Takeover: Friendly, Hostile, Motives, Challenges, Defence (+ Examples)

The term ‘takeover’ is used far less regularly for in the financial press for acquisitions than it once was, perhaps because of negative connotations owing to its associations with hostile takeovers.

However, as this article will lay out, takeovers don’t have to be hostile, and in fact, are more frequently agreed to by all parties. This is the DealRoom guide to takeovers.

What is a Takeover?

A takeover is an acquisition of a majority stake in a target company, with or without the agreement of the target company’s management. Takeovers are synonymous with acquisitions, which achieve the same ends. As the introduction paragraph alluded to, the term ‘takeover’ has taken on negative connotations, as many deals that began as friendly acquisition offers that were rebuffed by the shareholders, subsequently became takeover attempts.

Understanding business takeovers

In order to understand business takeovers, we need to take a closer look at them from several different perspectives. We’ll begin with the typical steps involved in a takeover.

Typical steps in a takeover

With the exception of opportunistic takeovers - that is, transactions which weren’t planned, but arose as opportunities presented themselves - most takeovers, whatever the size of company or industry, follow a fairly similar path:

1. Assess market opportunities

Targets should not be assessed in isolation - which is why investment bankers use comparable transactions when assessing transactions. It’s important to look at a range of potential targets in the same bracket, giving the company a good basis on which to make a decision about suitable target candidates.

2. Create a longlist of candidates

The market assessment should enable the company to draw up a longlist of suitable candidates. Broadly speaking, these would include companies that provide a strategic fit, appear to show growth potential, and would probably be priced within the buyer’s budget.

3. Create a shortlist of candidates

After internal discussion and/or an informal approach to the candidates, a shortlist is drawn up. Longlists rarely take long to whittle down to shortlists, as industries move fast. A target may be bought be a private equity firm, or release news that suggest it is otherwise not for sale.

4. Approach target(s)

By the point at which a target is approached, the buyer should already have a range of prices in mind. This should be a credible amount, or the target will (justifably) quickly call a halt to proceedings. The price shouldn’t be mentioned on the call; a range of multiples of EBITDA should suffice.

5. Conduct negotiations

Assuming there is some interest in discussing a takeover, the next phase is negotiations. Here, the buyer and target flesh out the terms and conditions of a mooted transaction. It’s vitally important at this stage that the buyer doesn’t fall into the fallacy of thinking, ‘we’ve come this far, now we can’t go back.’

6. Conduct due diligence

A significant chunk of the transaction’s value will likely be made in the time invested in due diligence. It cannot be overemphasized

7. Close transaction with target

Motives for a takeover

The overriding motive for a takeover is value generation. However, that can come in many forms.

Buyers will cite several different reasons for beginning a takeover attempt, among them:

Strategic

Whereby it is believed that the the target company can better enable the buyer to execute on their corporate strategy. For example, a takeover of a foreign company might be seen as a good way to expand in a market that the buyer had planned to enter.

Acquire capabilities

Many takeovers are motivated by the motivation to acquire capabilities or intellectual property. This is particularly common in the technology space. An example was Google acquiring Android for its cellular technology capabilities.

Achieve scale

Achieving scale enables companies to benefit from economies of scale (higher margins in production, better terms received from suppliers, etc.). Roll-up strategies are usually driven by this motive.

Diversification

Companies become conglomerates through acquiring for diversification. After the takeovers, these companies then become separate divisions under the buyer’s company umbrella.

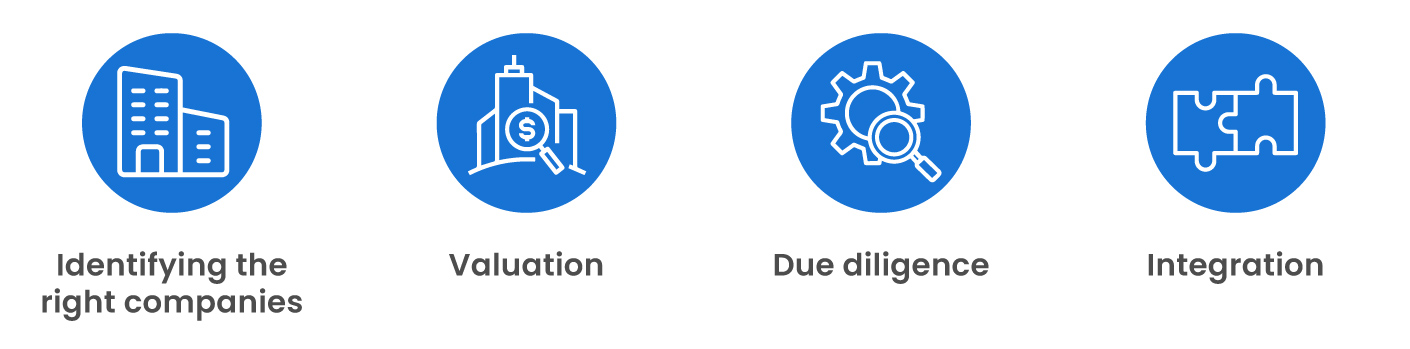

Challenges of a takeover

The takeover process is strewn with challenges, both before and after the transaction has closed.

Below, we look at just some of these challenges, in broadly chronological order.

Identifying the right companies

The motive for a takeover can sometimes override the necessity of ensuring that the buyer identifies the right target. Ensuring objectivity here is a critical challenge for management to overcome.

Valuation

Even if the company is right, a valuation can make the takeover a value destroyer. Investment banks spend most of their time working on valuations, because they’re one of the most important parts of the takeover process.

Due diligence

A thorough due diligence process is a crurical component for the takeover to be a success. Also, as a general rule, the more complex the company, the bigger the due diligence process.

