book-value approach, using comparables appropriate to the company’s size (do not benchmark a small business against listed large-caps). Treat the outputs as a range, add a control premium and directly attributable deal costs and aim for the lower end of the range to give the deal the best chance of creating value.

How does an acquisition affect the stock price?

When much of the consideration is the buyer’s own equity, the effective acquisition price moves with the market’s reaction. A well-received deal lifts the acquirer’s shares and raises shareholder value, while a poorly received deal does the opposite.

Why do acquirers overpay?

Acquirers overpay when they let the grand vision cloud the numbers and price in synergies they have not yet captured. The financial-statement notes of experienced buyers are full of write-downs: Microsoft alone impaired Nokia by about $7.6 billion (2015) and aQuantive by $6.2 billion (2012). Treat synergies as the motive, not the calculation.

Key Takeaways

The justified emphasis on change management and integration over the past decade may have led us to underestimate the importance of price to the success of an acquisition.

Price is fundamental. Applying science and rigor to this stage of the M&A process is just as important as doing so later on in the transaction.

Do everything to ensure that you’re achieving a good transaction price now, so that you’re not paying the price further down the line.

.avif)

.avif)

.jpeg)