Integration

Once the takeover is complete, the task then becomes integrating the target company into the buyer’s operations. Companies that aren’t properly integrated rarely generate value.

Risks of a takeover

With so much capital at stake - takeovers are the largest investments that companies make - the risks inherent in a takeover are existential for the buyer. These risks can all be categorized as ‘value destruction’.

They include, but are not limited to:

Overpaying

Target companies rarely look for a fair price - instead, they look for a price well in excess of that number. This creates a conflict of interest at the outset that often sees the buyer overpaying for the target.

Culture clashes

Corporate culture or ‘how things get done around here’ is different at every company. Sometimes the differences are more subtle than others, but they still exist. Culture clashes reduce corporate efficiency and create a drain on resources.

Bad timing

Economic and business cycles can dictate whether takeovers are a success or not. All takeovers are subject to exogenous risks such as interest rate hikes, financial crashes, or technological shifts.

Underlying Issues in Target

In their efforts to sell, target companies are often less transparent than they might be. Some value-destroying issues may not appear until well after the transaction has closed. This is why a thorough due diligence process is necessary.

Types of takeover

Takeovers are categorized into five separate buckets:

Friendly takeover: Where both sides of a transaction consent to the deal.

Hostile takeover: Where the buyer begins hoovering up stock in the target company without its management’s knowledge or buy-in.

Reverse takeover: Where a private company acquires a public company to gain its listing and avoid the need for an IPO.

Backflip takeover: Where the buyer retains the target’s name after the takeover because the target’s stronger brand image.

Bailout takeover: Where a struggling company is rescued under the terms of a financial institution or government (e.g. JP Morgan’s acquisition of Bear Stearn in March 2008).

Defense strategies for takeovers

There are countless number of defense strategies for target companies looking to stave off an unwanted buyer. The most common of these are:

Poison pill

Where the target company management sells its shares at a discount to several third parties, ensuring that the interested buyer will have to pay more by virtue of appealing to a broader pool of shareholders.

Scorched earth policy

Where the target company makes itself more unattractive to the buyer by implementing changes such as bringing on more debt, promising large management payouts in the event of firing, and even selling off key assets.

Golden parachute

Where the target company offers a massive salary increase to its executives in the event of a takeover, thereby making the takeover less attractive to the buyers.

Macaroni defense

Where the target company issues a large number of bonds that must be redeemed at a high price if the takeover occurs.

Pacman defense

Where the target company counters the buyer’s offense by beginning to buy up shares in the buyer’s company, thereby creating a counter offensive.

The importance of due diligence

Due diligence is a hugely important component of successful takeovers. Even companies that may appear on the surface to be perfect matches require a thorough due diligence process, the kind which DealRoom is designed for.

The DealRoom project management tool for M&A was designed with the help and feedback of practitioners who, combined, have closed several thousand deals.

The success of the takeovers that have used DealRoom is testament to its capabilities.

On the other hand, think of a deal like that of Caterpillar’s doomed $677 million acquisition of China’s ERA Mining company a decade ago. On the surface, Caterpillar’s executives believed they were buying into a company that gave them access to China’s mining boom.

If they had used DealRoom to conduct due diligence, they’d have seen a very different story.

Takeover financing

Takeovers can be financed by cash (retained earnings or debt), equity, or some combination of the three.

When equity prices are high, buyers in takeovers tend to offer more equity as part of the transaction.

Similarly, when debt prices are low - as they have been for the past 15 years - companies tend to use more debt. As a general rule, paying with equity is preferable to debt, as it also ensures more buy-in from the target company’s shareholders.

Examples of Takeovers

A relatively recent example of a friendly takeover was that of Facebook’s acquisition of WhatsApp for $19 billion in 2014.

The takeover was untypically friendly: Having learned of Facebook’s interest in a takeover, WhatsApp’s co-founder and CEO, Jan Koum, arrived on Facebook CEO Mark Zuckerberg’s doorstep with chocolate-covered strawberries. His aim was to discuss a deal.

By the time the two had finished the plate of strawberries, the terms of a deal had been fleshed out.

Example of a failed takeover

The most famous example of a failed takeover over the past 20 years is undoubtedly Microsoft’s failed takeover attempt of Yahoo in 2008. Although Microsoft may now look back and realize how lucky it was that the takeover was blocked, there was plenty of wrangling 15 years ago, as it sought to put its search engine capabilities on the map (Bing was released a year later, so we can assume that search was the primary motive for the attempted takeover).

In February 2008, Microsoft bid $31 per share in a cash and stock offer for Yahoo, which amounted to a $41 billion takeover. Three months later, after the attempt had turned hostile, Yahoo’s management team was still willing to budge on the offer, and Microsoft had to accept that it wasn’t getting anywhere. It pulled out of the takeover attempt. In 2015, Yahoo was acquired by Verizon in tandem with AOL for a combined $9 billion. Verizon took a $4.6 billion writedown on the takeover in 2018, perhaps saving Microsoft’s blushes in the process.

Summary

DealRoom is an M&A project management tool that benefits both sides of the takeover process.

Whether you're a seasoned professional or a first-time seller (or a buyer), DealRoom is the perfect solution for all your M&A needs.

Whether your motive is a friendly takeover, a Macaroni defense, or anything in between, DealRoom offers a powerful solution. Users benefit from state-of-the-art data protection, seamless communication and sharing of documents between participants, progress reports that show what percentage of tasks need to be completed, and more.

Talk to us today about how we can supercharge your takeover process.

%20(1)-p-800.jpeg)

Get your M&A process in order. Use DealRoom as a single source of truth and align your team.

.svg)

.png)